Download

1 / 23

230 likes | 436 Views

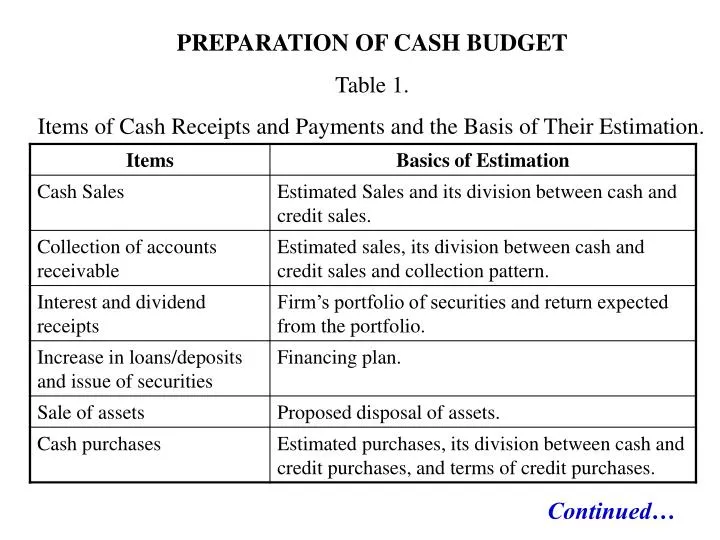

PREPARATION OF CASH BUDGET Table 1. Items of Cash Receipts and Payments and the Basis of Their Estimation. Continued…. Continued…. Problem on Cash Budgeting.

E N D

PREPARATION OF CASH BUDGET Table 1. Items of Cash Receipts and Payments and the Basis of Their Estimation. Continued…

Problem on Cash Budgeting Given below are the estimated details of Nagpur Company Ltd., from which you have to prepare the cash budget for three months – April, May and June,200X.

Some more information is given below: • The company gives one month credit to its customers, 50% of the sales are on credit. • 5% commission is given on all sales. • 2% cash discount is given on cash sales. • 60% of the purchases are on credit and the company gets two months credit from the suppliers. • Payment of the manufacturing overheads is normally delayed by 15 days. • The company will purchase furniture worth Rs. 40,000 on 01-05-200X with a down-payment of Rs. 20,000 and the remaining in two equal monthly installments in the immediately following months. • Advance tax of Rs.6,000 will have to be paid on 01-06-200X. • The company will sell old plant worth Rs. 25,000 for Rs. 18,000 on –06-06-200X. • Ten employees are going to retire on 31st March and total gratuity due to them in May amounts to Rs. 1,10,000. • Bank overdraft facility is available. • Cash-in-hand on 01-04-200X is Rs.12,000. • You can make the necessary logical assumptions.

Nagpur Company LtdQuarterly Cash Budget for April, May & June, 200X.

Working Notes • A cash budget is actually a combined statement of cash and bank accounts. Hence, the opening balance (on the 1st day of the month) and the closing balance (on the last day of the month) are the total of cash and bank balances. The closing balance of April will become the opening balance of May and so on. A negative balance means a bank overdraft. • 50% of sales are for cash, i.e. 50% of the sales for a month will be collected in the same month. But 2% cash discount is given on cash sales, i.e. 98% of cash sales are actually collected.Example Rs. April Sales 80,000 50% on Cash 40,000 Less: 2% cash discount 800Net Cash Sales Collection 39,200 Continued

Remaining 50% of sales are on credit and the company gives one month credit to its customers, i.e. credit sales of April will be collected in May and so on. Hence, credit sales of Rs. 60,000 (50% of Rs. 1,20,000 for March are shown as collected in April and so on, Hence, credit sales of Rs. 60,000; 50% of Rs. 1,20,000) for March are shown as collected in April and so on.(III) It is assumed here that sales commission at 5% is given on respective month’s sales in the same month, irrespective of the collection of credit sales in the next month, i.e. 5% commission on April sales of Rs. 80,000 amount to Rs. 4,000 and it will be paid in April because sales of Rs. 80,000 are achieved in April. Continued

(IV) As stated earlier, the cash budget has to show payments and receipts on account of daily business transactions or revenue payments and receipts and for purchase/sale of fixed or long-term assets, i.e. capital payments and receipts. The plant costing Rs. 25,000 will be sold for Rs.18,000 in June. The cash budget has to exhibit actual or net receipts or payments. Hence, Rs. 18000 is shown as an item of receipt in June and not Rs. 25,000 or loss of Rs. 7,000. Rs.20,000 is paid for the furniture on the date of its purchase (01-05-200X) and the remaining Rs. 20,000 in two equal monthly installments, i,.e. Rs.10,000 in June and the remaining Rs. 10,000 in July. Continued

(V) 40% of the purchases are for cash, i.e. these purchases will be paid immediately in cash. 60% of the purchases are on credit for which the suppliers give two months’ credit, i.e. credit purchase of February will be paid in April and so on. Hence, 60% of the purchases worth Rs. 60,000 of February (Rs. 36,000) are shown as ‘payment of credit purchases’ in April(VI) Payment of the manufacturing overheads will be delayed by 15 days, i.e. the overheads of the first fortnight of April will be paid in its second fortnight and the second fortnight’s overheads will be paid in the first fortnight of May and so on. Hence, Rs. 3,000 due in March (second fortnight) + Rs. 2,000 due in April (First fortnight) will be paid in the first and second fortnights of April, respectively. Continued

The total payments in April against manufacturing overheads amount to Rs. 5,000. The same rule applies to other months. Here it is assumed that the same amount of overhead is incurred every day in a month. (VII) Wages and administrative salaries for a month will be in the same month; as no information to the contrary is available. It is given in the problem that advance tax will be paid on 1st June and gratuity in May, so the payments are shown in the respective months. Continued

ILLUSTRATION FOR PREPARATION OF CASH BUDGET ABC Co. manufactures razor blades. Its estimated sales for the period January, 200X through June 200X are as follows: Rs. 1,00,000 per month from January through March and Rs. 1,20,000 per month from April through June. The sales for November & December of the previous year have been Rs. 1,00,000 each. Cash and credit sales are expected to be 20% & 80% respectively. The receivables from credit sales are expected to be collected as follows: 50% of receivables on an average one month from the date of sale & the balance 50% of receivables, on an average two months from the date of sale. No bad debt losses are expected to occur. Other anticipated receipts are: (1) Rs. 5000 from the sale of a machine in March & (ii) Rs. 2000 interest on securities in June. Given the information tabulate the forecasted each receipts. Continued…

Continued… Now consider the forecast of cash payments: ABC Co. plans to purchase the material worth Rs. 40,000 in January & February and material worth Rs. 48,000 in March & April. The payments for these purchases are made approximately a month after the purchase. The purchases for the month of December of the previous year have been Rs. 40,000 for which payments will be made in January 200X. Miscellaneous cash purchases of Rs. 2000 per month are planned for January through June. Manufacturing expenses are expected to be Rs. 20,000/- month. Continued…

Continued… General administration and selling expenses are expected to be Rs. 10,000- month. Dividend & Tax payment of Rs. 20,000 each is expected to be scheduled in June 200X. A machine worth Rs. 50,000 is proposed to be purchased on cash in March 200X Tabulate the proposed cash payments. Summaries the two tables to calculate the cash surplus/ deficit month wise for ABC co. Assume that the cash balance on 1st January 200X is Rs. 22,000 and the minimum cash balance required by the firm is Rs, 20,000. Continued…

The management can avoid this shortage by adopting one or more of the following means: • (i) Postponement of asset acquisition to April, • Deferring a position of the payment for the capital asset to April & • Resorting to short-term borrowing for the month of March. • Other alternatives like: • Delaying payment to suppliers of material and • Expediting the collection of receivables are also available. Continued

The receipt and payments method of cash forecasting is used commonly due to two advantages: • It provides a complete picture of expected cash flows; and • It is a sound vehicle for exercising control over day to day transactions. However this method has following drawbacks: • Its reliability is impaired by delays in collection or sudden demand for large payments and other similar factors. • It fails to provide a clean picture of important changes in the company’s working capital movement, especially those relating to inventories and receivables. • This method of cash forecasting, resembling the funds flow statement, seeks to estimate the firm’s need for cash at some future date and indicates whether this need can be met with internal resources or not: Continued

Playing The Float To illustrate the game of ‘Playing the float’, let us consider an example. ABC company issues cheques of Rs. 20,000 daily and it takes 6 days for these cheques to be cleared. ABC receives cheques of Rs.20,000 daily and, thanks to its expeditious collection, it takes 4 days for these cheques to be realised. Assuming that there is zero balance to begin with, the balance in the books of the firm and the books of the bank will be as shown in Table 8. From this table we find that a steady state is reached on the seventh day. From thereon the closing balance in the firm’s books would be zero and the closing balance in the bank’s books would be Rs. 40,000. This means that in the steady state situation the firm has a ‘net float’ of Rs. 40,000 and a part of this may be used.