Download

1 / 51

510 likes | 1.01k Views

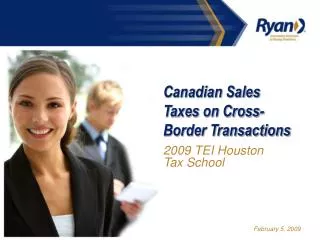

Canadian Sales Taxes on Cross-Border Transactions. 2009 TEI Houston Tax School . February 5, 2009. Cross-Border Transactions. Contents Introduction: value-added taxation in Canada Place of supply rules Taxation of imports Taxation of exports Drop-shipments Rebates. Tax Rates in Canada.

E N D

Canadian Sales Taxes on Cross-Border Transactions 2009 TEI Houston Tax School February 5, 2009

Cross-Border Transactions • Contents • Introduction: value-added taxation in Canada • Place of supply rules • Taxation of imports • Taxation of exports • Drop-shipments • Rebates

Tax Rates in Canada YT PST N/A HST 13% NT PST N/A NU PST N/A BC PST 7% AB PST N/A SK PST 5% MB PST 7% QC QST 7.5% ON PST 8% PE PST 10% GST 5%

Introduction • Goods and Services Tax (GST) • Value-added tax • Destination based • Taxes consumption of goods and services in Canada

Introduction • GST • Collected by registrants • Input tax credits (ITCs) • Exempt and zero-rated supplies

Introduction • Harmonized Sales Tax (HST) • Value-added tax • Destination based • Taxes consumption of supplies in the participating provinces • New Brunswick, Nova Scotia and Newfoundland & Labrador • Simply GST at 13%

Introduction • Quebec Sales Tax (QST) • Provincial value-added tax • Calculated on a GST-included amount • Taxes consumption of goods and services in Quebec • Input tax refund restrictions

Registration and Collection • Registration – GST/HST and QST • Required registration • Thresholds • $30,000 • $50,000 – public service bodies • Non-residents • Delivery of goods

Registration and Collection • Registration – GST/HST and QST • Non-resident registration requirements • Critical objective of the ETA • Concept of “carrying on business” • Implications to non-resident

Registration & Collection • Registration – GST/HST and QST • “Carrying on business” • Implications for: • Supplies of goods • Leases • Services • E-commerce

Registration and Collection • Registration – GST/HST and QST • CRA Policy Statement P-051R2 • Factor approach adopted • References to existing case law removed

Registration and Collection • Registration – GST/HST and QST • Contradicting situations in the Policy Statement • Example 1 • Example 12 • Example 14

Registration and Collection • GST/HST and QST • Voluntary registration • When permitted • Security requirements

Registration and Collection • Collection of tax • by registered suppliers • by recipients who import services or intangibles • self-assessment otherwise not generally permitted

Registration and Collection • Collection of tax • by the Canada Border Service Agency (CBSA) on goods imported into Canada • commercial goods • paying tax twice • non-commercial goods

Place of Supply • Taxable supplies made in Canada • First determine if supply is made in Canada • Second determine if supply is: • Zero-rated or exempt • Made in Quebec or participating (HST) province

Place of Supply • GST place of supply rules • Goods • Destination based • Supplied by way of sale • Supplied by way of lease or license

Place of Supply • GST place of supply rules • Services • Intangibles • Real property

Place of Supply • HST/QST place of supply rules • Separate set of place of supply rules • Complicated rule set to make determination • Outside scope of presentation

Place of Supply • Supplies made by non-residents • Overview • Non-resident override rule • Concerns • Supplies made by registered non-residents • Non-residents carrying on business in Canada

Taxation of Imports • Importation of goods – GST • 5% on the value of taxable goods imported into Canada • Payable by importer of record • Collected by the CBSA • Tax base of imported goods • Importation of goods – QST • Not collected • By CBSA on commercial imports into Canada • On interprovincial transactions

Taxation of Imports • Importation of goods – GST • Potential for double tax if goods supplied by registered non-resident • No provision to self-assess tax on imported goods

Taxation of Imports • Importation of goods – GST • Exemptions are available for goods not intended to be taxed • Non-taxable imported goods • Temporary Importation Regulations to the Customs Act • Inward processing

Taxation of Imports • Temporary use • Relief is available in cases of temporary presence or use • Proportionate relief • GST/QST • RST

Taxation of Imports • Services and intangible property – GST/QST • Imported taxable supplies • Services • Intangibles • Goods • Leases • Drop-shipments

Taxation of Imports • Services and intangible property – GST/QST • Imported taxable supplies • Exclusions • Exclusive use • Generally 90% or more • 100% for financial institutions

