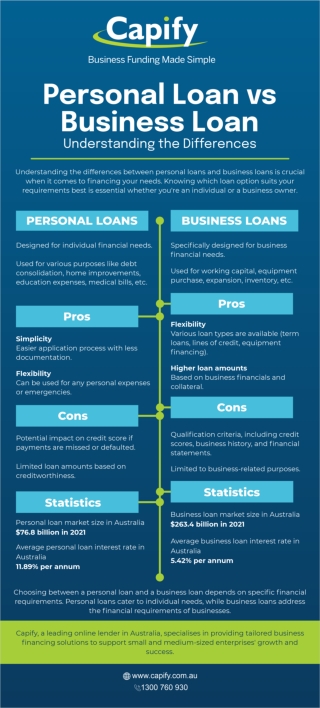

Download

1 / 22

220 likes | 318 Views

Welcome! So you’re looking to finance a car? Before you look at taking out loans make sure that you are financially able to pay for a vehicle.

E N D

Welcome! So you’re looking to finance a car? Before you look at taking out loans make sure that you are financially able to pay for a vehicle. If you think you’re ready, we’re going to learn some important loaning terms, where to get loans, and other legal concerns that may impact your car purchase. The Loan Click to continue

Buying a vehicle is truly an investment. So it’s important to be financial prepared before looking at financing options. Make sure that you have a good FICO /credit score so that you can get a good interest rate on your loan. To learn more about your credit score, credit report, and interest rate, refer to our website or your base’s Personal Finance Management Specialist. The process to get a loan can get rather complicated, so we’re going to give you the basics. But before we get into how to get a loan we need to understand some key terms that come with loans.

When you go to a lending institution – places that loan money, like a bank – they will ask you questions about what you’re looking for in a loan. What you will actually get in the loan depends on your credit history, but you should know what they’re going to ask you about before walking in. Ask the bank associate to explain each of the terms bellow to learn more about it. APR Down payment True Market Value MSRP Balance Incentives Sales tax Dealer’s invoice Payment term Once you feel comfortable with these terms – click next to continue.

Ask the bank associate to explain each of the terms bellow to learn more about it. APR Down payment True Market Value MSRP Balance Incentives Sales tax Dealer’s invoice Payment term APR stands for Annual Percentage Rate. It’s like an interest rate, but it is the rate you pay for the entire loan. So if you have an interest rate of 4% every quarter of a year, your APR would be 16% Once you feel comfortable with these terms – click next to continue.

Ask the bank associate to explain each of the terms bellow to learn more about it. APR Down payment True Market Value MSRP Balance Incentives Sales tax Dealer’s invoice Payment term A down payment is the amount that you pay the dealer upfront for the car before taking a loan. So if you were buying a $20,000 car and put as a down payment $3,000, the loan will be for $17,000 instead. This is a great way to reduce your monthly payments! Once you feel comfortable with these terms – click next to continue.

Ask the bank associate to explain each of the terms bellow to learn more about it. APR Down payment True Market Value MSRP Balance Incentives Sales tax Dealer’s invoice Payment term True Market value (TMV) is the average price of the car you are buying. This is determined by the price similar cars to the one you want have been sold for. The more popular the car is in your area – the higher the TMV, and vice vera. Once you feel comfortable with these terms – click next to continue.

Ask the bank associate to explain each of the terms bellow to learn more about it. APR Down payment True Market Value MSRP Balance Incentives Sales tax Dealer’s invoice Payment term MSRP stands for Manufacturer’s Suggested Retail Price, also known as the “Sticker price”. The manufacturer of the car –not the dealer– determines the MSRP for the base model. The dealer, though, does not have to sell at this price. Once you feel comfortable with these terms – click next to continue.

Ask the bank associate to explain each of the terms bellow to learn more about it. APR Down payment True Market Value MSRP Balance Incentives Sales tax Dealer’s invoice Payment term A loan’s balance is the amount remaining to be paid. It’s what you still owe on the loan. So if you took a loan for $1,000, then paid off $300 of it, your balance would be $700. Once you feel comfortable with these terms – click next to continue.

