Download

1 / 19

200 likes | 304 Views

Business Finance. MB-664 DuPont Model. Profit Improvement. Du Pont Formula. ROA can be broken down into margin and turnover Gain insight into planning for profit improvement Improve margin Improve turnover Improve both!. Improve Margin. Reducing expenses Using less costly materials

E N D

Business Finance MB-664 DuPont Model MB 664 UVG-TAMU May 2009

Profit Improvement MB 664 UVG-TAMU May 2009

Du Pont Formula • ROA can be broken down into margin and turnover • Gain insight into planning for profit improvement • Improve margin • Improve turnover • Improve both! MB 664 UVG-TAMU May 2009

Improve Margin • Reducing expenses • Using less costly materials • Automation to improve productivity • Review fixed costs (advertising, R&D, management development programs, etc.) • Raising prices • Requires pricing power • Also requires brand loyalty • Easier for firms with unique high-quality goods or services MB 664 UVG-TAMU May 2009

Improve Turnover • Increase sales while holding investment in assets relatively constant • Dispose of obsolete and redundant assets • Speed up collections of receivables • Evaluate credit terms and policies • Identify unused fixed assets • Use idle cash to repay outstanding debts or invest in profit-producing activities MB 664 UVG-TAMU May 2009

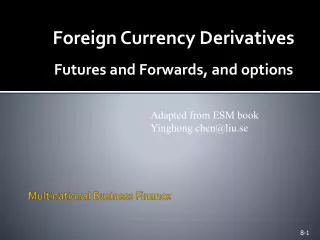

Cost of goods sold Selling expenses Administrative expenses Cash Accounts receivable Inventories Marketable securities Other current assets Land Buildings Machinery Equipment MB 664 UVG-TAMU May 2009

Cost of goods sold Selling expenses Administrative expenses Total cost Cash Accounts receivable Inventories Marketable securities Other current assets Current assets Land Buildings Machinery Equipment Fixed assets MB 664 UVG-TAMU May 2009

Sales Net income Cost of goods sold Selling expenses Administrative expenses Total cost Cash Accounts receivable Inventories Marketable securities Other current assets Current assets Total assets Land Buildings Machinery Equipment Fixed assets MB 664 UVG-TAMU May 2009

Sales Net income Net profit margin Cost of goods sold Selling expenses Administrative expenses Total cost ÷ Sales Cash Accounts receivable Inventories Marketable securities Other current assets Sales Current assets Total asset turnover ÷ Total assets Land Buildings Machinery Equipment Fixed assets MB 664 UVG-TAMU May 2009

Sales Net income Net profit margin Cost of goods sold Selling expenses Administrative expenses Total cost ÷ Sales ROA × Cash Accounts receivable Inventories Marketable securities Other current assets Sales Current assets Total asset turnover ÷ Total assets Land Buildings Machinery Equipment Fixed assets MB 664 UVG-TAMU May 2009

Sales Net income Net profit margin Cost of goods sold Selling expenses Administrative expenses Total cost ÷ Sales ROA × Cash Accounts receivable Inventories Marketable securities Other current assets Sales Current assets Total asset turnover ÷ Total assets Land Buildings Machinery Equipment Fixed assets The Du Pont formula MB 664 UVG-TAMU May 2009

Modified Du Pont Formula Use of borrowed funds can magnify returns to equity. To see this Consider the following definitions: ROE = Net income ÷ Equity or ROE = (Net income ÷ Total assets) × (Total assets ÷ Equity) or ROE = ROA × Equity multiplier where: Equity multiplier = Total assets ÷ Equity or Equity multiplier = 1 ÷ (1 – Debt ratio) MB 664 UVG-TAMU May 2009

An Example Assume the following values: Sales (S) = $50,000 Net income (NI)= $18,000 Total assets (TA) = $100,000 Equity (E) = $45,000 Using the previous definitions: ROE = NI ÷ E = $18,000 ÷ $45,000 = 40% Equity multiplier = TA ÷ E = $100,000 ÷ $45,000 = 2.22 or Equity multiplier = 1 ÷ (1 – Debt ÷ TA) = 1 ÷ (1 – .55) = 2.22 ROE = NI ÷ TA × Equity multiplier = 18% × 2.22 = 40% MB 664 UVG-TAMU May 2009

Continuation of Example If the firm used only equity to fund its operation, the ROE and ROA would be identical, or: ROE = NI ÷ E = $18,000 ÷ $100,000 = 18% ROA = NI ÷ TA = $18,000÷ $100,000 = 18% However, 45% of the firm’s capital was supplied by creditors, so: Equity multiplier = 1 ÷ (1 – Debt ÷ TA) = 1 ÷ (1 – .55) = 2.22 ROE = NI ÷ TA × Equity multiplier = 18% × 2.22 = 40% This illustrates the potential benefitsto the use of leverage. MB 664 UVG-TAMU May 2009

Another Example Consider two firms each having $800,000 in total assets but one firm having debt of $400,000, or Firm A Firm B Total assets $800,000 $800,000 Total debt 0 400,000 Equity 800,000 400,000 Each firm has an operating income or EBIT of $300,000 but firm B has interest expenses of $40,000, so: Operating income $300,000 $300,000 Interest expense 0 40,000 Profit before taxes 300,000 260,000 Taxes at 30% 90,000 78,000 Net Income $210,000 $182,000 MB 664 UVG-TAMU May 2009

Continuation of Example The rate of return on equity for these two firms therefore would be: Firm A Firm B Total assets $800,000 $800,000 Total debt 0 400,000 Equity 800,000 400,000 Net Income $210,000 $182,000 ROE 26.25% 45.5% Conclusion: Although the absence of debt allows firm A to register higher profit after taxes, the owner(s) of firm B earn a significantly higher return on equity capital invested in the firm. MB 664 UVG-TAMU May 2009

DuPont formula Summary Because it links several critical ratios, the DuPont formula allows you to examine how a firm generates its ROE. NI = net income NPM = net profit margin = NI ÷ sales TA = total assets EM = equity multiplier = 1 ÷ (1 – debt ratio) TAT = total asset turnover = sales ÷ TA ROE = NPM × TAT × EM or ROE = (NI ÷ TA) × EM MB 664 UVG-TAMU May 2009

DuPont formula Summary Because it links several critical ratios, the DuPont formula allows you to examine how a firm generates its ROE. NI = $18,000 NPM = net profit margin = NI ÷ S = 0.36 TA = $100,000 EM = equity multiplier = 1 ÷ (1 – debt ratio) = 2.22 TAT = total asset turnover = S ÷ TA = 0.5 ROE = NPM × TAT × EM = .36 × .5 × 2.22 = .40 or ROE = (NI ÷ TA) × EM = .18 × 2.22 = .40 MB 664 UVG-TAMU May 2009

Analyzing DuPont formula A firm is said to be in a sound financial condition if: It has a high net profit margin (NPM), which signals strong operating management. It has a high total asset turnover (TAT), which signals strong asset management, It has a low equity multiplier (EM), which signals strong capital management in the presence of low and stable cost of debt capital. MB 664 UVG-TAMU May 2009