Download

1 / 6

60 likes | 137 Views

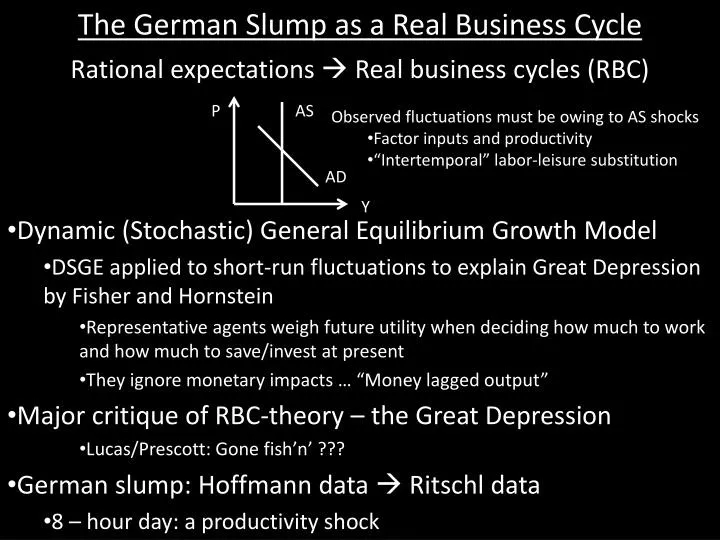

P. AS. Observed fluctuations must be owing to AS shocks Factor inputs and productivity “ Intertemporal ” labor-leisure substitution. AD. The German Slump as a Real Business Cycle. Y. Rational expectations Real business cycles (RBC) Dynamic (Stochastic) General Equilibrium Growth Model

E N D

P AS • Observed fluctuations must be owing to AS shocks • Factor inputs and productivity • “Intertemporal” labor-leisure substitution AD The German Slump as a Real Business Cycle Y Rational expectations Real business cycles (RBC) Dynamic (Stochastic) General Equilibrium Growth Model DSGE applied to short-run fluctuations to explain Great Depression by Fisher and Hornstein Representative agents weigh future utility when deciding how much to work and how much to save/invest at present They ignore monetary impacts … “Money lagged output” Major critique of RBC-theory – the Great Depression Lucas/Prescott: Gone fish’n’ ??? German slump: Hoffmann data Ritschl data 8 – hour day: a productivity shock

Fisher – Hornstein: DGE model of Germany, 1928-37 • All per capita variables relative to real gdp trend (in equilibrium, they should grow at same rate) • Measure total factor productivity (TFP) as Solow residual: Y = A Kα L(1- α) dA/A = TFP growth = dY/Y – αdK/K – (1 - α) dL/L • Ignore M1 … it lagged Y • Ignore how lower interest rate might have stimulated investment, output and employment (recall Voth) Note • Wages set by collective bargaining and arbitration Political Wage Wages too High? (Borchardt) • Bruening austerity policy • Nazis broke unions (1933) – set maximum wages and limited mobility Bruening lowered civil servant wages and tried to reduce private sector wages • Nazi expansion with limits to consumption Military Keynesianism?

Fisher – Hornstein Model • Representative agent maximizes discounted utility over infinite horizon • Utility increase with consumption and leisure • Leisure decreases with fraction of time spent working • Spending on consumption (c) plus investment (x) equals income from labor (wn) and capital (rk) plus transfers from government (s) • Expenditure tax rate and income tax rate enter this constraint • Per capita kapital stock increases with investment net of depreciation • Output determined by Cobb-Douglas production function Y = A k.25 [γtn].75 • Labor share of income averaged ¾ • Technology advanced at 1.87% annual rate (γ) • Profit maximizing firm hires factors (n and x) so MPL = w and MPK = r • Government spending g + s = tax revenue over horizon • As always, Y = c + x + g

Fisher – Hornstein Simulations • Response of employment, output, consumption, investment and real wage to alternative values of productivity (trend or actual), fiscal policy (trend or actual), and real wage (market clearing or actual) I – Actual productivity with trend fiscal stance and market clearing wage The actual decline in TFP generates patterns of employment, output, consumption and investment similar to what happened … but to clear labor market, real wage should have declined, not risen, in early years of German depression II – Actual fiscal policy with trend TFP and market clearing real wage Predict not nearly as much contraction of employment, output, consumption and investment as actually occurred from 1928 – 1932. Predict investment crowded out in Nazi years, which it wasn’t. III – Actual real wage with trend TFP and actual fiscal policy Predict less reduction in consumption than actually occurred … but otherwise generate patterns close to actual

Fisher – Hornstein Conclusions • High real wage by itself generates downturn close to actual • Reduced real wage of Nazi years does not by itself capture investment spurt and consumption stagnation • Combinations of actual real wages, Bruening fiscal austerity followed by Nazi expansion, and actual TFP fail to predict sharp decline in consumption in downturn and failure to recover in upturn. • More research is called for.

German Interwar Economic Pathologies: An Overview Lost War and Revolution Distributional Conflict +8 – Hour Day Desperate Government Hyperinflation Stabilization Monetary Constraints Outsized Wages Reduced Investment Depression and Slump Nazi Revolution/Constraints Broken Wages Down Government Spending Up “Recovery”