Download

1 / 12

120 likes | 213 Views

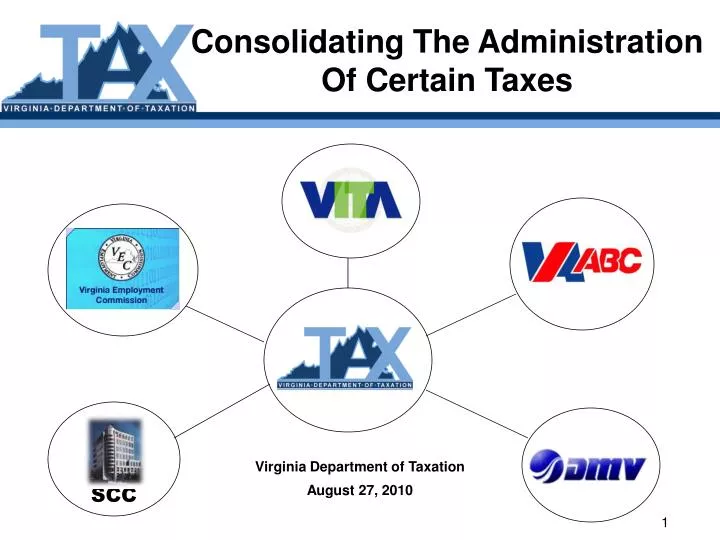

Consolidating The Administration Of Certain Taxes. SCC. Virginia Department of Taxation August 27, 2010. Guiding Principles. Customer service : One check per transaction. Regulatory coordination : No impact on tax revenue that is used by the regulatory agency.

E N D

Consolidating The Administration Of Certain Taxes SCC Virginia Department of Taxation August 27, 2010

Guiding Principles • Customer service: One check per transaction. • Regulatory coordination: No impact on tax revenue that is used by the regulatory agency. • Program coordination: No impact on tax revenue that is dedicated to support a specific program • Resources: Will it be necessary to transfer personnel for subject matter expertise or processing functions? • Cost/Benefit of Transfer: It may not make sense to incur high start up costs for a tax that has a very low volume of transactions and simple accounting requirements.

Process • TAX worked with DOA to develop list of potential taxes to study. • TAX developed scope (14 taxes administered by 5 agencies), guiding principles, and assembled multidisciplinary team. • TAX’s multidisciplinary team visited each of the five agencies to discuss issues, processes and costs. • Draft whitepaper provided to each agency for review and comment. • Agency comments incorporated into final whitepapers.

ABC Department Taxes • TAX examined the feasibility of collecting: 1) the liter tax on wine; 2) state tax on distilled spirits and wine; 3) the beer and beverage excise tax; and 4) the carrier's alternative mixed beverage tax. • Transfer of the tax collection would affect approximately 429 wine wholesalers,147 beer wholesalers, and 61 mixed beverage carriers. The distilled spirits tax is collected at the state-operated retail stores from purchasers of alcoholic beverages. • The privatization of ABC would change the structure of the distilled spirits tax. • While the issue of privatization is not directly related to issue of transferring the administration of the taxes on alcohol from ABC to TAX, it should still be considered in this process as privatization of retail stores would change the structure of ABC. • Recommendations: The Government Simplification & Operations Committee should consider shifting the tax collection from ABC to TAX as part of their recommendations on the privatization of ABC. If the privatization of liquor stores is authorized, the privatization of the stores and the transfer of the administration of the taxes on alcohol to TAX should happen simultaneously.

Fuels Tax and International Fuels Tax Agreement • TAX examined the feasibility of collecting the Fuels Tax and the Road Tax on Motor Carriers collected under the International Fuels Tax Agreement (“IFTA”). • IFTA is an agreement between states and Canadian provinces that allows a carrier to register and pay motor fuel road tax in the carrier's home or base state. • Transfer of the Fuels Tax would affect approximately 800 filers, with only 300 remitting tax. • Currently, all reports are filed electronically, and approximately 90% of the tax is paid electronically. • DMV currently uses a vendor provided system for the Fuels Tax, IFTA, and International Registration Plan programs. • TAX anticipates that it would administer the taxes using the same vendor system. Given that this would produce few efficiencies, TAX recommends that DMV continues to administer the Fuels Tax and IFTA program.

