Download

1 / 211

2.12k likes | 2.29k Views

P a g e | 1 Inter n atio na l A s s oci a t ion of R isk a nd Co mpl i a n c e Pr o f e s s io na l s ( I A RCP) 12 0 0 G St re e t N W Su i t e 8 0 0 W a s h i ng t o n, D C 2 000 5 - 67 0 5 U SA T e l : 2 0 2 - 44 9 - 9750 www .ri s k - c ompl i ance-a ss o c i a tion . c om.

E N D

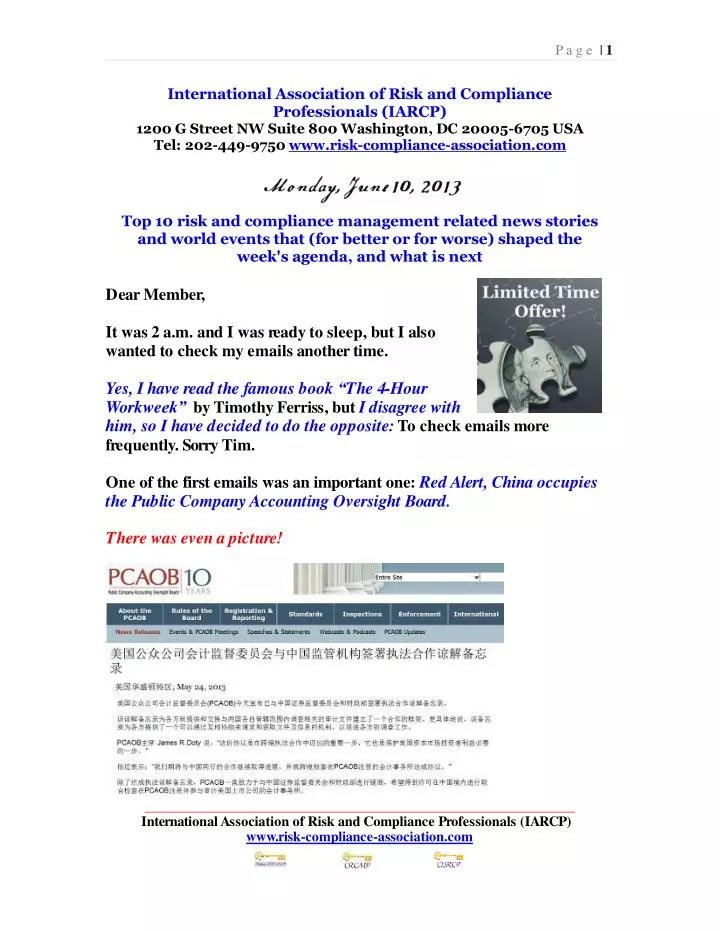

P age |1 InternationalAssociationofRiskandComplianceProfessionals(IARCP) 1200GStreet NWSuite800Washington,DC20005-6705USATel:202-449-9750www.risk-compliance-association.com Top10riskandcompliancemanagementrelatednewsstoriesandworldeventsthat(forbetterorforworse)shapedthe week'sagenda,andwhatisnext DearMember, Itwas2a.m.andIwasready tosleep,butIalsowantedtocheckmyemailsanothertime. Yes,Ihavereadthefamousbook“The4-HourWorkweek”byTimothyFerriss,butIdisagreewith him,soIhavedecidedtodothe opposite:Tocheck emailsmorefrequently.SorryTim. Oneofthefirstemailswasanimportantone:RedAlert,ChinaoccupiesthePublicCompanyAccountingOversightBoard. Therewasevenapicture! InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |2 What? IknowthatChinaimplementsaChineseSarbanes-Oxley…butwhatisthatnow? Iread inthepicturethatPCAOB主席JamesR.Doty说:“这份协议是 在跨境执法合作中迈出的重要一步,它也是保护美国资本市场投资者 利益必要的一步。” What?IsJamesR.Dotywell? Fortunately,Jamesisverywell.Therewasnoredalert.Oneofmyfriends,John,andattorney,sentmethisemail. Readmoreabout说:这份协议是在跨境执法合作中迈出的重要一步, 它也是保护美国资本市场投资者利益必要的一步atnumber7ofourlistbelow. Thefollowingmorning,Ireceivedanotheremail. Title:“Forecastingis theartofsayingwhatwillhappen,andthenexplainingwhyitdidn't” Message:Ihateyou.Ourbossisfollowingyourstresstestingrecommendations.Lao Tzuhassaidthatthosewhohaveknowledgedon'tpredict.Thosewho predict,don'thaveknowledge. Signature:Terminator Terminator? ArnoldSchwarzenegger,didyousendthisemail? Who?LaoTzu?TheChineseagain?Ireplied! “DearArnold(orotherTerminator), InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |3 Itisnotme!ItisBaseliiithatasksforaforward-lookingperspective!Baseliiirequiresstresstesting.And,wehaveacrystalballinriskmanagement:TherecommendationsoftheFinancialStabilityBoard(FSB).” Therecommendations… Whoreadstheserecommendations?Soimportant...Ihaveledsome classessinceJanuary,nobodyreadsFSB. TheylaughwhenIsayreadFSBeverymorning,beforereadingFTor WSJ! ItistimetoreadtherecommendationsoftheFSBcarefully.Itisabout theboard,seniormanagement,risk officers,complianceofficers,internalandexternalauditors. ThisisourNumber1.Thesepagesaresoimportant.Welcome totheTop10list. BestRegards, GeorgeLekatisPresidentoftheIARCP GeneralManager,ComplianceLLC 1200GStreetNWSuite800,WashingtonDC20005,USATel:(202)449-9750 Email:lekatis@risk-compliance-association.com Web:www.risk-compliance-association.comHQ:1220N.MarketStreetSuite804,WilmingtonDE19801,USA Tel:(302)342-8828 InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |4 ThematicReviewonRiskGovernancePeerReviewReport FinancialStabilityBoard(FSB)memberjurisdictionshavecommitted,undertheFSBCharterandintheFSBFrameworkforStrengtheningAdherencetoInternationalStandards,toundergoperiodicpeerreviews. Tofulfilthisresponsibility,theFSBhasestablishedaregularprogrammeofcountryandthematicpeerreviewsofitsmemberjurisdictions. ThematicreviewsfocusontheimplementationandeffectivenessacrosstheFSBmembershipofinternationalfinancialstandardsdevelopedbystandard-settingbodiesandpoliciesagreedwithintheFSBinaparticularareaimportantforglobalfinancialstability. KeynoteLuncheonSpeech By CommissionerElisseB.Walter U.S. SecuritiesandExchangeCommission 32ndAnnualSECand FinancialReportingInstituteConference,Pasadena,CA BackgroundonthePCAOB StevenB.Harris,BoardMemberKennesawStateGraduateStudentMeetingWashington,DC InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |5 FinancialConglomeratesDirectiveTechnicalReview ThisPrudentialRegulationAuthority(PRA) policystatementpublishesthefinalrulesimplementingtheFinancialConglomerates DirectiveTechnicalReview(2011/89/EC)(FICOD1)whichamendstheFinancialConglomeratesDirective(2002/87/EC)andcertainother Directivesinsofarastheyapplytofinancialconglomerates. CommitteeontheGlobalFinancialSystemCGFSPapersNo49 Assetencumbrance,financialreformandthedemandforcollateral assets ReportsubmittedbyaWorkingGroupestablishedby theCommitteeontheGlobalFinancialSystem TheGroupwaschairedbyAerdtHouben,NetherlandsBank Giventhatthedemandforcollateralassetsisincreasing,theCommitteeontheGlobalFinancialSystem(CGFS) in May2012establishedaWorkingGroup(chairedbyAerdtHouben,NetherlandsBank)toexploretheimplicationsofthistrendformarketsandpolicy. ThisreportpresentstheGroup’sfindingsfromasystem-wideperspectiveanddrawsbroadconclusionsforpolicymakers. Thereportpresentsevidenceofincreasedreliancebybanksoncollateralisedfundingmarketsinrecentyearsforsomeregions,withtheincreasebeingmostpronouncedinEurope. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |6 PeerReviewofSwitzerlandReviewReport FSBcountrypeerreviews TheFSBhasestablishedaregularprogrammeofcountrypeerreviewsofitsmemberjurisdictions. The objectiveofthereviewsistoexaminethestepstakenorplannedbynationalauthoritiestoaddressInternationalMonetaryFund(IMF)-WorldBankFSAP recommendationsconcerningfinancialregulationandsupervisionaswellasinstitutionalandmarketinfrastructure. PCAOBEntersintoEnforcementCooperationAgreementwithChineseRegulators The PublicCompanyAccountingOversightBoardannouncedthatithasenteredintoaMemorandumofUnderstanding(MOU)onEnforcementCooperationwiththeChinaSecuritiesRegulatoryCommission(CSRC)andtheMinistryofFinance(MOF). TheMOUestablishesacooperativeframeworkbetweenthepartiesfortheproductionandexchangeofauditdocumentsrelevanttoinvestigationsinbothcountries’respectivejurisdictions. Morespecifically,itprovidesamechanismforthepartiestorequestandreceivefromeachotherassistancein obtainingdocumentsandinformationinfurtheranceoftheir investigativeduties. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |7 Islamiccommerceandfinance OpeningremarksbyDrMichaelGondwe,GovernoroftheBankofZambia,attheworkshopon“Islamiccommerceandfinance”,Lusaka. Threequestionsonthenatureandmanagementofrisk KeynotespeechbyMrNormanTLChan,ChiefExecutiveoftheHongKongMonetaryAuthority,at theHongKongMonetaryAuthority-GlobalAssociationofRisk Professionals(GARP)GlobalRiskForumOpeningDinner,HongKong. InvestorProtectionThroughEconomicAnalysis ByCraigM.Lewis,ChiefEconomistandDirector DivisionofRisk,Strategy,andFinancialInnovation,U.S.SecuritiesandExchangeCommission SpeechatthePennsylvaniaAssociationofPublicEmployeeRetirementSystemsAnnualSpringForumHarrisburg,PA InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |8 ThematicReviewonRiskGovernance PeerReviewReportForeword FinancialStabilityBoard(FSB)memberjurisdictionshavecommitted,undertheFSBCharterandintheFSBFrameworkforStrengtheningAdherencetoInternationalStandards,toundergoperiodicpeerreviews. Tofulfilthisresponsibility,theFSBhasestablishedaregularprogrammeofcountryandthematicpeerreviewsofitsmemberjurisdictions. ThematicreviewsfocusontheimplementationandeffectivenessacrosstheFSBmembershipofinternationalfinancialstandardsdevelopedbystandard-settingbodiesandpoliciesagreedwithintheFSBinaparticularareaimportantforglobalfinancialstability. Thematicreviewsmayalsoanalyse otherareasimportantforglobalfinancialstabilitywhereinternationalstandardsorpoliciesdonotyetexist. The objectivesofthereviewsaretoencourageconsistentcross-countryandcross-sectorimplementation;toevaluate(wherepossible)theextent towhichstandardsandpolicieshavehadtheirintendedresults;and toidentifygapsandweaknessesinreviewedareasandtomakerecommendationsforpotentialfollow-up(includingviathedevelopmentofnewstandards)byFSBmembers. Thisreportdescribes thefindingsofthethematicpeerreviewonriskgovernance,includingthekeyelementsofthediscussionintheFSBStandingCommitteeonStandardsImplementation(SCSI). InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |9 ThedraftreportfordiscussionwaspreparedbyateamchairedbySweeLianTeo(MonetaryAuthorityofSingapore),comprisingTedPrice(CanadaOfficeoftheSuperintendentofFinancialInstitutions),XiangQi(ChinaBankingRegulatoryCommission),JérômeLachand(FranceAutoritédeContrôlePrudentiel),SofiaNikopoulos(GermanBaFin),AdrianaElizondo(MexicoNationalBankingandSecuritiesCommission),FranciscoGil(BankofSpain),Mike Brosnan(UnitedStatesOfficeoftheComptrolleroftheCurrency),Xavier-Yves Zanota(memberoftheBaselCommitteeonBankingSupervisionSecretariat),MatsIsaksson(OrganisationforEconomicCo-operationandDevelopment),andLauraArd(WorldBank). Merylin CoombsandGraceSone(FSBSecretariat)providedsupport totheteamandcontributed to thepreparationofthepeerreviewreport. