Download

1 / 45

460 likes | 573 Views

Fall in the Value of a Tangible Asset i.e. Depreciation has been discussed. The reasons of such fall, Objectives of recording depreciation in Accounting have been explained. We have also considered the different methods of charging depreciation. Some useful concepts like Change in method of depreciation, Asset’s life or estimated useful life are discussed.

E N D

Takshila LearningLearn anything anywherewww.takshilalearning.comCall: +91-8800999280

DEPRECIATION ACCOUNTING (AS-6)

Concept decrease in the value or the expired portion of the cost of fixed asset is called as “Depreciation”. a process of allocating the cost of a fixed asset over its estimated useful life in a rational and systematic manner. AICPA- “a system of accounting which aims to distribute the cost or other basic value of tangible capital assets less salvage (if any) over the estimated useful life of the unit (which may be a group of assets) in a systematic and rational manner. It is a process of allocation and not of valuation

Depreciable Assets expected to be used during more than one accounting Depreciable period have a limited useful life held by an enterprise for Assets’ use in the production or supply of goods and services for rental to others or for administrative purposes and not for the purpose of sale in the ordinary course of business.

Causes Wear & TearTime effluxion (Passage of time) Obsolescence (Technological changes) Depletion (Natural resources)

Objectives Calculating Net Profit/Loss Correct financial position Funds for Replacement correct cost of production Tax benefit Legal requirements. ( Companies & Income Tax Act)

Notes of Depreciation Depreciation: a Non-Cash expense a charge against profit Depreciation : a Source of Fund for replacing the asset Depreciation is calculated using the Cost of the fixed asset (Market Value is ignored)

Interchangeable terms of Depreciation “Depreciation” is for Fixed Asset “Amortization” is for Intangible & Fictitious assets “Depletion” is for Natural Resources or Wasting Assets.

Factors to calculate Depreciation Cost of asset including Capital expenses for installation, commissioning, trial run etc. Estimated useful life of the asset Estimated scrap value (if any) at the end of useful life of the asset [Also called as Salvage Value, Residual Value, Terminal Value] Note : The Cost of the asset Less Estimated Scrap Value is called as “Depreciable Value” which is to be written off during the useful life

Methods of charging Depreciation Straight Line Method Written Down Value method Annuity MethodSinking Fund Method Sum of year’s digits methodMachine hour method Production units method

Straight Line Method Also called as ““Fixed Instalment”, “Original Cost” Method The depreciable value is written off over the useful life & reduced to Nil. An equal amount is charged as depreciation in P&L A/c. Assumption : The usage/utility of the asset is equal in every accounting period.

Straight Line Method Depreciation Amount = Cost – Scrap Value Useful Life Depreciation rate = Depreciation Amount * 100 Cost of Asset Applicable for assets that have insignificant repairs & maintenances.

Written Down Value Method Also called as “Reducing Balance”, “Diminishing Balance” or “Fluctuating Instalment” method Annual depreciation decreases every year The asset Reduced value never touches Zero Depreciation rate =

Written Down Value Method Depreciation is high, when repairs are negligible. As repair increases, Depreciation gets lesser. Income Tax Act mandates WDV method Part C of Schedule II (Companies Act, 13) specifies depreciation rates (SLM/WDV) Schedule XIV (Companies Act,1956) First Year-Depreciation same (under SLM/WDV) Subsequent years- Lesser Depreciation as per WDV

Sum of year’s digits method Variation of the “Reducing Balance Method” Depreciable Value (Original Cost Less Scrap Value) multiplied by The number of years (including present year) of remaining life of the asset Total of all digits of the life of the asset (in years)

Annuity Method This method includes the factor of interest on capital employed Asset A/c – Dr. To Interest A/c Depreciation is charged on the asset’s original cost + the interest(opportunity cost) Depreciation is constant over the years (calculated using the annuity table) Note : Depreciation – Debited to P&L A/c, Interest – Credited to P&L A/c Generally used for long term leases which involves capital outflow.

Sinking Fund Method For replacing the fixed asset at the end of its life, just accumulating the depreciation is not enough This annual depreciation (calculated using Sinking Fund table) is transferred to a sinking fund account & a same amount investment is done (government securities) Every subsequent year the annual depreciation & the interest earned is reinvested the Investment. Last year of the old asset’s life, the securities are sold for replacing the asset

Sinking Fund Method(Depreciation Reserve Fund) The book value of the old asset, at the time, is transferred to the Sinking Fund Account. Amount realised on sale of the old asset, as well as the profit or loss on sale of securities is transferred to the Sinking Fund Account Surplus of Sinking Fund A/c to General Reserve Deficit to P&L A/c

Journal Entries – Sinking Fund Depreciation A/c Dr. Bank A/c Dr To Sinking Fund A/c To Sinking Fund Investment A/c Profit and Loss Account Dr. Sinking Fund Investment A/c Dr. To Depreciation A/c To Sinking Fund A/c (Reverse if loss) Sinking Fund Investment A/c Dr. Sinking Fund A/c Dr To Bank A/c To Asset A/c Bank A/c Dr. Sinking Fund A/c Dr. To Interest on Sinking Fund Investment A/c To General Reserve A/c Interest on Sinking Fund Investment A/c Dr. P&L A/c Dr. To Sinking Fund A/c To Sinking Fund Account Note : Similarly “Insurance Policy method” is used, where annual depreciation is deposited as annual premium, on maturity the assured sum is used for replacement of asset.

Production Units Method Used by the Manufacturing industries Depreciation depends mainly on the actual units/ output produced in a particular year. Depreciation: (Original Cost – Scrap Value) * Units produced in the year Total Estimated output (Entire Life)

Machine Hour Method Used by the Manufacturing industries Depreciation depends mainly on the actual machine hours used in a particular year. Depreciation: (Original Cost – Scrap Value) * Machine hours run in the year Total Machine hours(Entire Life)

Depletion method Used for mines, quarries etc The depreciation rate is calculated by dividing the cost of the asset by the estimated quantity of product likely to be available. Annual depreciation will be the quantity extracted multiplied by the rate per unit.

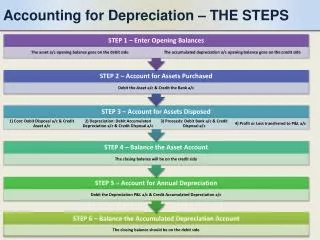

Methods-Recording of Depreciation Asset A/cProvision for Depreciation A/c Also called as “ Accumulated Depreciation A/c” Depreciation is charged from the Asset A/c itself Depreciation A/c – Dr. To Asset A/c Depreciation is accumulated in a separate A/c Depreciation A/c - Dr. To Provision for Depreciation A/c

Asset Method Only Asset A/c is prepared The Purchase of Asset, Depreciation charged, Sale of asset, its profit/loss & its closing balance (Book value/WDV) are shown in the Asset A/c. In the Balance Sheet, the asset is shown at the Net Book Value (Gross Value – Depreciation)

Accumulated Depreciation The Asset A/c & “Provision for depreciation A/c” are separately maintained In the Asset A/c, the Purchase, Sale & its Profit/loss are recorded ( the account shows the Original cost of the asset) The depreciation is accumulated in the separate “Accumulated Depreciation” A/c When the asset is sold, corresponding accumulated depreciation on it, is to be closed. