Download

1 / 17

170 likes | 172 Views

Job order costing ppt file asmita publication pp solution

E N D

Cost and Management Accounting CHAPTER-8 JOB ORDER COSTING

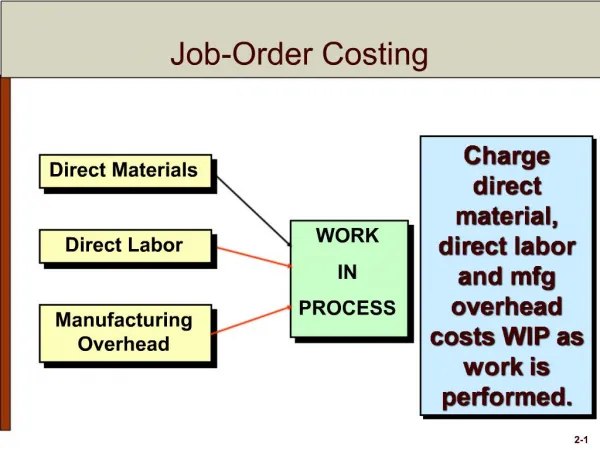

A job is done in a factory. But most of the contract work is done outside a factory as requested by clients. The number of jobs may be more which is not there in contract costing. Expenses are absorbed in job costing. Site expenses are charged directly in contract costing. Time frame in a job is comparatively shorter in comparision with contract costing. Job order costing fixes the cost of particular job/work. Each type of work constitutes a job and the price of each job is determined separately. Job order costing is the system that determines the cost of job received from a client. PRESENTED BY: SHIBA PRASAD DAHAL

Direct Material • Direct Labour • Direct Expenses • Overheads. • Manufacturing Overheads • Non Manufacturing Overheads • Cost of Goods Manufactured: • =Opening WIP + Manufacturing Cost –Closing WIP • Cost of goods sold= Opening balance of Finished goods+ Cost of goods manufactured – CLosing Stock of Finished goods PRESENTED BY: SHIBA PRASAD DAHAL

SP-1 • Job Cost sheet for job No. 101 Working Note: Profit= Cost X Profit% /(100-Profit%) profit= 9000 X10/(100-10)= 90000/90=1000 PRESENTED BY: SHIBA PRASAD DAHAL

EP-1 • Job Cost sheet PRESENTED BY: SHIBA PRASAD DAHAL

EP-2 • Job Order Cost sheet PRESENTED BY: SHIBA PRASAD DAHAL

EP-3 Nischal Company • Job Order Cost sheet Job Order No. 205 Name Of Customer: .. Particulars of Job: … Quantity:… Customer Ref No. Date Of Commencement Date of Completion:….. PRESENTED BY: SHIBA PRASAD DAHAL

EP-4 Muskan Company • Job Order Cost sheet Job Order No. 206 Name Of Customer: .. Particulars of Job: … Quantity:… Customer Ref No. Date Of Commencement Date of Completion:….. PRESENTED BY: SHIBA PRASAD DAHAL

EP-5 X Ltd. Company • Job Order Cost sheet Job Order No. 204 Name Of Customer: .. Particulars of Job: … Quantity:… Customer Ref No. Date Of Commencement Date of Completion:….. PRESENTED BY: SHIBA PRASAD DAHAL

EP-6 X Ltd. Company • Job Order Cost sheet Job Order No. 105 Name Of Customer: .. Particulars of Job: … Quantity:… Customer Ref No. Date Of Commencement Date of Completion:….. PRESENTED BY: SHIBA PRASAD DAHAL

EP-7 Saumya Ltd. Company • Job Order Cost sheet Customer Ref No. Date Of Commencement Date of Completion:….. Job Order No. 222 Name Of Customer: .. Particulars of Job: … Quantity:… a: Solution PRESENTED BY: SHIBA PRASAD DAHAL

b. Cost of goods Manufactured: =Opening Stock of WIP + Total manufacturing cost – Closing stock of WIP. =Rs.(1000+ 7500-2500) =Rs. 6000 c. Cost of goods sold: =Opening stock of finished goods + Cost of goods Manufactured – Closing stock of finished goods. = Rs.( 3500+6000-2000) = Rs. 7500 d. Job order Price: =Cost of goods sold + Profit = Rs. (7500 + 7500*20%) =Rs.(7500 + 1500) =Rs. 9000

LQ-1 Muskan Ltd. • Job Order Cost sheet Customer Ref No. Date Of Commencement Date of Completion:….. Job Order No. 103 Name Of Customer: .. Particulars of Job: … Quantity:… a: Solution PRESENTED BY: SHIBA PRASAD DAHAL

b. Cost of goods Manufactured: =Opening Stock of WIP + Total manufacturing cost – Closing stock of WIP. =Rs.(500+ 16500-1000) =Rs. 16000 c. Cost of goods sold: =Opening stock of finished goods + Cost of goods Manufactured – Closing stock of finished goods. = Rs.( 2000+16000-500) = Rs. 17500 d. Job order Price: =Cost of goods sold + Profit = Rs. 17500 + 17500*12.5%/(100-12.5)% =Rs.(17500 + 2500) =Rs. 20000

LQ-2 A Company • Job Order Cost sheet Customer Ref No. Date Of Commencement Date of Completion:….. Job Order No. 222 Name Of Customer: .. Particulars of Job: … Quantity:… a: Solution PRESENTED BY: SHIBA PRASAD DAHAL

b. Cost of goods sold: =Opening stock of finished goods + Cost of goods Manufactured – Closing stock of finished goods. = Rs.( 6000+36000-12000) = Rs. 30000 c. Job order Price: =Cost of goods sold + Profit = Rs. (30000 + 30000*25%) =Rs.(30000 + 7500) =Rs. 37500 THANK YOU THE END