Download

1 / 9

90 likes | 99 Views

The Uniform Certified Public Accountant examination is a credentialing exam for professionals seeking to become CPAs. It is graded by AICPA (American Institute of Certified Public Accountants) and administered with NASBA (National Association of State Boards of Accountancy).

E N D

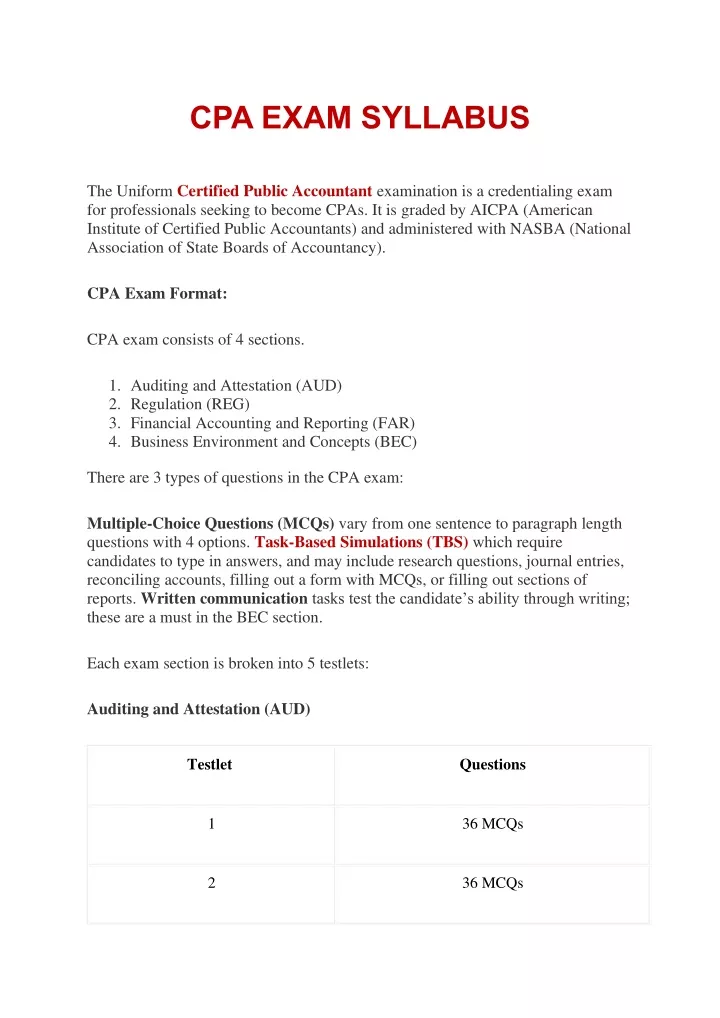

CPA EXAM SYLLABUS The Uniform Certified Public Accountant examination is a credentialing exam for professionals seeking to become CPAs. It is graded by AICPA (American Institute of Certified Public Accountants) and administered with NASBA (National Association of State Boards of Accountancy). CPA Exam Format: CPA exam consists of 4 sections. 1.Auditing and Attestation (AUD) 2.Regulation (REG) 3.Financial Accounting and Reporting (FAR) 4.Business Environment and Concepts (BEC) There are 3 types of questions in the CPA exam: Multiple-Choice Questions (MCQs) vary from one sentence to paragraph length questions with 4 options. Task-Based Simulations (TBS) which require candidates to type in answers, and may include research questions, journal entries, reconciling accounts, filling out a form with MCQs, or filling out sections of reports. Written communicationtasks test the candidate’s ability through writing; these are a must in the BEC section. Each exam section is broken into 5 testlets: Auditing and Attestation (AUD) Testlet Questions 1 36 MCQs 2 36 MCQs

3 2 TBS 4 3 TBS 5 3 TBS Regulation (REG) Testlet Questions 1 38 MCQs 2 38 MCQs 3 2 TBS 4 3 TBS 5 3 TBS Financial Accounting and Reporting (FAR) Testlet Questions 1 33 MCQs 2 33 MCQs

3 2 TBS 4 3 TBS 5 3 TBS Business Environment and Concepts (BEC) Testlet Questions 1 31 MCQs 2 31 MCQs 3 2 TBS 4 2 TBS 5 3 Written Communication Questions CPA Exam by Sections and Question Type: Sections Time MCQs TBS Written communication AUD 4 Hours 72 8 – REG 4 Hours 76 8 –