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |10 Executivesummary Therecentglobalfinancialcrisisexposedanumberofgovernanceweaknessesthatresultedin firms’failure to understandtheriskstheyweretaking. In thewakeofthecrisis,numerousreportspaintedafairlybleakpictureofriskgovernanceframeworksatfinancialinstitutions,whichconsistsofthethreekeyfunctions: Theboard,thefirm-widerisk managementfunction,andtheindependentassessmentofrisk governance. Thecrisishighlightedthatmanyboardshaddirectorswithlittlefinancialindustryexperienceandlimitedunderstandingoftherapidlyincreasingcomplexityoftheinstitutionstheywereleading. Toooften,directorswereunabletodedicatesufficienttimetounderstandthefirm’sbusinessmodelandtoodeferentialtoseniormanagement. In addition,manyboardsdidnotpaysufficientattention to riskmanagementorsetupeffectivestructures,suchasadedicatedriskcommittee,tofacilitatemeaningfulanalysisofthefirm’sriskexposuresandtoconstructivelychallengemanagement’sproposalsanddecisions. Theriskcommitteesthatdidexistwereoftenstaffedbydirectorsshorton bothexperienceandindependencefrommanagement. Theinformationprovidedtotheboardwasvoluminousandnoteasily understoodwhichhamperedtheabilityofdirectors to fulfiltheirresponsibilities. Moreover,mostfirmslackedaformalprocesstoindependentlyassesstheproprietyoftheirriskgovernanceframeworks. Withouttheappropriatechecksandbalancesprovidedbytheboard,theriskmanagementfunction,andindependentassessmentfunctions,a InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |11 cultureofexcessiverisk-takingandleveragewasallowed topermeateintheseweaklygovernedfirms. Further,withtheriskmanagementfunctionlackingtheauthority,statureandindependencetoreininthefirm’srisk-taking,theabilityto addressanyweaknessesinrisk governanceidentifiedbyinternalcontrolassessmentandtestingprocesseswasobstructed. Thepeerreviewfoundthat,sincethecrisis,nationalauthoritieshavetakenseveralmeasurestoimproveregulatoryandsupervisoryoversightofriskgovernanceatfinancialinstitutions. Thesemeasuresincludedevelopingorstrengtheningexistingregulationorguidance,raisingsupervisoryexpectationsfortheriskmanagementfunction,engagingmorefrequentlywiththeboardandmanagement,andassessingtheaccuracyandusefulnessoftheinformationprovided totheboardtoenableeffectivedischargeoftheirresponsibilities. Nonetheless,moreworkremains;nationalauthoritiesneedtostrengthentheirability to assess theeffectivenessofafirm’sriskgovernance,andmorespecificallyitsriskculturetohelpensuresoundrisk governancethroughchangingenvironments. Supervisorswillneed toundergoasubstantialchangein approachsinceassessingrisk governanceframeworksentailsforminganintegratedviewacrossallaspectsoftheframework. Thepeerreviewalsoaskedsupervisorstoevaluateprogressmadebytheirsurveyedfirm(s)towardenhancedrisk governanceinsevenareas. Toprovidesomeconsistencytothisexercise,thereviewteamdevelopedhigh-levelcriteriatoassistsupervisoryevaluationsoffirms’progress,drawingfromacompilationofrelevantprinciples,recommendationsandsupervisoryguidance. Thehigh-levelcriteriawereviewedasfundamentalprerequisitesforriskgovernanceframeworks. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |12 • Thisevaluationfoundthatmanyofthebestriskgovernancepracticesatsurveyedfirmsarenow moreadvancedthannationalguidance. • Thisoutcomemayhavebeenmotivatedbyfirms’needto regainmarketconfidenceratherthanregulatoryrequirements. • Firmshavemadeparticularprogressin: • assessingthecollectiveskillsandqualificationsoftheboardaswellastheboard’seffectivenesseitherthroughself-evaluationsorthroughtheuseofthirdparties; • institutingastand-alonerisk committeethatiscomposedonlyofindependentdirectorsandhavingacleardefinitionofindependence; • establishingagroup-widechiefriskofficer(CRO)andriskmanagementfunctionthatisindependentfromrevenue-generatingresponsibilitiesandhasthestature,authorityandindependencetochallengedecisionsonrisk madebymanagementandbusinesslines;and • integratingthediscussionsamongtheriskandauditcommitteesthroughjointmeetingsorcross-membership. • Althoughmanysurveyedfirmshavemadeprogressinthelastfewyears,significantgapsremain,relative tothecriteriadeveloped,particularlyinriskmanagement. • Therewerealsodifferencesinprogressacrossregionswithfirmsinadvancedeconomieshavingadoptedmoreofthedesirableriskgovernancepractices. • Theresultsofthesupervisoryevaluationsweregroupedby: • allsurveyedfirms; • firmsidentifiedbytheFSBandBaselCommitteeonBankingSupervision(BCBS)asglobalsystemicallyimportantfinancialinstitutions,orG-SIFIs;and InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |13 • (iii)firmsthatresideinadvancedeconomies(AEs)oremergingmarketanddevelopingeconomies(EMDEs). • In summary,acrossthesevenareasevaluated,firmshavemadethemostprogressindefiningtheboard’sroleandresponsibilities,andreasonableprogressintheirapproachtorisk governanceandtheindependentassessmentofrisk governance. • Thesupervisoryevaluations,however,indicatethatsurveyedfirmsshouldcontinuetoworktowarddefiningtheresponsibilitiesoftheriskcommitteeandstrengtheningtheirriskmanagementfunctionsasnearly 50percentofsurveyedfirmsdidnotmeetalloftheevaluationcriteria intheseareas. • Bytypeof institution,surveyedG-SIFIsaremoreadvancedthanotherfinancialinstitutionsin definingtheresponsibilitiesoftheboardandriskcommittee,conducting independentassessmentsofriskgovernance,providingrelevantinformationtotheboardandrisk committee,andtosomeextentmoreadvancedintheriskmanagementfunction. • Theseresultssupport thefindingthatthefirmsintheregionshardesthitbythefinancialcrisishavemadethemostprogress. • Meanwhile,supervisoryevaluationsoffirmsthatresideinEMDEsshowthatnearly65percentdidnotmeetallofthecriteriafortheriskmanagementfunction. • Thesegapsneedimmediateattentionbybothsupervisorsandfirms.Othersignificantfindingscomingoutofthereviewincludethefollowing: • Nationalauthoritiesdonotengageonasufficientlyregularandfrequentbasiswiththeboard,risk committeeandauditcommittee. • Severaljurisdictionshold suchmeetingsonlyonceayearoronanas-neededbasis. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |14 • GoodprogresshasbeenmadetowardelevatingtheCRO’sstature,authority,andindependence. • In manyfirms,theCROhasadirectreportinglinetothechiefexecutiveofficer(CEO)andarolethatisdistinctfrom otherexecutivefunctionsandbusinesslineresponsibilities(e.g.,no“dual-hatting”). • Thiselevation,however,needstobesupportedbytheinvolvementoftheriskcommitteeinreviewingtheperformanceandsettingtheobjectivesoftheCRO,ensuringthattheCROhas accesstotheboardandriskcommitteewithoutimpediment(includingreportingdirectlyto theboard/riskcommittee),andfacilitatingperiodicmeetingswithdirectorswithoutthepresenceofexecutivedirectorsorothermanagement. • Moreworkisneededonthepartofbothnationalauthoritiesandfirmsonestablishinganeffectiverisk appetiteframework(RAF). • Assessingafirm’sRAFisachallengingtaskthatrequiresgreaterclarityandanelevatedlevelofconsistency amongnationalauthorities. • Supervisoryexpectationsfortheindependentassessmentofinternalcontrolsystemsbyinternalauditorother independentfunctionwerewell-establishedpriortothecrisis. • Assuch,thisisanarea thatdemonstratedrelativelysoundpracticesacrosstheFSBmembershipatbothnationalauthoritiesandfirms. • However,nojurisdictionhadspecificexpectationsfor internalaudit toperiodicallyprovideafirm-wideassessmentofriskmanagementorriskgovernanceprocesses. • Nearlyallfirmshaveanindependentchief auditexecutive(CAE)whoreportsadministrativelytotheCEO andtheauditcommitteechairandwhodirectlyreportsauditfindings to apermanentauditcommittee. • However,thereisstillroomforimprovingtheCAE’saccesstodirectorsbeyondthoseontheauditcommittee. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |15 Drawingfromthefindingsofthereview,includingdiscussionswithindustryorganisationsaswellasrisk committeedirectorsandCROsofseveralfirmsthatparticipatedinthereview,thereportidentifiessomeofthebetterpracticesexemplifiedbynationalauthoritiesandfirms to collectivelyformalistofsoundrisk governancepractices. Italsodrawsonsomeoftherelevantprinciplesandrecommendationsforriskgovernancepublishedbyotherorganisationsandstandardsettingbodies. Noonesingleauthorityorfirm,however,demonstratedallofthesesound practices. Thisintegratedandcoherentlistofsoundpracticesaimstohelpnationalauthoritiestakeamoreholisticapproach to riskgovernance,ratherthanlookingat eachfacet in isolation,andmayprovideabasisforconsiderationbyauthoritiesandstandardsettingbodiesastheyreviewtheirguidanceandstandardsforstrengtheningriskgovernancepractices. Thereviewsetsoutseveralrecommendations to ensuretheeffectivenessofriskgovernanceframeworkscontinuetoimprovebytargetingareaswheremoresubstantialworkisneeded. Whilethereviewfocusedonbanksandbroker-dealersthataresystemicallyimportant,theserecommendationsapply to othertypesoffinancialinstitutions,includinginsurersandfinancialconglomerates. Recommendations: 1.Toensurethatfirms’risk governancepracticescontinuetoimprove,FSBmemberjurisdictionsshouldstrengthentheirregulatoryandsupervisoryguidanceforfinancialinstitutions,inparticularforSIFIs,and devoteadequateresources(bothinskillsandquantity)toassesstheeffectivenessofriskgovernanceframeworks. In particular,nationalauthoritiesshouldconsiderthefollowingsoundriskgovernancepractices: InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |16 Setrequirementsontheindependenceandcompositionofboards,includingrequirementsonrelevanttypesofskillsthattheboard,collectively,shouldhave(e.g.,risk management,financialindustryexpertise)aswellasthetimecommitmentexpected. Holdtheboardaccountableforitsoversightofthefirm’sriskgovernanceandassessifthelevelandtypesofriskinformationprovidedtotheboardenableeffectivedischargeofboardresponsibilities. Boardsshouldsatisfythemselvesthattheinformationtheyreceivefrommanagementandthecontrolfunctionsiscomprehensive,accurate,completeandtimelyto enableeffectivedecision-makingonthefirm’sstrategy,risk profileandemergingrisks. Thisincludesestablishingcommunicationproceduresbetweentheriskcommitteeandtheboardandacrossotherboardcommittees,mostimportantlytheauditandfinancecommittees. SetrequirementstoelevatetheCRO’sstature,authority,andindependenceinthefirm. ThisincludesrequiringtheriskcommitteetoreviewtheperformanceandobjectivesoftheCRO,ensuringtheCROhasunfetteredaccesstotheboardandrisk committee(includingadirectreportinglinetotheboardand/orriskcommittee),andexpectingtheCROtomeetperiodicallywithdirectorswithoutexecutivedirectorsandmanagementpresent. TheCRO shouldhaveadirectreportingline totheCEOandadistinctrolefrom otherexecutivefunctionsandbusinesslineresponsibilities(e.g.,no“dual-hatting”). Further,theCROshouldbeinvolvedinactivitiesanddecisions(fromariskperspective)thatmayaffectthefirm’sprospectiverisk profile(e.g.,strategicbusinessplans,newproducts,mergersandacquisitions,internalcapitaladequacyassessmentprocess,orICAAP). InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |17 Requiretheboard(orauditcommittee)toobtainanindependentassessmentofthedesignandeffectivenessoftherisk governanceframeworkonanannualbasis. Engagemorefrequentlywiththeboard,risk committee,auditcommittee,CEO,CRO,andotherrelevantfunctions,suchastheCFO,toassessthefirm’sriskculture(e.g.,the“toneatthetop”),whetherdirectorsprovideeffectivechallengetomanagement’sproposalsanddecisions,andwhethertheriskmanagementfunctionhastheappropriateauthority to influencedecisionsthataffect thefirm’srisk exposures. Therelevantstandardsettingbodies(e.g.,BCBS,IAIS,IOSCO, OECD)shouldreviewtheirprinciplesforgovernance,takingintoconsiderationthesoundrisk governancepracticeslistedinSectionV. Risk cultureplaysacriticalrolein ensuringeffectiverisk governanceenduresthrough changingenvironments. TheFSBSupervisoryIntensityandEffectivenessgrouphasagreed toimplementtherecommendationfromthe2012FSBprogressreportonenhancedsupervision to explorewaystoformallyassessriskculture,particularlyatG-SIFIs. ThisworkshouldbecompletedbySeptember2013. To improvetheirability to assessfirms’progresstowardmoreeffectiveriskmanagement,nationalauthoritiesshouldprovideguidanceonthekeyelementsthatareincorporatedineffectiverisk appetiteframeworks. To enablefirmstodefineframeworkswithaminimumamount ofcomparabilitydespitetheirfirm-specificnature,acommonnomenclaturefortermsusedin riskappetitestatements(e.g.,“riskappetite”,“riskcapacity”,“risklimits”)shouldbeestablished. TheFSBSupervisoryIntensityandEffectivenessgroup,incollaborationwithrelevantstandardsetters,hasagreed to finalisethisworkbytheend of2013. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |18 • TheFSBshouldconsiderlaunchingafollow-upreviewonriskgovernanceafter2016(i.e.,aftertheG-SIFIpolicy measuresbegintobephasedin),to assessnationalauthorities’implementationoftherecommendationstostrengthentheirsupervisoryguidanceandoversightofriskgovernance. • ThereviewalsoshouldincludetheG-SIFIs identifiedin2014bytheFSBincollaborationwiththeBCBSandIAIS. • Introduction • Increasingtheintensityandeffectivenessofsupervision to reducethemoralhazardposedbySIFIsisakeycomponentoftheFSB’spolicymeasures,endorsedbyG20Leaders. • Sincetheonsetoftheglobalcrisis,supervisorshaveintensifiedtheiroversightoffinancialinstitutions,particularlySIFIs,soastoreducetheprobabilityoftheirfailure. • Specifically,supervisoryexpectationsofriskmanagementfunctionsandoverallrisk governanceframeworkshaveincreased,asthiswasanareathatexhibitedsignificantweaknessesinmanyfinancialinstitutionsduringtheglobalfinancialcrisis. • Whilesupervisorsareresponsibleforassessingwhetherafirm’sriskgovernanceframeworkandprocessesareadequate,appropriateandeffectiveformanagingthefirm’sriskprofile,thefirm’smanagementisresponsibleforidentifyingandmanagingthefirm’srisk. • InOctober2011,theFSBagreedtoconductathematicpeerreviewonriskgovernancetoassessprogresstowardenhancingpracticesatnationalauthoritiesandfirms(banksandbroker-dealers). • Forpurposesofthisreview,riskgovernance collectivelyrefers to theroleandresponsibilitiesoftheboard,thefirm-wideCROandriskmanagementfunction,andtheindependentassessmentoftheriskgovernanceframework(seeChart2). InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |19 • Boardresponsibilitiesandpractices:Theboardisresponsibleforensuringthatthefirmhasanappropriaterisk governanceframeworkgiventhefirm’sbusinessmodel,complexityandsizewhichisembeddedintothefirm’srisk culture. • Howboardsassumesuchresponsibilitiesvariesacrossjurisdictions. • Firm-wideriskmanagementfunction:TheCROandriskmanagementfunctionareresponsibleforthefirm’sriskmanagementacrosstheentireorganisation,ensuringthatthefirm’sriskprofileremainswithintheriskappetitestatement(RAS)asapprovedbytheboard. • Therisk managementfunctionisresponsiblefor identifying,measuring,monitoring,andrecommendingstrategiestocontrolormitigaterisks,andreportingonriskexposuresonanaggregatedanddisaggregated basis. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |20 • Independentassessmentoftheriskgovernanceframework:Theindependentassessmentofthefirm’srisk governanceframeworkplaysacrucialroleintheongoingmaintenanceofafirm’s internalcontrols,riskmanagementandriskgovernance. • Ithelpsafirmaccomplishitsobjectivesbybringingadisciplinedapproachtoevaluateandimprovetheeffectivenessofriskmanagement,controlandgovernanceprocesses. • Thismayinvolveinternalparties,suchasinternalaudit,orexternalresourcessuchasthird-partyreviewers(e.g.,auditfirms,consultants). • Thepeerreviewdidnotfocuson otherrelevantdimensionsofriskgovernance,suchasriskdisclosuresandfirm-widecompensation practices(sincetheseareashavebeencoveredbypreviousFSBpeerreviews)orrisk dataaggregation capabilitiesatbanks (sincethistopicisbeingcoveredbyataskforceoftheBCBS. • Separately,theInternationalAssociationofInsuranceSupervisors(IAIS)launchedapeerreviewattheendof2012againstitsCorePrinciplesongovernanceandriskmanagementandinternalcontrols. • Thereiscurrentlynosinglesetofprinciplesandstandardsthatcomprehensivelyaddressesandintegratesriskgovernancerequirements;however,anumberofdifferentstandardsandrecommendationsongoodgovernanceframeworksarerelevant. • Thereviewthereforedidnotassesscompliancewithanyspecific standard,butusedacompilationofexistingstandardsand recommendations(asappropriate)totakestockofriskgovernancepracticesatbothnationalauthoritiesandfirms,andtoidentifyanygapstherein. • Supervisorswereaskedtoevaluatefirms’progressandthereview teamdevelopedhigh-levelcriteriatoprovidesomeconsistencytothisexercise. • ThefindingsofthereviewwerebasedontheresponsestoquestionnairesfromFSBmemberjurisdictions11andfromthe36banks and InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |21 broker-dealersthatFSBmembersdeemedassignificantforthepurposeofthereview. SectionIItakes stockofnationalauthorities’initiatives to strengthenoversightoffirms’riskgovernanceframeworksanddescribestherangeofsupervisorypracticesin fourbroadareas: Theboardanditscommittees; Thefirm-widerisk managementfunction,includingtheCRO; Theindependentassessmentofthefirm-wideriskmanagementframeworkbyinternalauditand/orthirdparties;and Thesupervisoryassessmentofrisk governanceframeworks. SectionIIIexaminesriskgovernancepracticesatsurveyedfirmsandthechangesmadesincethefinancialcrisis. Inadditiontotheresponsestothequestionnaire,thefindingsdrawontheoutcomesofdiscussionswithindustryorganisationsaswellasriskcommitteedirectorsandCROsofseveralfirmsthatparticipatedinthereview. Nationalsupervisorswereaskedto assessfirms’progress towardenhancingkeyriskgovernancefunctions,aswellastheaccuracyandcompletenessoftheresponsesprovidedbyfirmsheadquarteredintheirjurisdiction. SectionIVsetsouttheconclusionsandrecommendationsdrawnfromthefindingsofthereview,whichisfollowedbyalistofsoundriskgovernancepracticesthatencompassanoverlayofsupervisoryexpectationsforsound practicesatfirms. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |22 • II.Nationalauthorities’oversightofriskgovernancepractices • Sincethefinancialcrisis,nationalauthoritieshaveincreasedtheirsupervisoryfocusonrisk governance,whichisacriticalelementforpromotingamoreresilientfinancialsystem. • Underpinningtherangeofreformsis theissuancein 2010oftheBCBSPrinciplesforEnhancingCorporateGovernanceandtheOECDpublicationonCorporateGovernanceandtheFinancialCrisis– ConclusionsandEmergingGoodPractices. • Someofthenotablechangesembeddedinregulatoryandsupervisoryguidanceinclude: • introducingexplicitrequirementsfortheestablishmentofariskcommittee; • conveyingexpectationstostrengthentherisk managementfunction,includingthestatureandqualificationsoftheCRO; • introducingadditionalrequirementsforriskgovernanceatSIFIs; • enhancingthemandateandresourcesofsupervisoryauthoritiesinrelationtorisk governanceoversight; • increasingtheintensityofengagementbetweenthesupervisorandtheboardandseniormanagementonrisk governanceissues;and • adjustingthesupervisoryrisk assessmentprocess,particularlyincreasingthefocusonriskgovernanceacrossdifferentbusinessmodels. • AnnexCprovidesmoredetailsontheinitiativesFSBmembershavetakentostrengthenoversightofrisk governancepractices,includingimplementationofotherrelevantprinciplessuchastheFSBprinciplesforsoundcompensationpracticesandrecommendationsputforwardinthe2009reportbytheSeniorSupervisorGroup(SSG)onriskmanagementpracticesduringthefinancialcrisis. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |23 • Whilesupervisoryguidancehasimproved,progresshasbeenuneven acrossthefunctionsthatcollectivelyformtheriskgovernanceframework. • Basedonthefindingsfromthereview,someareaswheremoresupervisoryrequirementsand/orguidancewouldbeusefulinclude: • Acleardefinitionofindependencewhichisseparatefromnon-executivedirector; • Theestablishmentofastand-aloneriskcommitteethatiscomposedofindependentdirectors; • Thelevelandtypesofriskinformationfirmsshouldprovideaswellasthefrequencyofriskreporting; • Thekeyfeaturesofaneffectiverisk appetiteframeworktohelpsupervisoryevaluations;and • Thewaysinternalauditcanprovidefeedbackonwhetherafirm’sriskgovernanceprocessesarekeepingpacewithtrendsand/oralignwith bestpractices. • Thenextfoursub-sectionssummariseexistingsupervisoryexpectationsforthethreekeyriskgovernancefunctionsandexamineauthorities’approachestoassessingtheimplementationofsupervisoryexpectations. • 1.Theboardandits committees • RegulatoryandsupervisoryguidancespecifyingtheroleandresponsibilitiesoftheboardareprevalentacrosstheFSBmembership,includingamongotherthingsforriskgovernance. • Akeyresponsibilityoftheboardis to approve thefirm’soverallbusinessstrategyandRAF. • Assuch,theboardhasultimateresponsibilityforthefirm’sriskmanagement,includingsettingtheriskcultureofthefirmandoverseeingmanagement’simplementationoftheagreedbusinessstrategy. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |24 Toensurethatboardsarefocusedonthehigher-levelstrategicandriskissues,supervisorsareengagingmorefrequentlywiththeboardinparticularwithindependentdirectors. Thedefinitionofwhatconstituteseffectiverisk governanceisevolving,however,supervisorshighlighttheimportanceoftheboardsettingthe“toneatthetop”inregardtothefirm’sstrategyandrisk cultureandchallengingmanagementontheadherencetotheagreedriskappetite. 1.1Boardcomposition Theleadershipstructuretooverseethefirm’srisk managementvariesacrossjurisdictions. Mostjurisdictionsrequire theestablishmentofapermanentauditcommittee,whichhasalongerhistorythanotherboardsub-committees,drivenbyrequirementsfromsecuritiesregulatorstoprovideassurance tothequalityofthefinancialinformationprovidedbyregisteredfinancialinstitutions. Assuch,morespecificregulatoryandsupervisoryrequirementsforthecompositionandindependenceoftheauditcommitteearesetoutthanfortherisk committee. Forexample,anumberofjurisdictionsrequiretheauditcommitteetocompriseamajorityofindependentornon-executivedirectors,severaljurisdictionsrequiretheauditcommitteechairtobeindependent(or insomecasesanon-executive),andinafewjurisdictionstheparticipationofthechairoftheboardisrestricted. Theestablishmentofastand-alonerisk committeeislessprevalentandtherequirementtypicallyapplies to large,complexfinancialinstitutions(e.g.,firmswithmanylegalentitiesand/orcross-borderoperations). Wherestand-alonerisk committeesexist,severaljurisdictions19requireriskcommitteememberstohaveexpertisein risk-relateddisciplinesandonlyafewjurisdictionsrequireaminimumnumberofindependentdirectors. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |25 • In HongKong, however,forthcomingchangeswillrequireall,orthemajority,ofthemembersoftherisk committeetobenon-executivedirectors. • AnnexDprovidesfurtherdetailsontheregulatoryandsupervisoryguidanceforthecompositionoftheboardandsub-committees,butsomeofthekeyfeaturesinclude: • Independence:Manyjurisdictionshaveestablishedgeneral requirementsconcerningtheindependenceoftheboard to ensurethat thereisobjectivejudgementanddecision-makingontheboard. • Manyjurisdictionsalsosetoutquantitativeminimumsforthenumberofindependentdirectorsontheboard. • Some otherjurisdictionsonlysetquantitativeminimumsforthenumberofnon-executivedirectorswhichdoesnotnecessarilyensureindependentjudgementontheboard. • Expertise:Regardlessoftheboardstructure,theboardneeds tocomprisememberswhocollectivelybringabalanceofexpertise,skills,experienceandperspectiveswhileexhibitingtheobjectivitytoensuredecisionsarebasedonsoundjudgementandthoughtfuldeliberations. • Manyjurisdictionsconductperiodicreviewsoftheperformance,trainingandskillsneededintheboardandrisk committee. • Requiringspecificskillsforalldirectorsareacommonpractice(usuallysubsumedin“fitandproper”tests)andtypicallyincluderelevantknowledge,experienceandskillsin financeand/orbusiness. • Severaljurisdictionsnotonlylookatindividualqualificationsbutalsotakeaholisticviewoftheboard,examiningtheircollectiveskillsandqualifications. • In additiontohavingcertainskillsandqualifications,somejurisdictionsrequiredirectors tohave thecapacity todedicatesufficienttimeand InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |26 energyinreviewinginformationanddevelopinganunderstandingofthekeyissuesrelatedtothefirm’sactivities. 1.2Governanceoftheboard Fortheboardtoeffectivelysuperviseandmanagethefirm’sadherencetotheagreedbusinessstrategyandrisk appetite,directorsshouldbeprovidedandhaveaccess to comprehensiveinformationaboutthefirm’srisks. Thisinvolvesensuringtherearecommunicationandreportingproceduresacrossboardsub-committees,andseveralnationalauthoritiessetoutsuchrequirementsintheirguidance(seeAnnexE). However,thereislittlesupervisoryguidanceprovidedonthelevelandtypesofriskinformationfirmsshouldprovideaswellasthefrequencyofriskreporting. Importantly,theriskmanagementreportsprovidedtotheboardshouldcontribute to soundriskmanagementanddecision-making. Theboardanditscommittees,however,shouldnotjustrelyontheinformationmanagementreportsprovided. Theyshouldconsiderifthereisaneedforadditionalrisk-relatedinformationwhichshouldbemadeavailabletothemwhenneeded. Onlyafewjurisdictions,however,requiretheboard tohavesuchaccess. 2.Thefirm-wideriskmanagementfunction Sincethefinancialcrisis,nationalauthoritieshaveintensifiedtheiroversightoffirms’risk managementpracticesandraisedtheirexpectationsforwhatisconsideredstrongrisk management,whichisintegralto thecorebusinessofafinancialinstitution. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |27 • Thefailure tohaveastrong, independentrisk managementfunctioncanlead to ill-informedboardsandseniormanagementteamsaswellasimprudentdecisions. • Therisk managementfunctionshouldberesponsibleforthefirm’sriskmanagementframeworkacross theentireorganisation,ensuringthatthefirm’srisklimitsareconsistentwiththeRASandthatrisk-takingremainswithinthoselimits. • Stress testsandscenarioanalysesareviewedasausefultoolforidentifyingfirms’vulnerabilitiesanddevelopingrisk managementstrategiestoaddresstherisksidentified. • Tofulfiltheseresponsibilities,riskmanagementfunctionsshouldbeled byaninfluentialandhighlyeffectiveCRO. • 2.1Governanceoftheriskmanagementfunction • SupervisorshaveincreasedtheirexpectationsfortheriskmanagementfunctionandareevaluatingtheCRO’sstature,authority,qualifications,andindependencewithinthefirm. • Asthecrisisdemonstrated,theseareprerequisitesfortheCROtobeabletoinfluencethefirm’srisk-takingactivitiesdirectlyandthroughtheriskmanagementfunction,andtoeffectivelyinformtheboardasrisksevolve,are identified,andaretaken. • AnnexFprovidesmoreinformationonthegovernancearoundtheriskmanagementfunction,butsomesupervisorypracticesregardingtheCROfunctioninclude: • Independence:MostjurisdictionsrequiretheCROand/orriskmanagementfunction tobeindependent;thatis,tohaveadistinctrolefromthe otherexecutivefunctions,revenue-generatingfunctionsand businesslineresponsibilities. • Stature:TheCROandriskmanagementfunctionshouldhavesufficientstatureintheorganisationtoinfluencethefirm’srisk-takingactivities. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |28 • Inthisregard,somejurisdictionshavesupervisoryguidancethatrequirestheCROtoreportandhavedirectaccess to theboard. • ToelevatetheCRO’sstature,SingaporeexpectsthedismissaloftheCROtobeapprovedbytheboard. • Authority:Toeffectivelyfulfilitsrole,manyjurisdictions30require theCROtohavetheauthority to influencedecisionsthataffectthefirm’sexposuretorisk,andseveraljurisdictionssetoutexplicitexpectationsfortheCROtobeabletochallengemanagement’srecommendationsanddecisionsandcommunicatedirectlywithseniormanagementandwiththeboard. • Qualifications:“Fitandproper”testsarecommonlyusedtoassessthequalificationsandcompetenciesoftheCROinmanyFSBmemberjurisdictions. • In addition,theappointmentoftheCROisapprovedbyauthoritiesinChina,Germany(iftheCROisamemberofthemanagementboard),andSingapore,whiletheUnitedKingdominterviewsCROcandidates. • ManyjurisdictionsevaluatetheCROthroughtheiron-goingsupervisoryprocesses. • 2.2Riskappetiteframework • Assessingafirm’sRAFisachallengingtaskthatrequiresgreaterclarityandanelevatedlevelofconsistencyamongnationalauthorities. • AtthecoreoftheRAFisthefirm’sRAS,whichhas becomeaneffectivetoolforenhancingthediscussionsbetweensupervisorsandboardsaboutthefirm’sstrategicdirectionintermsofrisk taking. • However,akeychallenge towardassessingtheeffectivenessofafirm’sRASisalackofcommonterminologyforriskappetite,riskprofile,andriskcapacityusedwithinfirms,acrossfirmsandacrossnationalauthorities. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |29 Thisisanarea thatisdevelopinginmanyjurisdictions;forinstance,India,RussiaandSaudiArabiahavelookedatrisk appetiteonlyincontextoftheBCBSICAAP,while inCanada,FranceandtheUnitedStates,separateprocessesarecontinuingto beputinplacetoassessfirms’RAFs,oftendrawingonassessmentcriteriaoutlinedintheworkoftheSSG. Supervisoryreviewsareunderwayin Canadaoffirms’integrationoftheirRAF withthestrategic,financialandcapitalplanningprocessesandcompensationpractices. InHongKong,firms’risk appetiteisreviewedfromanintegratedfirm-wideperspectivetaking intoaccountallrisks(financialand non-financial). Thesupervisordetermineswhetherthefirm’sRASiscomprehensiveandincludes theappropriaterisktargetsthatareconsistentwitheachother. ThesupervisorwillalsodeterminewhethertheRAShasawiderangeofmeasuresandactionableelementsandwhetherrobustproceduresandcontrolsare inplaceforthesettingandmonitoringoftheagreedriskappetite. NationalauthoritiesinSingaporeassessannuallyfirms’linkbetweenriskappetite,strategicobjectives,capitalplanningandoperationalbudgetplanning. Supervisorsalsoreviewthefirm’sprogressinthetranslationofriskappetiteintolimitsandtriggersbyrisk type,aswellastheirmonitoringandreportingprocedures. InSwitzerland,supervisorsregularlyreviewtherisklimitframeworksandthere mustbeanestablishedlinkbetweenthelimitsandthestrategy. 2.3Stress testing The objectiveofstresstestsandscenarioanalysesistoassesstheunanticipatedlossesthatafirmmayincurundercertainstressscenarios InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |30 andtheimpactthatmayhaveonitsbusinessplans,riskmanagementstrategiesorcapitalplans. Theuseofstresstests infirms’riskgovernanceandcapitalplanninghasincreasedin recentyearswiththeresultsservingasaninputintothefirm’sstrategicdecision-making. Asfirmsareincreasinglylinkingstress testresultstorisk appetite,ICAAP,contingencyplanning,andrecoveryandresolutionplans,supervisoryapproachestostresstestingareevolvingaccordingly. InCanada,supervisorsassesswhetherchosenscenariosareappropriatefortheportfoliooftheinstitution, includingsevereshocksandperiodsofsevereandsustained downturns,andwhererelevant,anepisodeofmarketturbulenceorashock tomarketliquidityandwhetherthefrequencyandtimingofstresstestingissufficient to supporttimelymanagementaction. Similarly,supervisorsinHongKongassessthecoverageofstresstestsandthetypesofstressscenariosandparameterschoseninrelationtothefirm’srisktolerance,overallrisk profileandbusinessplan;appropriatenessofassumptions;adequacyofpoliciesandprocedures;theadequacyofthefirm’scontingencyplanningforactiontobetakenshouldaparticularstressscenariohappen;thelevelofoversightexercisedbytheboardandseniormanagementonthestress-testingprogramandresultsgenerated;andtheadequacyofthefirm’s internalreviewandauditofitsstress-testingprogram. Indeed,supervisoryattentionnowincludesboththeoutcomesofstresstestsandtheeffectivenessofthefirms’stresstestingprocesses. Forinstance,Singapore,SwitzerlandandUnitedKingdomhavededicatedteamstoreviewstresstestingpracticesatfirms,andChina,Germany,andHongKongexpectfirms’internalauditfunctionstoassesstheeffectivenessofrisk managementsystemsingeneral,includingstresstests. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |31 • 3.Independentassessmentoffirms’riskgovernanceframework • Strong internalcontrolsystemsareakeyelementofsoundriskgovernance. • Theboardisresponsibleforoverseeingtheimplementationofaneffectiveriskgovernanceframework,andassuch,shoulddirectlyoverseetheindependentassessmentprocess. • Anassessmentthatisindependentfromthebusinessunitandtheriskmanagementcontrolfunctioncanassisttheboardinjudgingwhethertheriskgovernanceframework,internalcontrolsandoversightprocessesareoperatingasintended. • Thismaybeperformedbyinternalauditorbythirdpartiessuchasauditfirmsorconsultants. • Regardlessoftheapproach,itiscriticalthattheassessmentresultinanoverallopiniononthedesignandeffectivenessoftherisk governanceframeworkandbeperformedbyindividualswiththeskillsneededtoproduceareliableassessment. • Currently,auditfunctionsatonlyafewfirmsprovideoverallopinionsregardingtherisk governanceframework. • 3.1Internalaudit • Across theFSBmembership,regulatoryorsupervisoryexpectationsexistforinternalaudit. • AnnexGprovidesacomparisonofkeyregulatoryandsupervisoryexpectationswiththemostnotableelements,including: • Independence:Nearlyalljurisdictions38requirefirmstohaveapermanentinternalauditfunctionthatisindependentfrombusinesslines,supportfunctions(e.g.,treasury,legal),andrisk management. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |32 • Firmsarealsorequiredtoexplicitlylinktheindependenceofinternalaudittoauditorcompensationorcareerplans. • Regardlessofthedirectreportinglines,mostjurisdictionsexpectinternalaudittohaveunfetteredaccesstotheboardwhenreportinginternalauditresults. • Stature:Severaljurisdictionsexpectinternalaudittoreportdirectlytotheboard,acommitteethereof,oranindependentdirector. • Thedirectreportingrelationshipinvolves theresponsiblepartydeterminingtheCAE’scompensation,completingtheCAE’sannualperformanceevaluation,approvingtheCAE’sbudget,and/orotherwiseensuringtheCAEisnotundulyinfluencedbytheCEOorothermembersofthemanagementteam. • WhiletheCAEmayreporttotheCEOonday-to-dayadministrativematters,allsubstantivedecisionsregardingtheCAEandinternalaudit functionaremadeattheboardlevel. • In Singapore,HongKong,andIndonesia,thedismissaloftheCAErequirestheauditcommittee’sapproval. • Qualifications:AllFSBmembershaveestablishedrequirementsorexpectationsfortheCAEandinternalauditstafftohave theskillsnecessarytoeffectivelycarryouttheirduties. • Supervisoryassessmentsgenerallyconsiderthetechnicalknowledge, experience,andcharacterofindividualswithintheinternalauditfunction. • Scope,coverage,andfrequency:Manyjurisdictions41expectinternalaudittoassessand/oropineonrisk managementorrisk governanceprocesses,aswellasinternalcontrols. • Expectationsforthescope,coverage,andfrequencyofsuchassessmentsvarywidely. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |33 • However,almostalljurisdictionsexpectinternalaudit to assesstheorganisationandmandatesoftherisk managementfunction(s)andtheadequacyofsystemsandprocessesforassessing,controlling,respondingto,andreportingthefirm’srisks. • Nojurisdictionindicatedthatitexpectsinternalaudit toperiodicallyprovideafirm-wideassessmentofriskmanagementorriskgovernanceprocesses. • Riskappetiteframework:Manyjurisdictionsexpectinternalaudit toassesscompliancewiththeboard-approvedrisk appetite. • In theUnitedKingdom, internalauditisexpectedtoensurethatproceduresareinplacetoreportbreachesinthefirm’sriskappetitetotheboard. • Benchmarking:Mostjurisdictionsindicatethatinternalauditshouldbeawareofindustrytrends/bestpracticesandthatauditorsshouldconsidersuchknowledgewhenconductingtheirwork. • However,nojurisdictionhadspecificexpectationsfor internalaudit toopineonwhetherafirm’srisk governanceprocessesarekeepingpacewithtrendsand/oralignwithbestpractices. • Remediationprocess:Thereisawiderangeofexpectationsfor internalaudittofollow-uponremedialactionstoaddressmaterialdeficienciesandseveraljurisdictionsexpectinternalaudit to reporttheresultsofitsfollow-up activitiestotheboard. • Nearlyalljurisdictionsindicatedthattheyrequiresomeformoffollow-upandreporting. • Chiefauditexecutive:AlljurisdictionsindicatethatsupervisorsconsidertheCAE’sperformancewhenassessingthequalityofinternalaudit. • Suchassessmentsmaybeperformedoff-site,withinon-siteinspections,and/orthroughregularmeetingswiththeCAEandinternalauditstaff. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |34 InSaudiArabia,theappointmentoftheCAErequiresa“noobjection”fromthecentralbank,andin Indonesia,banksarerequiredtoreporttobanksupervisorstheappointmentanddismissaloftheirCAE. 3.2Thirdparties Employingthirdpartiescouldhelptoenhancethequalityoffirms’independentassessmentsbyprovidinganunbiasedopinionofafirm’sriskgovernanceframeworkasmanyinternalauditfunctionsarestaffedwithindividualswhoseexperiencemaybelimited tothepracticesemployedbyoneortwo firms. In addition,thirdpartiesoftenhaveabroaderunderstandingofleadingindustrypractices,especiallyinhighlytechnicalareas. Mostjurisdictionsallow theuseofthirdpartiestoassessafirm’sriskgovernanceframework,andin ChinaandtheNetherlands,theexternalauditoralsoassessestheeffectivenessoftheinternalauditfunction. Manyjurisdictionsappropriatelystipulatethroughregulationorguidancethat: Theuseofathirdpartydoesnotrelinquishtheboardormanagementfromultimateresponsibilityforensuringthereliabilityoftheindependentassessments,and Largeandcomplexfirmsshouldnotbecomeoverlyreliantonthird partiestoprovideexpertisethatshouldbedevelopedwithinthefirm’sinternalauditfunction. Francespecificallyrequiresthatoutsourcingarrangementsbeengagedandoverseenbyinternalaudittoensureindependenceandthatinternalauditmaintains accountabilityforthescope,coverage,andfrequencyofwork. Severaljurisdictions,however,restricttheuseofthirdparties. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |35 Forinstance,inItaly,internalauditworkcanbeoutsourcedonlybysmallcreditinstitutionswithlimitedoperationalcomplexity. Meanwhile,inSouthAfricathecentralbankmustapproveanyoutsourcingactivity,andinKorea,theuseofthirdpartiestoassessafirm’sriskgovernanceframeworkisnotregulated. 4.Supervisoryapproachestowardassessingriskgovernanceframeworks Supervisorsplayacrucialrole inassessingtheadequacyofafirm’sriskgovernanceframeworkandthepracticesemployedbyafirmtoindependentlyassessitsframework. Supervisoryexpectationsforriskgovernancepracticesoutlinedabovearegenerallysetoutwithin thelegalframeworkthroughacombinationoflegislation,regulationandsupervisoryguidance;however,theapproachvariesconsiderablyacrossjurisdictions. AustraliaandCanadacomplementtheirstandardswithwrittenguidanceprovided totheindustrytoassistwiththeimplementationofprudentialrequirementsandadoptionofgoodpractices. Supervisoryapproachestowardassessingimplementationofregulatoryorsupervisoryguidanceencompassavarietyofsteps(e.g.,on-siteinspections,off-sitereviews,horizontalreviews). Supervisoryassessmentsgenerallyoccuratleastonceayearacross theFSBmembership,thoughinArgentinaassessmentstakeplaceevery18monthsandtheUnitedKingdomismovingfromabi-annualassessment towardasystemofcontinuoussupervision. Severaljurisdictionstakearisk-basedapproach to on-siteexaminations,focusingonriskierinstitutions. In theUnitedStates,nationalauthoritieshaveon-siteteamswithexpertisetoassessthegovernancepracticesatthelargestandmostcomplexbanksonarealtimebasis. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |36 In China,jointregulatorymeetingsareheldonaregularbasisbetweenthefirm’sheadoffice,itsbranches,andtheregulatoryauthoritywherethebranchesarelocated. Meetingswithdirectorsandseniormanagementprovideanotheravenuefornationalauthoritiestoassessfirms’risk governancepractices. AnnexHprovidesmoreinformationontheapproachestaken toassessingfirms’riskmanagementframeworks. Supervisorsreceiveawiderangeofriskreportsor informationfromfirmsontheirriskmanagementpractices, includingfromexternalauditorsorotherthirdpartiesaswellassupportingdocumentationrequestedduringon-siteinspections. Standardisedfinancialandrisk reportingareacommonpractice;however,thetypesofreportsorinformationprovidedvaries. Forinstance,inArgentina,newreportingrequirementswillrequestquantitativemeasuresforrisk governanceandformalexposurelimitsforeachofthesignificantrisksandstresstestinformation;inHongKongandelsewhere,regularprudentialreportingdataandadhocrequestsforpeergroupanalysisareutilised,e.g.,stresstestcapitalanalysisand horizontalcreditreviewsofcommon(problem)loan accounts;andinCanadaandSingapore,supervisory teamsworkwithriskspecialists toidentifytrendsthatcantriggeradditionalinvestigationsorreviews. Nationalauthoritieshaveaccesstoabroadsetofsupervisorytoolstoincentivisefirms to remediatedeficiencieswithintheirrisk governanceframework,dependingontheseverityofthedeficiency. Thesetoolsincludemoralsuasion,capitalsurcharges,restrictionsoncertainbusinessactivities,imposingfinesandpenalties,andtheultimatepenaltyofwithdrawingbanklicences. Whilealargenumberofsupervisoryauthoritiescanuseanumberofthesetools,afewhavelimitedsupervisorypowers to scale thesanctionbased InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |37 • ontheseverityoftheinfraction,raisingconcernsovertheirability toeffectivelyinterveneearlywherenecessarywhenrisksstart tosurface. • Moreover,eventhoughsomenationalauthoritieshavetheauthoritytoimposefines,thisisdifficulttoimplementinpractice,forinstance,duetocumbersomeprocessesorsupervisorslackingthewilltoact. • III.Firms’riskgovernancepractices • Thefinancialcrisisspurredfundamentalchangesinrisk governancepracticesatfinancialinstitutions,andinmanycases,surveyedfirmsareaheadofregulatoryandsupervisoryguidance. • Ingeneral,surveyedfirmsthatweremostaffectedbythecrisishavemadethegreatestadvancements,perhapsnecessitatedbyaneedtore-gainmarketconfidence. • Firmsthatwerelesstroubledfromthecrisis,however,haveincreasedtheintensityofthemeasuresthattheyhadinplace pre-crisis. • Someofthemostobviouschangesinclude: • Consolidatingandraisingtheprofileoftheriskmanagementfunction acrossbankinggroupsthroughtheestablishmentofagroupCRO,increasingthestatureandauthorityoftheCROandincreasingtheCRO’sinvolvementinrelevantinternalcommittees. • Changingthereportinglinesoftheriskmanagementfunctionsothat theCROnow reportsdirectly totheCEOwhilealsohavingadirectlinktotherisk committee. • Intensifyingtheoversightofrisk issuesattheboardthroughcreationofastand-aloneriskcommittee,supportedbygreaterlinks withtheriskmanagementfunctionand otherrisk-relatedboardcommittees,particularlyauditandcompensationcommittees. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |38 • Cross-membershipoftheauditcommitteeandrisk committeeisnowquitecommon,withsomefirmsinvolving(oratleastinviting)thechairoftheboard,eventhefullboard,ontotherisk committee. • Thetimecommitmentofindependentdirectorshasincreasedconsiderablyoverthepastseveralyears. • Upgradingtheskillsrequirementsofindependentdirectorsontheriskcommitteeandexpectingthesemembers to commitmoretime totheseendeavours. • Thecompositionofboardshaschangedconsiderablywithmany • non-executivedirectorsnowhavingfinancialindustryexperience;thedominanceofmembersfromindustrialcompaniesormajorshareholdersismuchlessthanadecadeago. • Changingtheattitudetowardtheownershipofriskacrossthefirmwiththebusinesslinenowbeingmuchmoreaccountablefortheriskscreated bytheir activitiesthanpreviously. • In additiontochangingthecompositionandimprovingthestrengthoftheboard,therehavebeenmajordevelopmentsinhowfirmsanalyserisksandtheassociatedtoolsutilisedsuchasRAFs,stress testsandreversestress testing. • Oneofthekeylessonsfromthecrisiswasthatreputationalriskwasseverelyunderestimated;hence,thereismorefocusonbusinessconductandthesuitabilityofproducts,e.g.,thetypeofproductssoldandwhotheyaresoldto. • Asthecrisisshowed,consumerproductssuchasresidentialmortgageloanscouldbecomeasourceoffinancialinstability. • Thenextfoursub-sectionssummarisethefindingsfromthesurveyedfirmsregardingthethreekeyrisk governancefunctionsandprovideasummaryofthesupervisoryevaluationsoffirms’progress. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |39 1.Theboardandits committees Theboardisresponsibleforensuringthatthefirmhasanappropriateriskgovernanceframeworkthatiscommensuratewiththefirm’sstrategy,complexityandsize. Theboard’sroleandresponsibilitiesforrisk governancearegenerallydefinedintheboard’scharterandincludeapprovalofthefirm’sstrategyandoverseeingitsimplementation,settingouttheguidelinesandpoliciesforriskmanagement,andensuringthefirm’sinternalcontrolsarerobust. Theboardisalsoresponsibleforformulatingthemandateandresponsibilitiesofitscommitteessuchastherisk andauditcommittees. Forinstance,auditcommitteesshouldensurebusinessunitshaveeffectiveremediationplans to addressanycontrolweaknessesnotedbyinternalaudit. SomefirmshavedevelopedaCorporateGovernanceFrameworkor Codewhereallrulesregardingtheroles,responsibilitiesandoversightfunctionsoftheboardareassembled. Establishinganenterpriseorfirm-widerisk managementframeworkcanhelptoprovideanoverviewofriskpolicyarchitectureandprocess. Havingastand-alonerisk committeeisacommonpracticeeventhoughitisnotrequiredbyallnationalauthorities. Firmsgenerallyensurethattherisk committee,whichisresponsibleforoverseeingseniormanagement’simplementationoftheriskstrategy,coversalltherisksfacedatthefirm-widelevel,includingfinancialrisksaswellasoperational,compliance,legalandregulatoryrisks. RegularmeetingsareheldwithseniormanagementandtheCROtodiscussperformanceofthebusinessunitandcompliancewiththeRASandrisk limits. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |40 Materialrisksarepresentedanddiscussedonbothanaggregatebasisandbytypeofrisk. Afewfirms,however,notedthechallengeofaggregatingrisksdue to thecomplexityoftheorganisation,underscoringtheimportanceofriskcommitteesaddressinginformationchallengesarisingfromthecomplexityoflargefirms. Aneffectivegovernancestructurehasmeasures topreventconcentration ofpowerandresponsibility,suchasrequiringanumberofindependentdirectors,representationofcertainskillsandqualificationsontheboard,andtheboardregularlyevaluatingitseffectiveness. Itiscommonforboardstohaveindependentdirectors;somefirmsestablishminimumquantitativerequirements,rangingfromaminimumofone-third tothree-quartersoftheboard. Most firmsprovideadefinitionofindependence intheboard’scharter,whichisembeddedinthefirm’sgovernanceframework. Therisk committeeoftencomprisesonlyindependentdirectors. Thereisawiderangeofpracticeregardingthequalificationsformembersoftheboardandrisk committee;onefirmhighlightedthattheskillsrequiredbytheboardareevolving, in partreflectingtheriskstakenbythefirm. Somefirmsperformamatrixanalysisoftheexperienceandexpertiseofeachdirectortoidentifyskillsneededfromincomingdirectors. Thereisalsoawiderangeofpracticeinvolvinglimitationslinkedtoboardstructure,including: Thepreclusionofthechairoftheboardfrombeingchairofeithertheriskorauditcommittee; TheseparationoftherolesoftheCEOandchairoftheboard;and InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |41 (iii)Limitedtenureonacommittee. Periodicreviewsoftheperformanceoftheboardandriskcommitteeareacommonpractice. Reviewsareconductedby theboardnominationorgovernancecommitteesorbytheentireboard. In somecases,externalpartiesmaybeemployed.Suchreviewsmayincludeanassessmentoftrainingand skillsneededontheboard. In somefirms,theboardconsidersthefunctioningofitsoverallcommitteestructure,includingthenumberandtypesofcommitteesandthehighestandbestuseofboardmembers’expertise. Theyalsoevaluatethereportingbythecommitteestothefullboard. Theboardandriskcommitteeareabletoreceiveinformation, bothformallyandinformally,directlyfromtheCROortherisk managementfunction. ItisbecomingacommonpracticefortheCROtoreportinformationdirectly totheboard;therisk reportsareusuallystandardised in termsofformality,frequencyandcontent. Boththeoverallrisklevelofthefirmandinformationforeachrisk typeare includedinthereportingtemplate(e.g.,aheatmapofidentifiedriskcategoriesacrossregions,globalbusiness,andareportwiththetopandemergingrisksfacedbythefirm). Somefirmsexplicitlydefineanddocumenttheinformationthattheboardandrisk committeeshallreceive,settheagendaatthebeginningoftheyear,andcirculatetomembersinadvanceofmeetingstherelevantmaterialto supporttheagendaitem. Somefirmsrequireinternalaudit,orathirdparty,toverifytheaccuracy,comprehensivenessandcompletenessofinformationprovided to theboardandrisk committee. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |42 Otherfirmssatisfythemselvesthroughdiscussionswithmanagementorconductself-assessmentsoftheeffectivenessoftheinformationprovidedtotheboard. 2.Theriskmanagementfunction Sincethefinancialcrisis,manyfirmshaveimprovedriskmanagement. Someofthemostobviouschangesrelateto thegovernanceprocessesaroundtheriskmanagementfunction;therealsohavebeenmajorchangesinhowrisksareanalysedandcommunicatedandtheassociatedtoolsthatareutilised. 2.1Governanceoftheriskmanagementfunction Sincethefinancialcrisis,manyfirmshavestrengthenedhowtheirriskmanagementfunctionsarestructured,resourced,compensated,whothefunctionis accountable to aswellasitsoverallmandate. In manyways,thesechangesarebringingthegovernancearrangementsfortheriskmanagementfunctionuptothestandardthathastypicallyappliedtotheinternalauditfunctionforseveralyears. Firmsarethereforeencouraged to atleastconsiderthevalidityofany remainingdifferencesingovernanceprocessesthatsurroundthetwofunctions. Oneofthemostcommonimprovementsmadebyfirmsoverthepastfiveyearshasbeentoconsolidateandraisetheprofileoftheriskmanagementfunctionthroughtheestablishmentofagroup-wideCRO. TheCROandtherisk managementfunctiongenerallyhavebeengivenmorestature,authorityandindependencecompared to thepre-crisisperiod. AlmostallfirmsreportedthattheynowhaveaCROwithfirm-wideresponsibilityforriskmanagementwhooperatesindependently. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |43 AssessmentoftheCRO’sstature,authorityandindependenceincludestheprocessforappointment,dismissalandperformanceevaluationoftheCROaswellasthestaffingrequirementsoftheriskmanagementfunctionmoregenerally. Onlyafewfirmsnotedthatthechairoftherisk committeeisinvolvedintheperformanceassessmentoftheCRO. Further,onlyafewfirmslinktheadequacyandqualificationsoftheriskmanagementstafftoanannualprocessthattakes intoconsiderationthestrategyofthefirmgoingforward. MostfirmsnotedthattheCROhasadirectreportinglinetotheCEO(versus anotherbusinessunit)whichrepresentsamajorimprovementsincethecrisis. However,therearestillexamplescitedatasmallnumberoffirmswheretheCROdoesnothaveadirectreportingline to theCEO. AfewfirmsrequiretheCROtohaveadirectreportinglinetotheboard,whichhelpstoboostthestatureoftheCRO. Alarge numberoffirmsalsonotedthattheirCROisable to“access”theboard,generallythroughtheriskcommittee,butitisunclearhow thisisdoneinpractice. AlmostallfirmsoperatewithaCROwhoisseparatefromrevenue-generatingresponsibilitiesorotherexecutivefunctions(thatis, “dual-hatting”oftheCRO’sresponsibilitiesisavoided).SuchastructureisessentialfortheCRO’sindependence. Thisseparationofresponsibilitieshasbeenreinforcedbymanyfirms re-structuringtheirriskmanagementfunctionsunderagroup-wideCRO,withregionalorbusinesslineCROshavingadirectreportingline to thegroupCRO,ratherthantotheregionalorbusinesslineheadsashadoccurredinthepast. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |44 • Topreservetheindependenceintendedfromsuchstructures, • ‘dual-hatting’ofresponsibilitiesshouldalsobeavoidedforthoseseniorpositionsintheriskmanagementfunctionthatreporttothegroupCRO,particularlyatgloballyactive,complexfirms. • Atsomefirms,theCROreportstotheCFOor,inafewexceptionalcases,onepersonassumestheresponsibilitiesofboththeCROandCFO. • In addition,thereareinstancesatsomefirmswheretheCROisassignedotherfunctional,albeitnon-revenuegenerating,responsibilities. • Wherethisrelates totheoversightoffunctionssuchascomplianceandanti-moneylaundering,theconcernismoreabouttherisk of • over-burdeningtheCRO,particularlyinmorecomplex,global • institutions,thanthepotentialforconflictofinterestperse. • Indeed,muchprogresshasbeenmadetowardelevatingthestatureandindependenceoftheCRO. • WhiletheroleoftheCROhasbroadenedandincludesinvolvementin anumberofkeyprocessesandinternalcommitteesthatrequireinputsfromtherisk managementfunction,otherimportantprocesseswarrantgreaterparticipationoftheCRO,suchas: • Mergersandacquisitions.Whiletheanalysisofaproposedmergeroracquisitionwouldbesubmittedtotheboardoracommitteeforapproval, theCROgenerallytakes partintheprocessasamemberofthecommittee. • OnlyafewfirmsrequiretheCROtoprepareaformalriskopiniononplannedmergersand acquisitions. • Strategicplanningprocess.Traditionally,theCROisresponsiblefortheoversightoftheexistingriskprofileofthefirmandofthoserisksbeingtakenonaday-to-daybasisasaresultofpreviousbusinessdecisions. • However,asindicatedabove,theCROshouldalsobecomeincreasinglyinvolved, in amoreproactivemanner,intheactivitiesandplansthatdeal InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |45 • withprospectivebusinessrisk,includingthoseriskswhichmayarisefromtheexecutionofthefirm’sstrategicbusinessplan. • TheCRO