Ask the bank associate to explain each of the terms bellow to learn more about it. APR Down payment True Market Value MSRP Balance Incentives Sales tax Dealer’s invoice Payment term Incentives are essentially discounts on the overall car price. A dealer will place an incentive or rebates (which is money back on your purchase) on certain cars to try to tempt people into buying that car. Once you feel comfortable with these terms – click next to continue.

Ask the bank associate to explain each of the terms bellow to learn more about it. APR Down payment True Market Value MSRP Balance Incentives Sales tax Dealer’s invoice Payment term You’re probably familiar with sales tax. Anything you buy is taxed – a percentage of the amount you pay goes to the State. Because cars are thousands of dollars, the percentage you’ll pay in sales tax will be much higher – be sure to factor this into your total cost of ownership for a car. Once you feel comfortable with these terms – click next to continue.

Ask the bank associate to explain each of the terms bellow to learn more about it. APR Down payment True Market Value MSRP Balance Incentives Sales tax Dealer’s invoice Payment term A dealer invoice is the price dealers pay for a car from the manufacturer. When a dealer sells you a car they are trying to cover the costs in their dealer invoice too. The cost of having the car moved to the dealership and advertising gets rolled into the price you pay for the car. Once you feel comfortable with these terms – click next to continue.

Ask the bank associate to explain each of the terms bellow to learn more about it. APR Down payment True Market Value MSRP Balance Incentives Sales tax Dealer’s invoice Payment term A payment term is the time you have to pay off the loan. Normally, car loans have a payment term of 36 – 60 months (3 -5 years). The shorter the payment term, the bigger the monthly payment. Once you feel comfortable with these terms – click next to continue.

Loan Central Where should I get a loan? You should feel free to shop around – see who has the best deal for you. If you already know what car you want, you can negotiate this into the loan because you can already specify what kind of car or dealer or what your maximum amount needed for approval would be. If you haven’t decided on a car or dealer yet, it’s still a great idea to get preapproved before going to a dealership to look at cars. You can better manage your budget, compare interest rates, and it simplifies the negotiation process because you have a fixed maximum you can pay on the spot. Now that you’re comfortable with loan terms, your first step to financing your car is to pick a lender. You can find financing for your vehicle in many places: your bank or credit union, dealerships, and online financial institutions.

Loan Central Can I afford the monthly payments? How much overall am I paying in this this loan? This most important things to remember when getting a loan is how much you’re paying in overall costs and if you can make the monthly payments. Once you know how much you want to pay overall and what you can afford monthly you can consider other questions.

Loan Central How much will my APR be? What payment term works best for me to pay off the balance on the loan? How much is the MSRP compared to the True Market Value of the car and the Dealer Invoice? Click here to learn more! How much should I put as a down payment? How much will the car cost after taxes? What are the dealer’s incentives? All these things factor in when you’re taking out a loan. Let’s take one as an example. Other questions could be…

Don’t forget the two biggest questions to ask yourself when getting a loan: How much overall am I paying in this this loan? Can I afford the monthly payments? Loan Central How much will my APR be? What payment term works best for me to pay off the balance on the loan? 0% APR! How much is the MSRP compared to the True Market Value of the car and the Dealer Invoice? How much should I put as a down payment? How much will the car cost after taxes? What are the dealer’s incentives? Dealers often offer 0% APR on a vehicle. But is it a good value? You have to consider other incentives. You may be better off taking a rebate or cash allowance – a discount the dealer or manufacturer will give to lower the final price on the car. This way you have a smaller principal to pay and therefore less interest. Making the overall payment smaller and monthly payments more affordable.

Let’s do a little practice. Which of these lenders is giving you the most affordable loan if you want to pay the lowest monthly payment possible? You may need a calculator! Hi there! Here are your loan conditions… Payment term: 36 months APR: 18% Your down payment: $5,000 Sales tax: 14% Negotiated car price based on TMV: $18,500 Lender 2! Hello! Here are you loan conditions… Payment term: 36 months APR: 21% (but can have 0% for the first 6 months) Your down payment: $5,000 Sales tax: 14% “Buy now” rebate: $1,500 MSRP: $20,000 Having trouble remembering the terms? Click here to download the terms from our website! Lender 1!

