Download

1 / 36

360 likes | 654 Views

The External Environment for Developing Countries November 2009 The World Bank Development Economics Prospects Group. Global IP gaining momentum in the third quarter of 2009 growth %, 3 month saar. Source: World Bank, DEC Prospects Group.

E N D

The External Environment for Developing CountriesNovember 2009The World BankDevelopment EconomicsProspects Group

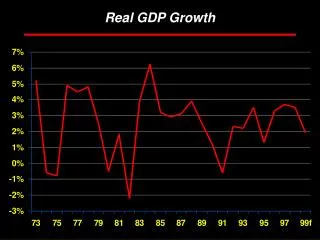

Global IP gaining momentum in the third quarter of 2009 growth %, 3 month saar Source: World Bank, DEC Prospects Group.

Gross capital inflows to developing countries surge in second half of 2009 % share of GDP, 2009*=annualized Sources: Dealogic and World Bank

U.S. economy pulls out of recession with 3.5% growth in Q3-2009 (saar) growth of real GDP, and contributions to growth in percentage points Stocks Investment Government Consumption Net exports Source: Department of Commerce.

A favorable employment turn in Octoberwith retail sales maintaining momentum retail sales growth (saar) [L]; change in employment (‘000, 3mma) [R] Retail sales [L] Change in employment [R] Source: U.S. Departments of Commerce and Labor.

Manufacturing has led recoverybut services emerging to growth Headline PMI indices for manufacturing and services sector [50=+growth] PMI Services PMI manufacturing Source: Institute for Supply Management.

Japan’s GDP growth beats expectations for the third quarter at 4.8% (saar) growth of real GDP, and contributions to growth in percentage points Net Exports Stocks Government Consumption Investment Source: Japan Cabinet Office.

Japan’s export- and production growth waning into the third quarterexport volumes and manufacturing production, ch% saar Goods export volumes Production Source: Japan Cabinet Office.

New Japanese government inherits debt equivalent to 190% of GDPgeneral government balance as a share of GDP in percent Source: Japan Cabinet Office.

Euro Area emerges from recessionon growth in the ‘Big-3” economiesGDP growth, q/q percentage change saar Source: Eurostat.

Euro Area production up in September on exports and stock rebuildingmanufacturing output, German and French export volumes, ch% (saar) France exports Euro Area IP Germany exports Source: Eurostat.

Houshold spending still a damper on growth retail volume growth, Euro Area, Germany and France, (ch%, 3mma, y/y) Euro Area retail volumes Germany retail volumes France retail volumes Source: EUROSTAT.

Global IP picked-up sharply in the third quarter of 2009 growth %, 3 month saar Source: World Bank, DEC Prospects Group.

High-income countries emerged to growth in output during 2009-Q3 growth %, 3 month saar Source: World Bank, DEC Prospects Group.

Capacity utilization- outside of Europe trending back toward pre-crisis levels Source: Thomson Datastream and World Bank.

East Asian imports step up as Chinese import momentum begins to slowimports, 3mma saar % change Source: Haver Analytics.

Import recovery in China grounded in capital-and consumer goodsimports, year-over-year % change Source: Haver Analytics.

German and Japanese export volumes surge on rising external demanddeveloping import volumes, German and Japanese export volumes, 3mma saar % change Source: World Bank, DEC Prospects Group.

Oil prices break out of recent range… but market still well supplied $/bbl mb/d OPEC Production [R] Oil price [L scale] Source: IEA and DECPG Commodities Group.

OECD total oil stocksdays of forward consumption Source: IEA and DECPG Commodities Group.

WTI Futures Prices - NYMEX Monthly contract prices to Dec 2017* for select dates in 2009 $/bbl Nov 11 Jul 13 Feb 18 *Monthly prices interpolated for 2015-17

Grains prices rise on late U.S harvest c/bushel Soybeans [left scale] Corn [right scale] Wheat [left scale] Source: Datastream and DECPG Commodities Group.

Metals prices remain rangebound $/ton $/ton Copper Nickel Zinc Source: LME and DECPG Commodities Group.

Gold prices surge above $1,100/toz per toz Gold in US$ Gold in euros Source: LME and DECPG Commodities Group.

Flows to emerging markets surge to $50 billion in October… a new record Source: DECPG Finance Team.

Low interest rates in high-income countries contribute to inflows to emerging markets Three-month interbank interest rates (%) Sources: Thomson Datastream and World Bank.

Deteriorating credit quality for EM sovereignsnet rating: number of upgrades minus downgrades* *Includes rating actions from Moody’s, S&P, and Fitch. Source: Bloomberg and DECPG staff calculations.

Dollar’s fall from Spring peaks now 20% vs Euro…10% against yen USD per Euro (inverse) [Left] and Yen per USD [right] USD/Euro (inverse) yen/USD Source: Thomson/Datastream.

Dollar fall is half that of 2002-07… but decline compressed into 6 months Indices, Jan 1990=100. 12% decline 25% decline Nominal effective rate [NEER] Real effective rate [REER] Source: JPMorgan-Chase.