Download

1 / 47

480 likes | 570 Views

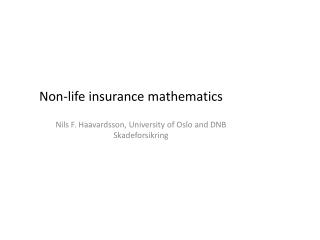

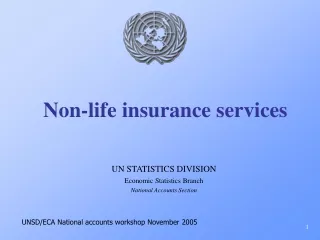

Non-life insurance mathematics. Nils F. Haavardsson, University of Oslo and DNB Skadeforsikring. Key ratios – claim frequency. The graph shows claim frequency for all covers for motor insurance Notice seasonal variations , due to changing weather condition throughout the years.

E N D

Non-lifeinsurancemathematics Nils F. Haavardsson, University of Oslo and DNB Skadeforsikring

Key ratios – claimfrequency • The graph shows claimfrequency for all covers for motor insurance • Noticeseasonalvariations, due to changingweatherconditionthroughouttheyears

The model (Section 8.4) • The idea is to attributevariation in to variations in a setofobservable variables x1,...,xv. Poissonregressjon makes useofrelationshipsofthe form (1.12) • Why and not itself? • The expectednumberofclaims is non-negative, where as thepredictoronthe right of (1.12) can be anythingonthe real line • It makes more sense to transform so thattheleft and right side of (1.12) are more in line witheachother. • Historical data areofthefollowing form • n1 T1 x11...x1x • n2 T2 x21...x2x • nnTn xn1...xnv • The coefficients b0,...,bvareusuallydetermined by likelihoodestimation Claimsexposurecovariates

Introduction to reserving Non-lifeinsurance from a financialperspective: for a premium an insurancecompanycommitsitself to pay a sum if an event has occured Contractperiod retrospective prospective Policy holder signs up for an insurance During thedurationofthe policy, someof thepremium is earned, some is unearned • How muchpremium is earned? • How muchpremium is unearned? • Is theunearnedpremiumsufficient? Premium reserve, prospective Policy holder payspremium. Insurance company starts to earnpremium During thedurationofthe policy, claimsmight or might not occur: • How do wemeasurethenumber and sizeofunknownclaims? • How do weknowifthe reserves onknownclaimsaresufficient? Claims reserve, retrospective Accident date Reporting date Claims payments Claimsclose Claims reopening Claims payments Claimsclose

Imagine youwant to build a reserve risk model Therearethreeeffectsthatinfluencethe best estimat and theuncertainty: •Paymentpattern •RBNS movements •Reporting pattern Up to recentlytheindustry has basedmodelonpaymenttriangles: Whatwillthefuturepaymentsamount to? ?

The ultimate goal for calculatingthe pure premium is pricing Pure premium = Claimfrequency x claimseverity Parametric and non parametricmodelling (section 9.2 EB) The log-normal and Gamma families (section 9.3 EB) The Pareto families (section 9.4 EB) Extreme valuemethods (section 9.5 EB) Searching for themodel (section 9.6 EB)

Claimseveritymodelling is aboutdescribingthevariation in claimsize • The graphbelow shows howclaimsizevaries for fire claims for houses • The graph shows data up to the 88th percentile • How do we handle «typicalclaims» ? (claimsthatoccurregurlarly) • How do we handle largeclaims? (claimsthatoccurrarely) Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Claimseveritymodelling is aboutdescribingthevariation in claimsize • The graphbelow shows howclaimsizevaries for water claims for houses • The graph shows data up to the 97th percentile • The shapeof fire claims and water claimsseem to be quite different • Whatdoesthissuggestaboutthe drivers of fire claims and water claims? • Anyimplications for pricing? Non parametric Log-normal, Gamma The Pareto Extreme value Searching

The ultimate goal for calculatingthepure premium is pricing • Claimsizemodellingcan be parametricthrough families ofdistributionssuch as the Gamma, log-normal or Pareto with parameters tuned to historical data • Claimsizemodellingcanalso be non-parametricwhereeachclaimziofthepast is assigned a probability 1/n of re-appearing in thefuture • A newclaim is thenenvisaged as a random variable for which • This is an entirely proper probabilitydistribution • It is known as theempiricaldistribution and will be useful in Section 9.5. Non parametric Log-normal, Gamma The Pareto Sizeofclaim Client behavourcanaffectoutcome • Burglar alarm • Tidyship (maintenanceetc) • Garage for thecar Bad luck • Electric failure • Catastrophes • House fires Extreme value Where do wedraw the line? Searching Here we sample from theempiricaldistribution Here weusespecial Techniques (section 9.5)

Example Non parametric Empirical distribution Log-normal, Gamma • The thresholdmay be set for example at the 99th percentile, i.e., 500 000 NOK for thisproduct • The threshold is sometimescalledthelargeclaimsthreshold The Pareto Extreme value Searching

