Download

1 / 21

230 likes | 580 Views

Perfect Competition and Monopoly. Perfect Competition. Conditions: Large number of buyers and sellers Homogeneous product Perfect knowledge Free entry and exit No government intervention Key Implications: Flat firms’ demand determined by market equilibrium price

E N D

Perfect Competition Conditions: • Large number of buyers and sellers • Homogeneous product • Perfect knowledge • Free entry and exit • No government intervention Key Implications: • Flat firms’ demand determined by market equilibrium price • Market participants are price takers without any market power to influence prices (have to charge MR = P = MC) • In the short run firms earn profits or losses or shut down • In the long run profit = normal = 0 (firms operate efficiently)

Unrealistic? Why Learn? • Many small businesses are “price-takers”.Decision rules for such firms are similar to those of perfectly competitive firms • It is a useful benchmark • Explains why governments oppose monopolies • Illuminates the “danger” to managers of competitive environments • Importance of product differentiation • Sustainable advantage

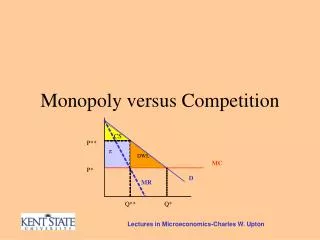

Setting Price SM DM $ TR Qf(units) $ $ Df = Pf = AR = MR PM QM(106) Qf(units) Firm Market

Setting Output To maximize total profit: T = TR - TCFONC: dT/dQ = M = MR - MC = 0In general (including monopoly) MR = MC.In perfect competition MR = P = MC. To maximize profit increase output (Q) until 1) MR = P = MC (at Q*), and2) for Q > Q* => MC > MR => M < 0 => TC < TR or MC is increasing

A Numerical Example • Given estimates of • P = $10 • C(Q) = 5 + Q2 • Optimal Price? • P = $10 • Optimal Output? • MR = P = $10 = 2Q = MC • Q = 5 units • Maximum Profits? • PQ - C(Q) = 10(5) - (5 + 25) = $20

Normal Profit • Normal profit is necessary for the firm to produce over the long run and is considered a cost of production • Normal profit is required because investors expect a return on their investment. • Profit < normal leads to exit in the long run. • Profit > normal leads to entry in the long run. • Profit = normal maintains the # of firms in the industry.

Shut-Down Point • In the long run all cost must be recovered. • In the short run fixed cost incurred before production begins and do not change regardless of the level of production (even for Q = 0). • Shut down only if: –TFC > T (total) P < AVC (per unit). • TFC = AFC*Q = (SAC – AVC)*Q • Operate with loss if: 0 > T > –TFC (total) SAC > P AVC (per unit). • This is the third T maximizing condition.

$ $ S S* Entry Pe Df Pe* Df* D QM Qf Firm Market Effect of Entry on Market Price & Quantity • Short run profits leads to entry • Entry increases market supply, driving down the market price and increasing the market quantity

Effect of Entry on Firms Output & Profit LMC $ LAC Pe Df Df* Pe* Q QL Qf* • Demand for individual firm’s product and hence its price shifts down • Long run profits are driven to zero

Perfect Competition in the Long Run • Socially efficient output and price: MR = P = MC (no dead weight loss) • Efficient plant size: P = MC = min AC (all economies of scale exhausted) • Optimal resource allocation: T = Normal = 0, for P = MC = min AC (opportunity cost = TR, lowered by free entry)

Monopoly Conditions: • Large number of buyers and one sellers • Product without close substitutes • Perfect knowledge • Barriers to entry • No government intervention Key Implications: • Downward sloping firm’s demand is market demand • Firm has market power and determines market price (can charge P > MR = MC) • In the short run monopoly earns profit or loss or shuts down • In the long run profit > normal is sustainable indefinitely but even with profit = normal = 0 (monopoly does not operate efficiently)

Sources of Monopoly Power Natural: • Economies of scale and excess capacity • Economies of scope and cost complementarities • Capital requirements, sales and distribution networks • Differentiated products and brand loyalty Created: • Patents and other legal barriers (licenses) • Tying and exclusive contracts • Collusion (tacit or open) • Entry limit pricing (predatory pricing illegal)

Natural Monopoly Economies of scale exist over the entire LAC curve.One firm distributes 4 million kWh at ¢5 a kWh.This same total output costs ¢10 a kWh with two and ¢15 a kWh with four firms.Natural monopoly: one firm meets the market demand at a lower cost than two or more firms.Public utility commission ensures that P = LAC (not P associated with MR = MC), eliminating monopoly rent. 15 Price (cents per kilowatt-hour) 10 5 LAC D=P 0 1 2 3 4 Quantity (millions of kilowatt-hours)

Consumer surplus Efficient quantity Producer surplus Perfect Competition Price S = MC > min AVC PPC D = P = MR 0 Quantity QPC

Consumer surplus Deadweight loss Monopoly gain Producer surplus Inefficiency of Monopoly Price S = MC > min AVC PM PPC MR D = P 0 QM QPC Quantity

Monopoly in the Long Run with Greater than Normal and Normal Profit • Socially inefficient: P > MR = MC (QM<QPC, PM>PPC, dead weight loss) • Scale inefficient: P > MC = min AC (economies of scale still exist) • Misallocated resources: even whenT = normal = 0, P isstill > min AC (because of market power or barriers to entry opportunity cost < TR) • Encouraged R&D, benefits from natural monopolies, economies of scope and cost complementarity might offset inefficiencies

You are a price taker, other firms charge $40 per unit? P = MR = 40 = 8Q = MC => Q* = 5 and P* = 40 Max T = TR - C(Q*) = 40(5) - (125+4(5)2) = 200 - 225 = -$25 Expect exit in the long-run You are a monopolist with inverse demand P = 100 – Q? MR = 100 - 2Q = 8Q = MC => Q* = 10 and P* = 100 - Q = 100 - 10 = 90 Max T = TR - C(Q*) = 90(10) - (125+4(100)) = 900 - 525 = $375 No entry until barriers eliminated Synthesizing Example C(Q) = 125 + 4Q2 => MC = 8Q is unaffected by market structure. What are profit maximizing output & price, and their implications if