Download

1 / 14

140 likes | 155 Views

2.2 Production Possibilities Frontier. How much can an economy produce with the resources available? What are the economy’s production capabilities?. Simplifying Assumptions.

E N D

2.2 Production Possibilities Frontier • How much can an economy produce with the resources available? • What are the economy’s production capabilities?

Simplifying Assumptions • 1. To reduce the analysis to manageable proportions, the model the output to two broad classes of production: Consumer goods, such as pizzas and haircuts, and Capital goods, such as pizza ovens and hair clippers. • 2. The focus is on production during a given period- (ex. A year) • 3. The resources available in the economy are fixed in both quantity and quality during the period.

continued • 4. Society’s knowledge about how best to combine these resource to produce output-that is, the available technology-does not change during the year. • Point of theses assumptions is to freeze the economy’s resources and technology for a period of time to focus on what possibly can be produced during that time.

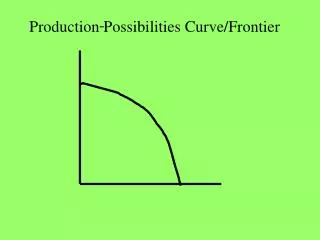

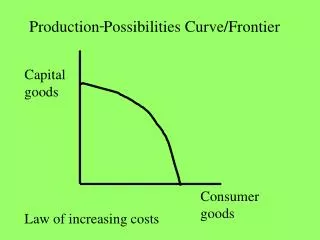

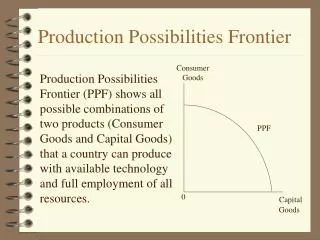

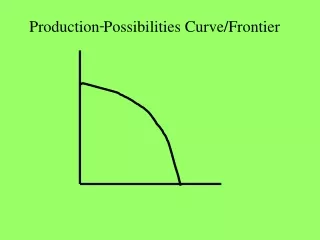

Production possibilities frontier • Shows the possible combinations of the two types of goods that can be produced when available resources are employed fully and efficiently. • Efficiency means producing the maximum possible output from available resources.

Inefficient and unattainable production • Inefficient production- • Look on the board for the PPF Curve • Law of increasing opportunity cost- states that each additional increment of one good requires the economy to give up successively large increments of the other good.

continued • The laws of increasing opportunity cost also applies when moving from the production of capital goods to the production of consumer goods. • When all resources in the economy are making capital goods, certain resources such as cows & farmland are of little use in making capital goods.

Con’t • When resources shift from making capital goods to making consumer goods, few capital goods need be given up initially. • As more consumer goods are produced, resources that are more productive in making capital goods must be used for making consumer goods reflecting the law of increasing opportunity cost.

continued • If resources were perfectly adaptable to the production of both types of goods, the amount of consumer goods sacrificed to make more capital goods would remain constant. • The PPF would be a straight line, reflecting the constant opportunity cost along the PPF

Shifts of the PPF • Economic growth- an expansion in the economy’s production possibilities or stability to produce. • Changes in Resources availability • Work longer hours, retire later, or if the labor is more skilled the PPF shift outward (right)

continued • Increase in other available resources, such as new oil discoveries the shift of the PPF outward (right) • Decrease in availability of quality of resources shifts the PPF inward (left)

Increase in Stock of Capital Goods • An economy’s PPF depends in part on its supply of the stock of capital goods. • The more capital goods an economy produces during one period, the more output it can produce in the next period. • Producing capital goods this period shifts the economy’s PPF outward (right) the next period. • The choice b/w consumers goods and capital goods is really b/w present consumption and future production.

Technological Changes • Shifts the economy’s PPF outward is a technological discovery that employs available resources more efficiently. • Ex. Internet, telephone, fax, email. • Efficiency, the PPF describes the efficient combinations of outputs that are possible, given the economy’s resources and technology.

continued • The second is scarcity. • Given the stock of resources and technology, the economy can produce only so much. • The PPF slopes downward, indicating that,as the economy produces more of one good, it must produce less of the other good. • Trade-off demonstrates opportunity cost. • Bowed-out shape of the PPF reflects the law of increasing opportunity cost.

continued • Shift outward reflects economic growth. • The PPF need choice. • That choice will determine not only current consumption but also the capital stock available next.