Motor Vehicle Rental Taxes • TAX examined the feasibility of administering the rental taxes. • Transfer of the tax collection would affect 480 taxpayers who file monthly paper returns with DMV for the three rental taxes. • While the current administrative cost to DMV for the administration of the vehicle rental taxes is minimal, DMV does not receive any revenues from the tax for the administration of the tax. • TAX would be able to automate the collection of the taxes but would need to recover its direct costs of administering the taxes from the revenues collected. • TAX recommends transferring the administration of the rental taxes to TAX provided that a funding source is identified.

Motor Vehicle Sales and Use Tax on Manufactured Homes • TAX examined the feasibility of collecting the Motor Vehicle Sales and Use Tax on manufactured homes. DMV would continue to administer the tax on other motor vehicles. • If manufactured houses are not exempted from the titling process or subject to a different tax, taxpayers would have to obtain titles from DMV while remitting the tax to TAX under this proposal. • The issue of the titling process for manufactured houses must be considered when determining the feasibility of transferring the administration from DMV to TAX. • Recommendation: TAX does not recommend the transfer of the administration of the tax on manufactured housing to TAX unless the issue of changing the titling process is first resolved.

Insurance Premium Tax TAX examined the feasibility of collecting the insurance premium tax. Collection of this tax could be moved to TAX in a 3-step process. Legislation would be needed for all of these changes. • Short-term TAX could provide the processing of the returns, the handling of the payments, and any related billing. The SCC would continue to provide customer services and perform the collections and auditing duties. • Intermediate-term TAX could assume the collections responsibilities for this tax. • Long-term TAX could take over the complete administration of this tax. This plan would require study, including surveying stakeholders and determining if it would be necessary to transfer staff from the SCC over to TAX in order to preserve the level of expertise.

Consumption Taxes on Natural Gas & Electric Service • In order to centralize tax administration, the processing and audit functions for these consumption taxes could be moved to TAX. • This would involve close communication between TAX and the SCC: • The information from the returns would still need to be sent to the SCC. • Taxpayers would communicate with staff at the SCC. • The special regulatory tax and the information for that tax would need to be transmitted to the SCC. • Because of the low volume of taxpayers and the lack of potential cost savings or increased efficiencies, TAX does not recommend this change.

Unemployment Insurance Tax • VEC administers the Unemployment Insurance (“UI”) Tax paid by employers. TAX examined the feasibility of collecting the UI Tax. • The close linkage between the administration of the benefits and the tax has led to VEC administering both. Additionally, the federal government pays for VEC’s administration of both the benefits and tax out of revenue from a similar federal tax. • TAX has advantages in collections, such as the power to issue liens, and may be more efficient in collecting delinquent UI Tax. • Recommendations: A comprehensive study should be undertaken to determine whether transferring the UI Tax from VEC to TAX is feasible and desirable. TAX also recommends transferring the collections of delinquent UI Tax to TAX. Legislation would be necessary to transfer the collections of delinquent UI Tax over to TAX.

Postpaid Wireless E-911 Surcharge • TAX examined the feasibility of administering the wireless E-911 surcharge. • Transfer of the collection of the wireless E-911 surcharge would affect 42 wireless service carriers and resellers. • TAX already has a Communications Tax audit unit, which would relieve the Board of the necessity of establishing an audit process and taxpayers would not be subject to two audits of the same information. • Recommendations: Short-Term TAX should take over the collection of the wireless E-911 surcharge. Intermediate-Term TAX recommends that the General Assembly study the feasibility of TAX distributing the wireless E-911 surcharge revenues and moving the Wireless E-911 Services Board functions to TAX, focusing on tax collection, formula-based distribution, the technical aspects of wireless E-911, and the necessity of the grant program.