Download

1 / 27

270 likes | 455 Views

CENTRAL ASIA MICRO FINANCE ALLIANCE. December, 2006. CENTRAL ASIA MICRO FINANCE ALLIANCE. USAID funded 3 - year project, continuation of CAMFA I project. Objective:

E N D

CENTRAL ASIA MICRO FINANCE ALLIANCE December, 2006

CENTRAL ASIA MICRO FINANCE ALLIANCE • USAIDfunded 3-yearproject, continuation of CAMFA I project. • Objective: • To increase the range and enhance the outreach of financial services to micro and small businesses, especially in rural and isolated regions of Kyrgyzstan.

CAMFA II: 3 COMPONENTS • I: Continue support the development of 4 Microfinance Associations in Central Asia region • II: Continue support of Frontiers, a wholesale lender for small and very small financial institutions in Central Asia • III: Promote Agricultural Finance in Kyrgyzstan

COMPONENT I • To increase the capacity and sustainability of national Microfinance Associations (MFAs).

COMPONENT I • MFA Capacity building • Improve the policy and regulatory environment for microfinance • Increase availability of microfinance training and specialized technical assistance • Support standards development and increased financial transparency

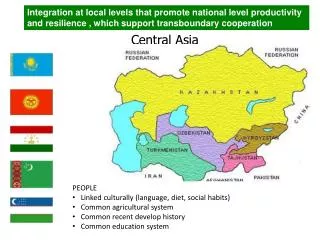

COMPONENT I • PARTNERS: • AMFOK – Kazakhstan (May 2004) • AMFOT – Tajikistan (Feb 2005) • MTA – Uzbekistan (July 2005) • AMFI – Kyrgyzstan (Dec 2005) • Regional Network (July 2006)

COMPONENT I SUPPORT TO MFAS FOR: • Lobby government • Gain access to new technical approaches • Best practice information in Russian • Hands-on experience at best practice MFIs • New information technologies and support • Networking and sharing regional experiences • Reporting to the MixMarket • Social impact tools and research • Commercial financing options

COMPONENT I • MFA CAPACITY BUILDING • Improving Governance • Strategic planning / Operations • Membership driven service delivery • Increased MFA Financial Sustainability • Human Resource Development • Enhanced External Relations

COMPONENT I • COUNTRY SPECIFIC ACTIVITIES • Credit Bureau in Tajikistan • Legal assistance to MFI in Uzbekistan

COMPONENT I • ACHIEVEMENTS: • MF law in Uzbekistan (Sept’06) • Tax benefits for MFIs in Uzbekistan (Jan’06) • Loan size cap for MFIs in Kazakhstan (Nov’06) • MFI Reporting to NBT in Tajikistan (Apr’06) • MF midterm strategy participation in Kyrgyzstan

COMPONENT I • REGIONAL NETWORK • Regional MOU between the 4 MFAs in May 2006 • AMFOT – in 2007 will take the responsibility for regional coordination hub

COMPONENT I • REGIONAL NETWORK • Coordination of activities • Information sharing • Trainings • Donor/ commercial funding

COMPONENT II • FRONTIERS SUPPORT • To increase MFI access to wholesale lending

COMPONENT II • Institutional development of Frontiers • Facilitate expansion of Frontiers loan portfolio and outreach to MFIs in Central Asia region. • Continue diversification of Frontiers’s sources of funds through increased leveraging of its capital.

COMPONENT III • Expanding Ag Financial Services: • TA and mini-grants to MFI, CU, Ag Coop. and commercial banks for innovative products and new lending methodologies • Rural Finance window at Frontiers (on-lending fund) • OBJECTIVE: Improving access to demand driven and sustainable rural and agricultural financial services

COMPONENT III • Two main motivations • Agriculture sector remains a leading economic sector for Kyrgyzstan; main exporter and major employer • Improved financial markets can accelerate agricultural and rural growth, increasing food security, poverty reduction and conflict resolution

COMPONENT III • Specialized technical assistance services • Small grants program • Disseminate best practices in rural finance • Access to credit through Frontiers • Support pilot activities for innovative financial services

COMPONENT III • Lending for agricultural production • Lending for animal husbandry • Lending for agro-processing, that operate in rural areas • Fixed Asset purchases for farm equipment and agricultural processing (including leasing) • Loans that support improved technologies for handling, storage and marketing of agricultural products • Loans that support rural enterprises for competitive packaging and labeling and branding of products

COMPONENT III • Challenges and Opportunities in Rural Financial Market • High transactions costs for lenders and borrowers • High risks faced by borrowers and savers due to natural disasters and limited tools to manage risks • Lack of reliable information • Lack of adequate collateral • Inhospitable legal and regulatory framework

COMPONENT III Key Assumptions • Improving economic opportunities in rural areas leads to improvement in agricultural productivity • The financial services should be tailored specifically to rural households, rural enterprises and Ag. sector • Need to improve the ability of existing financial institutions to deliver appropriate rural and Ag. Financial services

COMPONENT III • Serving clients at a distance - managing high transaction costs • Management loans at a distance - decentralization of loan approval authority • Ag lending specific: • Seasonality of agricultural production • Loan terms structured around cash flow and crop cycles • Loan application assessments require substantial knowledge of local crops, crop prices, yields and farming methods

COMPONENT III • Dealing with risks in rural financial services • Need for non-conventional lending methodologies • Alternative (creative) collateral and term conditions

RURAL FINANCE: Financial services used in rural areas by people of all income levels AGRICULTURAL FINANCE: Financing of agriculture-related activities, from production to market MICROFINANCE: Financial services for poor and low-income people Financial Markets Rural Micro Financial Services in Rural Areas Agricultural

COMPONENT III • TA for Financial intermediaries for new product development, cash flow lending, savings, etc. • Building long term capacity by TA and incentives to increase the provision of agricultural finance services

COMPONENT III • TA to selected financial institutions: competitive system based on commitment and potential for increased outreach • Policy and regulatory reforms

Financial Sector Challenges • Elevated perceptions of risk, based on past negative experiences • Weak systems of land titling, collateral laws and judiciaries • Long time process for accepting innovative loan products and practices • Information imbalance • Need for donor effort coordination

Thank you! ACDI/VOCA Kyrgyzstan Bishkek, 720011 55, Suyunbaeva Street Tel: (996 312) 68-16-08, 68-15-57 Fax: (996 312) 68-17-21 E-mail: office@camfa.kgWeb cite: www.acdivoca.org