Download

1 / 17

170 likes | 322 Views

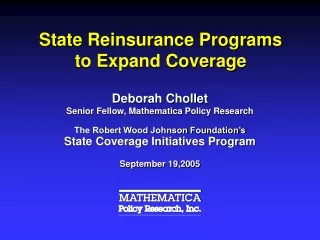

How States Are Trying To Expand Employer Sponsored Health Coverage. John M. Colmers Secretary Department of Health and Mental Hygiene. Percentage of All Firms Offering Health Benefits, 1999-2007*. Background. Majority of individuals get their health insurance from their employers

E N D

How States Are Trying To Expand Employer Sponsored Health Coverage John M. Colmers Secretary Department of Health and Mental Hygiene

Percentage of All Firms Offering Health Benefits, 1999-2007*

Background • Majority of individuals get their health insurance from their employers • Recent declines in employer sponsored insurance (ESI) account for much of growth in the uninsured • ESI still centerpiece of nation’s health financing system • $200 billion in federal tax incentive to purchase insurance through employers • ERISA has made it difficult for states to mandate employer coverage • Voluntary measures to increase number of individuals who get ESI have had limited success

ERISA • Adopted in 1974 to allow multi-state employers to offer comparable benefits across state lines • Preempted state regulation of employee benefits plan • Federal DOL did not issue regulations for health coverage as it did for pensions • Net effect: exempted health benefits offered by self-funded employers from any regulatory oversight • Does not allow for state waivers

ERISA Legal Framework • Preemption • ERISA preempts any state law that either refers explicitly to ERISA plans or have substantial financial or administrative impact • “Savings” Clause • States can regulate the terms and conditions of health insurance among traditional insurance carriers conducting traditional insurance business • “Deemer” Clause • Statute prohibits states from regulating plans that “self-insure” i.e. bearing primary insurance risk

Employer Mandates • Most unlikely to withstand an ERISA challenge • Border issues • Massachusetts and Vermont have modest “fair share” assessment

Pay or Play • Requires an employer to pay an assessment (whose proceeds partially finance a publicly-administered health coverage program). • But will provide a credit against that assessment for the amount of employee health care costs. • Doesn’t bind plan administrators to a particular choice

Maryland Fair Share Share Health Care Fund Act • Gave employers with 10,000 or more employees a choice: • Spend at least 8% (6% for non-profits) of payroll on health insurance costs or • Pay the difference into a fund that supports Medicaid program • Challenged in court by Retail Industry Leader Association (RILA) • Struck down by federal district court and upheld by fourth circuit • Retail Industry Leaders Ass'n v. Fielder, 4th Cir., No. 06-1840 (January 17, 2007).

Massachusetts and Vermont • Employers with more than 8-10 employees must set up tax code section 125 plans • Contribute “fair share” assessment if do not offer fair and reasonable amount toward employee health insurance • Pay free rider surcharge for uncompensated care costs their employees or dependents incur

Recommendations for Modifications to ERISA • Explicitly allow states to apply premium taxes to employer plans.

Recommendations for Modifications to ERISA • Allow states to collect data from ERISA plans.

Recommendations for Modifications to ERISA • Set a federal floor on benefits. Because of ERISA preemption states are not able to define the scope of benefits provided by ERISA plans.

Recommendations for Modifications to ERISA • Strengthen consumer protections for those covered by ERISA plans.

State efforts to increase ESI through subsidies • Most other state efforts to increase ESI have spotty record • Key points • Any subsidy must be significant • Subsidy must be seen as secure over time • Program design must be simple and straightforward • Minimize impact on current distribution system

What is Maryland Doing?Working Families and Small Business Health Coverage Act • Assist very small low wage firms to offer insurance • To be eligible for a subsidy to purchase insurance, the employer must be: • A very small firms (2-9 full time employees) • Have average wages below about ~$50K • Have not offered insurance to their employees in the previous 12 months • Willing to offer health insurance benefits that include the wellness benefit design and Section 125 premium-only plan so that the employee’s contribution to premium is excluded from income and not taxed • Benefits • Maximum premium subsidy for each low wage employee will be the lower of $2000 or 50% of the premium • Subsidy will be divided between the employer and the employee based on the contribution each makes toward the premium • Enrollment is capped to stay within a budget of $30 M

What is Maryland Doing?Working Families and Small Business Health Coverage Act • Expand Medicaid Coverage for very poor adults • Year 1: Expand coverage to parents with family incomes up to 116% FPL ($20K/family 3) • Year 2-3: Expand services to Primary Adult Care program – childless adults under 116% FPL ($12K for individual) • Year 4: Full Medicaid coverage for all poor adults to 116% FPL

Final Remarks • More employers are moving to self-funded plans • Increase in the number of individuals who are in plans that have no state and limited federal regulation • ERISA makes health reform strategies all the more challenging • All eyes on MA and VT