FAR 4 Hours 66 8 – BEC 4 Hours 62 4 3 Skills Tested by Section: SectionRemembering & Understanding Analysis ApplicationEvaluation AUD 30 to 40% 15 to 25% 30 to 40% 5 to 15% REG 25 to 35% 25 to 35% 35 to 45% – FAR 10 to 20% 25 to 35% 50 to 60% – BEC 15 to 25% 20 to 30% 50 to 60% – CPA Exam Content Areas by Sections: Auditing and Attestation (AUD): •Developing a Planned Response & Assessing Risk (20 to 30%) •Debtor-creditor relationships •Entity’s internal control •Planning an engagement •Assessing and identifying the risk of material misstatement •Materiality •Specific areas of engagement risk •Professional Responsibilities, Ethics & General Principles (15 to 25%) •Nature and scope •Engagement documentation •Ethics and professional conduct •Communication with management

•Communication with component auditors •A firm’s system of quality control •Obtaining Evidence & Performing Further Procedures (30 to 40%) •Sampling techniques •Acquisition and disposition of assets •Internal control deficiencies and misstatements •Performing specific procedures to get evidence •Subsequent events •Written representation •Reporting and Forming Conclusions (15 to 25%) •Reports on attestation engagements •Reporting on compliance •Reports on auditing engagements •Review service engagements •Other reporting considerations Regulation (REG): •Federal Tax Procedures, Professional Responsibilities and Ethics (10 to 20%) •Federal tax procedures •Responsibilities in tax practice •Legal duties •Licensing and disciplinary systems •Business Law (10 to 20%) •Contracts •Business structure •Agency •Government regulation of business •Debtor-creditor relationships •Federal Taxation of Property Transactions (12 to 22%) •Estate and gift taxation •Determination of taxable estate •Acquisition and disposition of assets •Gift tax deductions •Gift tax annual exclusion

•Cost recovery •Federal Taxation of Individuals (15 to 25%) •Passive activity losses •Computation of tax and credits •Gross income •Filing status •Reporting items from pass-through entities •Alternative Minimum Tax •Computation of tax and credits •Federal Taxation of Entities (28 to 38%) •S corporations •C corporations •Liquidation of business entities & tax treatment of formation •Trusts and estates •Limited liability companies •Partnerships •Tax-exempt organizations Financial Accounting and Reporting (FAR) •Standard-Setting, Conceptual Framework, and Financial Reporting (25 to 35%) •Public company reporting topics •Standard setting for non business entities •Conceptual framework •Special purpose framework •Standard setting and conceptual framework for nonbusiness entities •General purpose financial statements •Select Financial Statement Accounts (30 to 40%) •Property, plant, and equipment •Cash and cash equivalents •Intangible assets •Investments •Long-term debt •Income taxes •Compensation benefits •Inventory

•Select Transactions (20 to 30%) •Business combinations •Derivatives and hedge accounting •Leases •Research and development costs •Subsequent events •Differences between IFRS and U.S. GAAP •Accounting changes and error corrections •Contingencies and commitments •Foreign currency transaction and translation •Nonreciprocal transfers •Software costs •Fair value measurements •State and Local Governments (5 to 15%) •Comprehensive Annual Financial Report (CAFR) •Specific types of transactions and events: calculation, measurement, presentation in governmental entity, and valuation. •State and local government concepts •Government-wide financial statements Business Environment and Concepts (BEC) •Corporate Governance (17 to 27%) •ERM (Enterprise Risk Management) frameworks •Internal control frameworks •Regulatory frameworks and provisions •Economic Concepts and Analysis (17 to 27%) •Market influences on business •Economic business cycles •Financial risk management •Financial Management (11 to 21%) •Working capital •Capital structure •Financial valuation methods •Information Technology (15 to 25%)

•Information security/availability •IT governance •Role of information technology business •Processing integrity •Systems development of maintenance •Operations Management (15 to 25%) •Cost accounting •Planning techniques •Performance management •Process management Conclusion: CPAs have a huge demand in different fields like public accounting, business and industry, non-profit, government, and education. Check out the CPA exam syllabus given above to be aware of the subjects. Hope the detailed information provided in this article about the CPA exam syllabus has been helpful to you. Feel free to comment if you have any other doubts. SIMANDHAR EDUCATION Simandhar is the official partner of Becker and AICPA – Largest Training provider for US CPA, US CMA , IFRS and EA, HRCI courses in India. Learn how to clear your CPA exams with extremely satisfying results by getting proper guidance and knowledge through our online courses and video tutorials taught by industry Experts. We’re here to provide you with all the help that you need in order to ace your CPA, CMA exams. We are just a call away for any assistance. Simandhar Education is the leading training provider for the CPA Exam in India. Contact us@ 91 9390584166. Hurry up !! CPA exam now in India and Simandhar Education will help you to achieve it.