Scale families ofdistributions • All sensible parametricmodels for claimsizeareofthe form • and Z0 is a standardized random variable corresponding to . • This proportionality os inherited by expectations, standard deviations and percentiles; i.e. ifareexpectation, standard devation and -percentile for Z0, thenthe same quantities for Z are • The parameter canrepresent for exampletheexchange rate. • The effectof passing from onecurrency to anotherdoes not changetheshapeofthedensityfunction (iftheconditionabove is satisfied) • In statistics is known as a parameter ofscale • Assumethe log-normal modelwhere and are parameters and . Then . Assumewerephrasethemodel as • Then Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Fitting a scalefamily • Models for scale families satisfy • wherearethedistributionfunctionsof Z and Z0. • Differentiatingwithrespect to z yieldsthefamilyofdensityfunctions • The standard wayof fitting suchmodels is throughlikelihoodestimation. If z1,…,znarethehistoricalclaims, thecriterionbecomes • which is to be maximizedwithrespect to and other parameters. • A usefulextension covers situationswithcensoring. • Perhapsthesituationwheretheactual loss is only given as somelowerbound b is most frequent. • Example: • travel insurance. Expenses by loss oftickets (travel documents) and passportarecovered up to 10 000 NOK ifthe loss is not covered by anyoftheotherclauses. Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Fitting a scalefamily • The chanceof a claim Z exceeding b is , and for nbsucheventswithlowerbounds b1,…,bnbtheanalogous joint probabilitybecomes • Takethelogarithmofthisproduct and add it to the log likelihoodofthefullyobservedclaims z1,…,zn. The criterionthenbecomes Non parametric Log-normal, Gamma completeinformation censoring to the right The Pareto Extreme value Searching

Shifteddistributions • The distributionof a claimmay start at sometreshold b insteadoftheorigin. • Obviousexamplesaredeductibles and re-insurancecontracts. • Models can be constructed by adding b to variables starting at theorigin; i.e. where Z0 is a standardized variable as before. Now • and differentiationwithrespect to z yields • which is thedensityfunctionof random variables with b as a lower limit. Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Skewness as simple descriptionofshape • A major issuewithclaimsizemodelling is asymmetry and the right tailofthedistribution. A simple summary is thecoefficientofskewness • The numerator is thethird order moment. Skewnessshould not dependoncurrency and doesn’tsince • Skewness is often used as a simplifiedmeasureofshape • The standard estimateoftheskewnesscoefficient from observations z1,…,zn is Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non-parametricestimation • The random variable that attaches probabilities 1/n to all claimsziofthepast is a possiblemodel for futureclaims. • Expectation, standard deviation, skewness and percentilesare all closelyrelated to theordinary sample versions. For example • Furthermore, • Third order moment and skewnessbecomes • Skewnesstends to be small • No simulatedclaimcan be largeerthanwhat has beenobserved in thepast • These drawbacks implyunderestimationof risk Non parametric Log-normal, Gamma The Pareto Extreme value Searching

TPL Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Hull Non parametric Log-normal, Gamma The Pareto Extreme value Searching

The log-normal family • A convenientdefinitionofthe log-normal model in the present context is • as where • Mean, standard deviation and skewnessare • seesection 2.4. • Parameter estimation is usuallycarriedout by notingthatlogarithmsareGaussian. Thus • and whenthe original log-normal observations z1,…,znaretransformed to Gaussianonesthrough y1=log(z1),…,yn=log(zn) with sample mean and variance , theestimatesofbecome Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Log-normal sampling (Algoritm 2.5) Input: Draw Return Non parametric Log-normal, Gamma The Pareto Extreme value Searching

The lognormalfamily • Different choiceof ksi and sigma • The shapedependsheavilyon sigma and is highlyskewedwhen sigma is not tooclose to zero Non parametric Log-normal, Gamma The Pareto Extreme value Searching

The Gamma family • The Gamma family is an importantfamily for whichthedensityfunction is • It wasdefined in Section 2.5 as is the standard Gamma withmeanone and shapealpha. The densityofthe standard Gamma simplifies to • Mean, standard deviation and skewnessare • and there is a convolutionproperty. Suppose G1,…,Gnareindependentwith • . Then Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Exampleof Gamma distribution Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Hull coverage (i.e., damagesonownvehicle in a collisionor othersudden and unforeseendamage) Time period for parameter estimation: 2 years Covariates: • Driving length • Car age • Region ofcarowner • Tariff class • Bonus ofinsuredvehicle 2 modelsaretested and compared – Gamma and lognormal Example: carinsurance Non parametric Log-normal, Gamma The Pareto Extreme value Searching

The modelsarecomparedwithrespect to fit, results, validationofmodel, type 3 analysis and QQ plots Fit: ordinaryfitmeasuresarecompared Results: parameter estimatesofthemodelsarecompared Validationofmodel: the data material is split in two, independentgroups. The model is calibrated (i.e., estimated) onone half and validatedontheother half Type 3 analysisofeffects: Doesthefitofthemodelimprovesignificantly by includingthespecific variable? Comparisonsof Gamma and lognormal Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Comparisonof Gamma and lognormal - fit Gamma fit Lognormalfit Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Comparisonof Gamma and lognormal – type 3 Non parametric Log-normal, Gamma Gamma fit Lognormalfit The Pareto Extreme value Searching

QQ plot Gamma model Non parametric Log-normal, Gamma The Pareto Extreme value Searching

QQ plot log normal model Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non parametric Log-normal, Gamma The Pareto Extreme value Searching

None ofthemodelsseem to be perfect Lognormalbehavesworst and can be discarded Canwe do better? Wetry Gamma once more, nowexludingthe 0 claims (about 17% oftheclaims) • Claimswherethe policy holder has noguilt (other party is to blame) Conclusions so far Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Comparisonof Gamma and lognormal - fit Gamma fit Gamma without zero claimsfit Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Comparisonof Gamma and lognormal – type 3 Non parametric Log-normal, Gamma Gamma fit Gamma without zero claimsfit The Pareto Extreme value Searching

QQ plot Gamma Non parametric Log-normal, Gamma The Pareto Extreme value Searching

QQ plot Gamma modelwithoutzero claims Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non parametric Log-normal, Gamma The Pareto Extreme value Searching

Non parametric Log-normal, Gamma The Pareto Extreme value Searching