Download

1 / 14

140 likes | 478 Views

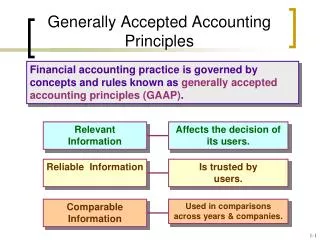

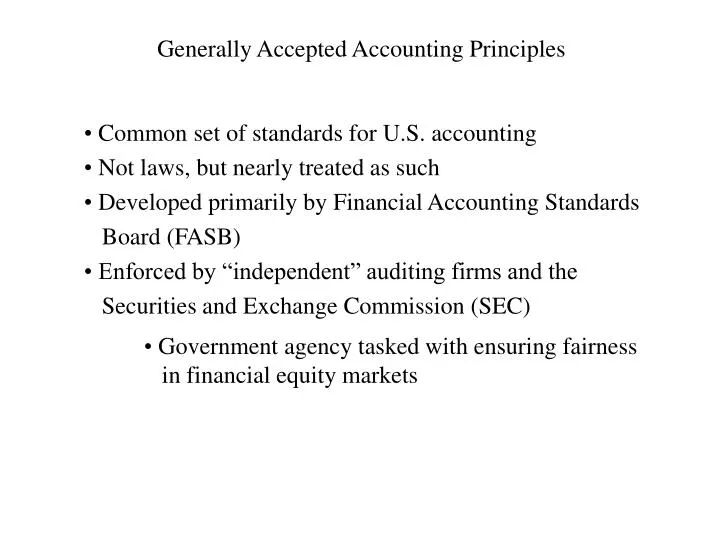

Generally Accepted Accounting Principles. Common set of standards for U.S. accounting Not laws, but nearly treated as such Developed primarily by Financial Accounting Standards Board (FASB) Enforced by “independent” auditing firms and the Securities and Exchange Commission (SEC).

E N D

Generally Accepted Accounting Principles • Common set of standards for U.S. accounting • Not laws, but nearly treated as such • Developed primarily by Financial Accounting Standards • Board (FASB) • Enforced by “independent” auditing firms and the • Securities and Exchange Commission (SEC) • Government agency tasked with ensuring fairness • in financial equity markets

History of Accounting Standards • AICPA first created the Committee on Accounting • Procedure (CAP) • Group of practicing CPAs • Issued 51 Accounting Research Bulletins from 1939-59 • AICPA then created more formal Accounting Principles • Board (APB) • Practicing CPAs, professors, and industry reps • Issued 31 APB Opinions from 1959-73

Financial Accounting Standards Board (FASB) • Formed to deter Congressional standard setting • Most formal type of standard setting board • Full-time board members. No external ties. • Increased independence

Standard Setting Process (Making GAAP) • Board addresses topics in meetings • Research on the topic is conducted and summarized • in discussion memorandum • There is a public hearing on the topic • An exposure draft is written and displayed. Comments • are solicited from any interested party. • Board evaluates comments and then issues final standard. 5 of • 7 votes required to pass.

FASB Products • Standards: Specific accounting rules (GAAP) • Interpretations: Further guidance on prior standards. Also • considered GAAP • Concepts: Fundamental objectives of financial accounting. • An overriding framework on what accounting should be. • Technical Bulletins: guidance on how to implement • standards for particular firms or industries • Emerging Issues Task Force Statements (EITF): guidance • on how to handle confusing or difficult issues Current EITF issues

ARB Research Bulletins APB Opinions FASB Standards (& Interpretations) Most Authority AICPA Accounting Interpretations FASB Question and Answer Guides Industry Practices Least Authority GAAP Authority Structure FASB Technical Bulletins AICPA Industry Audit and Accounting Guides AICPA Statements of Position Emerging Issues Task Force (EITF) Statements AICPA Practice Bulletins

Securities and Exchange Commission (SEC) • Governmental enforcement agency • Collects all mandatory financial filings and makes • them publicly available • 10K: Firm’s annual report. Must be filed within • 60 days from end of fiscal year (phased-in) Coca-Cola 10K example • 10Q: Firm’s quarterly report. Must be filed within • 35 days from end of fiscal quarter (phased-in) Abercrombie & Fitch 10Q example

Levels of Conceptual Framework • Basic Objectives • Fundamental Concepts • Recognition and Measurement Concepts

Basic Objectives of Financial Reporting • To provide information useful to investment and credit • decisions • To provide information helpful in assessing the amounts, • timing, and uncertainty of future cash flows • To provide information about economic resources, the • claims to these resources, and changes in them

Primary Qualitative Characteristics • Relevance: Capable of making an impact in a decision. • Reliability: Verifiable, free of bias or error. Secondary Qualitative Characteristics • Comparability: Measured and reported similarly across • firms so that comparisons can be made across firms. • Consistency: Applying the same accounting method • through time so that comparisons can be made over • time within the same firm.

Basic Assumptions Underlying Accounting • Economic Entity: economic activity can be identified to a unit • (firm). • Going Concern: the business enterprise will have an indefinite • life • Monetary Unit: there is a common monetary unit upon which • to value activity • Periodicity: economic activities can be divided into artificial • time periods (quarters, years, etc.)

Basic Principles of Accounting • Historical Cost: assets and liabilities recorded at historical cost • (for reliability) • Revenue Recognition: revenue should be recognized when • realized and earned (as opposed to when cash or goods • actually exchange) • Matching: revenues should be matched to expenses that help • generate them • Full disclosure: firms should provide all information that is • materially important to statement users

Constraints on Accounting • Cost-benefit analysis: benefits from collecting and reporting • information should outweigh the costs • Materiality: only need to be concerned with economic events • that are significant enough to matter • Conservatism: report so that you are least likely to overstate • assets and income

Who Uses Financial Statements? • Investors: Mutual fund companies, larger companies, • individual investors • Creditors: Banks have accounting covenants that can • trigger loan default • Firms, themselves: Most high-level managers are • compensated based on some mix of stock and • accounting performance