shouldbeinvolvedinthisprocess,fromariskperspective,byinteractingwithseniormanagementandtheboard,understandingstrategicbusinessplans,andformallyopiningontheprospectiveriskprofileandwhetherornotthefirmhasthenecessaryresourcesandsystems to accommodatetheresultingexposures. • Ifsuchresourcesarenotavailable,thenspaceinthestrategicplanshould becreated to ensureproperriskcontrols. • Treasuryfunction.SomefirmshaveclearlydefinedtherolesandresponsibilitiesoftheCROregardingoversightofafirm’streasuryfunction. • However,thereisarangeofpracticesurroundingtheorganisationalrelationshipbetweenthesetwo functions: • Theindependentliquidityrisk controlfunctionhasresponsibilityforthemanagementandcontrolofliquidityrisk andthatfunctionreportsdirectly totheCRO; • TheCROparticipatesasavotingmemberoftherelevantmanagementcommittee(typicallytheassetandliabilitymanagementcommittee),withnospecific rolefortheCROdefined;or • TheCFOaloneisresponsibleforthetreasuryfunctionwithoutanyoversightfromtheCROintheriskmanagementprocess. • 2.2Riskmanagementtools • Two keyadditionstoriskmanagementtoolshavebeen(i)thedevelopmentofRAFsand(ii)morerobustandseverestresstestingpractices. • Relatedtothis,andgiventheunderestimationofreputationalrisk pre-crisis,therenowismuchgreaterfocuswithinmanyfirmsonbusiness InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |46 • conductandthesuitabilityofproducts,e.g.,thetypeofproductssoldandtowhomtheyaresold. • TheRAFisanincreasinglyimportanttoolincentralisingthefocusonthefirm’sriskprofileandprovidingamoreintegratedpictureofthefirm’s risks. • Firmsindicatedagooddegreeofunderstandingthekeyelements,objectivesandusesofRAFswhicharegenerallyin linewithrecentstudiessuchasthe2010SSGreportondevelopmentsin risk appetiteframeworksandITinfrastructure. • Keyfeaturesofariskappetiteframework(RAF) • RAFshelpdrivestrategicdecisionsandright-sizeafirm’srisk profile. • RAFsestablishanexplicit,forward-lookingviewofafirm’sdesiredriskprofileinavarietyofscenariosandsetoutaprocessforachievingthatriskprofile. • RAFsincludeariskappetitestatementthatestablishesboundariesforthedesiredbusinessfocusandarticulatetheboard’sdesiredapproachtoavarietyofbusinesses,risk areas,andinsome cases,producttypes. • ThemoredevelopedRAFsareflexibleandresponsivetoenvironmentalchanges;however,risk appetiteisdefinitiveandconsistentenough tocontainstrategicdrift. • RAFssetexpectationsforbusinesslinestrategyreviewsandfacilitateregulardiscussionsabouthow tomanageunexpectedeconomicormarketeventsinparticulargeographiesorproducts. • Discussionswithfirms,however,revealthatthereissignificantvariationintheperceptionofhowmuchfirmshaveprogressedinthedevelopment,comprehensivenessandimplementationoftheirRAFs. • Oneofthekeychallengesisdifferentinterpretationsofessentialelements,includingrisk appetite,risklimits,andrisk capacity. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |47 • Somefirmswereable to reportsignificantprogressandhavehadanRAF forseveralyears(insomecasessincebeforethecrisis). • Thesefirms’RAFswerelinkedtothefirm’sstrategyandintegratedwithmost otherrelevantinternalprocessessuchasbudgeting,compensation plans,mergersandacquisitionevaluations,newproductapproval,andstress testing. • Thesefirmswereable to reportthattheunderstandingoftheRAFwas widespreadbothacrossfunctionallinesandwithinmultiplelayersoftheirfirm. • Theywerealsoabletoidentifyclearexamplesofhowtheyhadusedtheir RAFinstrategicdecision-makingprocesses,suchasdecisionstoactivelyreducethecomplexityoftheiroperations. • Thatsaid,evenatthesefirms,itwasrecognisedthatoperationalisinganeffectiveRAFisacontinualjourneythatneedstoevolvewithchangesin internalprocessesandtheexternalenvironment. • AnumberoffirmsreportedthattheirimplementationofanRAF wasmorerecentandwhileithadbeenlinkedto thefirm’sstrategyandintegratedwithsomeofthekeyinternalprocesses,furtherworkisenvisaged,suchas:linkingtheRAF withalltherelevantinternalprocesses;ensuringthatqualitativeaswellasquantitativemetricsareappropriatelyincluded;andsomewhatrelatedly,broadeningtheRAFtocoverthosehardertoquantifyrisks,suchasoperational,complianceandreputationrisks. • Forotherfirms,theirRAFsareatanearlystageofdevelopment. • Whiletheymayhaveahigh-levelframeworkinplace,numerousgapsexist. • Forexample,thecoveragemaynotextendtoallrelevantsubsidiariesintheframeworkbecausetherisk appetiteisnotclearlyarticulatedatthebusinesslevelnorintegratedwithalltherelevantinternalprocesses. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |48 Further,someRAFsarelessdevelopedintermsofincludingallthematerialrisksthefirmfaces,particularlyreputationalandoperationalrisks. Allfirmssurveyedconsideredrisk limitsto bethevehicleforoperationalisingtheRAF atthebusinesslinelevel. Thecommunicationandescalationprocessforanybreachesseemedtobeverysimilaracross thefirmssurveyed:theriskmanagementfunctionwasresponsibleformonitoringrisk limits,metrics,andbreaches,andescalatinganyconcerns;businessunitshave toexplainbreachestotheriskmanagementcommitteeorboarddependingonthenatureandsizeoftheexposure;theauthorisationofexceptionswasdefined top-down;andactionplanswererequired. However,thereweredifferencesbetweenfirmsintheirapproaches todeparturesfromtheRAF:somefirmsgrantflexibilityforabusinesslinetodepartfromtheRAFiftheglobalriskappetitewasnotbreached,whereasothersgivenoflexibilityfor individualbusinesslinesto deviatefromtheirbusinesslinerisk limits. Embeddingthefirm’sagreedRASintothefirm’srisk cultureremainsachallengebutseveralapproacheshavebeentakenbyfirms. Anumberoffirmshavedevelopedtrainingprogramsandmanuals(withonefirmrequiringrelevantemployeestocertifyeveryyearthattheyhaveattendedthetrainingprogramandreadthemanual),butonlyafewfirmsreportedthattheyhavelinkedcoreriskobjectivestostaffperformancemanagementprocesses. Discussionswithfirmsrevealedthatakeytocreatingincentivesforabetterriskcultureinfirmsisto linkriskobjectiveswitheithercompensationorcareeradvancementprospects. Stress testinghasbecomeacommontoolforfirms. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |49 Thegovernancearoundgroup-widestresstestingtypicallyinvolvesfirmsdevelopingtheir ownhistoricalandhypotheticalscenarios,though nationalauthoritiescan alsosetscenarios. TheCROandriskmanagementfunctiongenerallyhaveacentralrole,actingasthe owneroftheprocessorparticipatinginthecommitteeleadingtheeffort. The testingisconductedatleastannually,andinmany casesonaquarterlybasis. Stress testsresultsareusuallypresentedtotherisk committeeandsometimestothenationalsupervisor. TheseprocessesappeartobefurthestdevelopedinAEs,andsomealsoperformreversestresstestingandcounterpartystresstesting. In contrast,somefirmsinEMDEshavenotperformedstresstestingonanintegratedbasisorarestillin theprocessofimplementingtheirstresstestingprocesses. Mostfirmsusethestresstestingresultsfortheirbudgeting,RAF andICAAP processesand to setcontingencyplansagainststressedconditions. 3.Independentassessmentoffirms’riskgovernanceframework 3.1Internalaudit Firmsprimarilyrelyontheirinternalauditfunctions to independentlyassesstheirrisk governanceframeworks. Inalmostallcases,internalauditassessestheframeworkthroughaseriesofindividualassuranceaudits,combinedwithsomeproject-specificandotherongoingauditwork. InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com

P age |50 • Afewinternalauditfunctionsdemonstratethebetterpracticeof providinganoverallopinionoftherisk governanceframeworkonan annualbasis. • In linewithexpectationsestablishedbynationalauthorities,allofthefirms’internalauditfunctionsareorganisationallyseparatefrombusinesslinesandhaveunfettered accesstotheboard. • Almosteveryfirmreportedthattheyhavemadechangestostrengthentheir internalauditfunctionssince2008. • Majorchangesinclude:appointingaCAE;establishingmoreattractivecompensationplansandcareerpathsfor internalauditors; increasingboththenumberandskillsofinternalauditstaff;expandinginternalaudit’srole/responsibilities,includingparticipatingasanobserveratriskmanagementcommitteesanddecision-makingprocesses;andenhancingbusinessmonitoring. • Internalaudit’sroleandresponsibilitiesareprimarilyestablishedviaanauditcharter,withauditmanualsdetailingproceduresforplanning,executing,andreportingaudit’swork. • Atallsurveyedfirms,internalauditisresponsibleforassessingriskmanagementorriskgovernanceprocessesaswellasinternalcontrols. • Whilenationalauthorities’expectationsvary,mostinternalauditfunctionsalsoassess: • Theappropriatenessofassumptionsusedinscenarioanalysisandstresstesting, • Thedegreetowhichthefirm’srisk governanceiskeepingpacewithindustrytrendsandalignswithbestpractices, • Thequalityandadequacyofresourceswithintherisk managementfunction, InternationalAssociationofRiskandComplianceProfessionals(IARCP)www.risk-compliance-association.com