Taxation of Imports • Services and intangible property – GST/QST • imported taxable intangible property • Exclusions • Imported taxable supplies - example

Recovery of Tax on Imports • GST issues • For use in commercial activity • For the purpose of performing a commercial service • Excludes shipping • De facto importer issue • Caused the goods to be imported • Generally the owner of the goods

Recovery of Tax on Imports • GST issues • Solution to de facto importer issue • Section 178.8 - importer arrangement rules • Deems tax to be paid by the constructive importer • Supplier considered an agent • Agreement under Division II • Supplier must be a GST registrant • Considers supply to be made in Canada • Tax charged by supplier under general place of supply rules

Recovery of Tax on Import Canadian GST Registered Recipient Canada U.S. Supply of Goods Delivery Registered / Non-Resident Manufacturer Importer of record

Recovery of Tax on Import • GST issues • Goods imported for the purpose of performing a commercial service • Definition of commercial service • Recovery of GST • QST – no equivalent provision

Recovery of Tax on Import • GST/QST issues • Flow-through of taxes paid • To Canadian purchaser • To Canadian service provider

Recovery of Tax on Import Canadian GST Registered Recipient Delivery Canada U.S. Supply of Goods Non-Registered / Non-Resident Manufacturer Importer of record

Recovery of Tax on Import • GST/QST issues • Rebates available where no ITC/ITR permitted • For returned goods • Damaged or inferior goods • Subject to a 2-year claim period

Taxation of Exports • Export of goods – GST • Exported by vendor • Supplied outside Canada • No Canadian tax • Maintain evidence of export • Exported by recipient • Supplied inside Canada • Possible zero-rating • Conditions

Taxation of Exports • Export of services – GST/QST • Services • Supplied outside Canada/Quebec • Supplied inside Canada/Quebec • Generally zero-rated where supplied to a non-resident

Taxation of Exports • Export of services – GST/QST • Exclusions from the general zero-rating provisions

Taxation of Exports • Export of services – GST/QST • Generally zero-rated services include: • Advisory (provide opinions) • Consulting (provide information, instruction and expert advice) • Professional services (provided by person with specialized or advanced education • Sales/purchasing representatives • Advertising services • Other services and intellectual property • Dies, jigs and molds

Taxation of Exports • Export of services – GST/QST • Services related to property located in Canada/Quebec • Generally taxable • Zero-rated for qualifying services

Taxation of Exports • Export of services – GST/QST • Documentation requirements • Qualifying service • Verification of customers • Non-resident status • Non-registrant status

Drop-Shipments • Basic concepts • Objectives of legislation • Typical drop-shipment scenarios

Drop-Shipments • Goods • GST and QST • Supplies deemed to be made outside Canada/Quebec • Goods delivered in Canada/Quebec • On behalf of a registered non-resident • On behalf of an unregistered non-resident

Drop-Shipments - Goods Company C Company B Delivery of Goods Canadian GST Registered Supplier Canadian GST Registered Recipient (2) Selling Price ($1,500) + GST paid to supplier ($75) Selling Price ($1,000) + GST on FMV of Goods ($75) (3) Company A (1) Note: Flow-through provision available to Company B Unregistered / Non-Resident Customer / Supplier

Drop-Shipments - Goods Company B Delivery of Goods Drop-shipment Certificate Company C Canadian GST Registered Recipient Canadian GST Registered Supplier Selling Price ($1,500) No GST Selling Price ($1,000) No GST Company A Unregistered / Non-Resident Customer / Supplier

Drop-Shipments - Services Company D Company C Company B (5) (3) Canadian Registered Service Provider Canadian GST Registered Supplier Canadian GST Registered Recipient Selling Price ($500) + GST on FMV of Processed Goods ($100) Selling Price ($1,000) + GST ($50) Selling Price ($2,000) + GST paid to Co. C & Co. D ($50 + $100) (4) (1) (2) Company A Unregistered / Non-Resident Customer / Supplier

Drop-Shipments - Services Company D Company B goods goods Company C Canadian GST Registered Recipient Canadian GST Registered Supplier D/S certificate D/S certificate Service Provider Selling Price ($500), No GST Selling Price ($2,000) No GST Selling Price ($1,000) No GST Company A Unregistered / Non-Resident Customer / Supplier

Drop-Shipments • Goods • RST • General rules • Tax follows the goods

Drop-Shipments • Goods • RST • Specific rules by province • Ontario • Prince Edward Island • Manitoba

Drop-Shipments • Goods • RST • Specific rules by province • British Columbia • Saskatchewan

Special Situations • Rebates – GST/QST • Visitor Rebate Program eliminated • tour packages • non-resident exhibitors, sponsors and organizers of foreign conventions • installation services • non-resident contractors