Download

1 / 5

50 likes | 59 Views

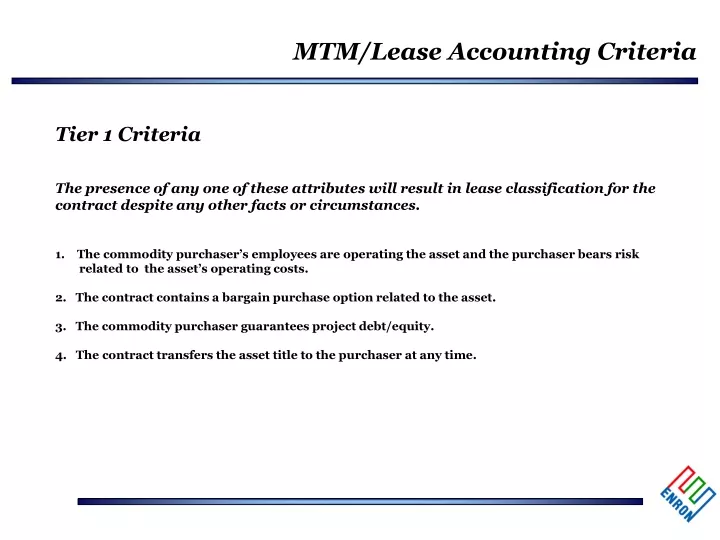

MTM/Lease Accounting Criteria. Tier 1 Criteria The presence of any one of these attributes will result in lease classification for the contract despite any other facts or circumstances. 1. The commodity purchaser’s employees are operating the asset and the purchaser bears risk

E N D

MTM/Lease Accounting Criteria Tier 1 Criteria The presence of any one of these attributes will result in lease classification for the contract despite any other facts or circumstances. 1. The commodity purchaser’s employees are operating the asset and the purchaser bears risk related to the asset’s operating costs. 2. The contract contains a bargain purchase option related to the asset. 3. The commodity purchaser guarantees project debt/equity. 4. The contract transfers the asset title to the purchaser at any time.

MTM/Lease Accounting Criteria Tier 2 Criteria The criteria included in this category should be analyzed to determine if the contract is effectively disassociated from the asset. If so, the contract presumably does not meet the definition of a lease. 1. The contract contains significant liquidated damage provisions in the event the commodity seller does not perform. Best case scenario would be that the damages are market-based. Market based damages with a cap are acceptable as long as the potential range of applicable damages creates a significant disincentive for nonperformance. 2. The commodity seller has the financial wherewithal to perform under any applicable liquidated damage provisions. 3. The pricing provisions of the contract are at market. 4. Any agreement to supply gas (or other fuel stock) to the asset is at market prices, is for a stated quantity, and has market-based liquidated damage provisions. 5. The specified delivery points pursuant to related contracts are liquid delivery points. 6. The purchaser does not control the operating policies and procedures of the asset.

MTM/Lease Accounting Criteria Tier 2 Criteria (cont.) 7. The contract does not require delivery (either explicitly or implicitly) from a specific asset. It is acceptable to reference a facility as long as delivery from that facility is not required and all other Tier 2 criteria have been met. 8. The contractual quantity is fixed in absolute terms (i.e., quantities are not stated as a percentage of capacity or production, etc.). 9. The commodity purchaser does not bear operational risk related to the facility.

MTM/Lease Accounting Criteria Tier 3 Criteria The criteria in this category are indicative of leases. These criteria should be evaluated using a “preponderance of the evidence” approach when 1) there is no Tier 1 attribute present within the contract or related agreements and 2) the contract is linked to a specific asset based on the Tier 2 evaluation. These criteria are additive to the Tier 2 criteria. Careful analysis should be applied to determine whether the Tier 2 and Tier 3 attributes, taken together, convey the right to use the facility. 1. Virtually all reasonably expected facility output is to be sold to the purchaser for a specified period of time. Notional contract volumes in excess of 70% will typically meet this definition and result in lease classification. Lease classification for contracts specifying less than 70% will be highly dependent on the other factors present in the applicable contracts. (note: the 70% is intended solely as an approximate benchmark and should not be interpreted as a hard, fast rule). 2. The commodity purchaser bears significant risk related to the construction of the specified facilities. 3. The purchaser’s employees are operating the facility. Presence of this attribute will almost always result in lease classification even if operational risk is not conveyed to the purchaser.

MTM/Lease Accounting Criteria Tier 3 Criteria (cont.) 4. The purchaser is responsible for selecting/designing all plant equipment. 5. The commodity purchaser bears the facility’s fuel price and/or availability risk. 6. The present value of the fixed, guaranteed contract payments approximates or exceeds the fair value of the facility. This is a strong indicator which, if present, will probably result in lease classification.