Correct! Lender 1 gives you the best loan! Here’s why… Lender 2 Lender 1 Payment term: 36 months APR: 18% Your down payment: $5,000 Sales tax: 14% Negotiated car price based on TMV: $18,500 Payment term: 36 months APR: 21% (but can have 0% for the first 6 months) Your down payment: $5,000 Sales tax: 14% “Buy now” rebate: $1,500 MSRP: $20,000 Because Lender 2 gives us 0% APR for the first 6 months, we have to remove that interest from the APR and we get 17.5% which is 0.48% monthly Sales tax will be tacked on to your monthly payment. So we multiply by 0.14 and divide by the payment term. In each loan you put a $5,000 down payment. So you subtract it to get the car price you are financing. But we want to know the monthly payment so we divide by the payment term. 18,500-5,000= 13,500 13,500/36= 375.00 13,500 * 0.14= 1890/36=52.50 18/36=0.5% .005 .005*13,500= 67.50/36 = $1.87 375.00+ 52.50+ 1.87 =$429.37 20,000-5,000= 15,000 15,000/36= 416.66 13,500 * 0.14= 2100/36=58.33 17.5/36=0.48% .0048 .0048*15,000= 72/36 = $2.00 416.66+ 58.33+ 2.00 =$476.99 Then we add the monthly car payment, tax, and APR to get our monthly total. Everything added together, Lender 1 gives us the most affordable monthly payment. We multiply the monthly APR to the total price and divide by the term.

Actually Lender 1 gives you the best loan! Here’s why… Lender 2 Lender 1 Payment term: 36 months APR: 18% Your down payment: $5,000 Sales tax: 14% Negotiated car price based on TMV: $18,500 Payment term: 36 months APR: 21% (but can have 0% for the first 6 months) Your down payment: $5,000 Sales tax: 14% “Buy now” rebate: $1,500 MSRP: $20,000 Because Lender 2 gives us 0% APR for the first 6 months, we have to remove that interest from the APR and we get 17.5% which is 0.48% monthly Sales tax will be tacked on to your monthly payment. So we multiply by 0.14 and divide by the payment term. In each loan you put a $5,000 down payment. So you subtract it to get the car price you are financing. But we want to know the monthly payment so we divide by the payment term. 18,500-5,000= 13,500 13,500/36= 375.00 13,500 * 0.14= 1890/36=52.50 18/36=0.5% .005 .005*13,500= 67.50/36 = $1.87 375.00+ 52.50+ 1.87 =$429.37 20,000-5,000= 15,000 15,000/36= 416.66 13,500 * 0.14= 2100/36=58.33 17.5/36=0.48% .0048 .0048*15,000= 72/36 = $2.00 416.66+ 58.33+ 2.00 =$476.99 Then we add the monthly car payment, tax, and APR to get our monthly total. Everything added together, Lender 1 gives us the most affordable monthly payment. We multiply the monthly APR to the total price and divide by the term.

Loan Central Can I afford the monthly payments? How much overall am I paying in this this loan? There are a lot of things that go into looking for a good loan. If you want more information, schedule an appointment with the Personal Finance Management Specialist on your base.

Thank you for learning with us! You may now exit. To find out more about any of the topics discussed in this module - contact your base’s Personal Financial Management Specialists.

Bought for $33,600 Sold for $12,000 3 years later Still owe $5,000 on loan. Payment term? The payment term is the amount of time in months you have to pay off the loan –and you get to choose it! However, you have to know what a good payment term is for you. The longer your payment term, the smaller your monthly payment, but that means that you are committed to keep that car for at least that length of time. As soon as you drive your new car off the lot, it loses at lot of value, and will continue to lose value the longer you own it. Let’s say that you got a 60 month loan –that’s 5 years—but 3 years into owning the car you decide that it’s not working out and you’d like to replace it. When you go to sell the car, you won’t be able to sell it or trade it in at the same price that you bought it –you’ll have to sell it at its current value –which means you’ll still owe whatever the difference is. So let’s take this car for example. If you bought this car for $33,600 and you try to sell it 3 years later, the car has already lost more than half of it’s value. You may be able to sell it for around $12,000 depending on the car’s condition. But you’ll still owe the difference between what you sell it for and what you still owe on the loan. In this example, you’d still owe $5,000. This is what makes buying a car is an investment –you’re going to want to pick a car that you’ll want to use even after you finish paying off the loan. That’s why it’s important to make sure you are financially able to pay off the loan within the payment term and to research and learn as much as you can about owning that car.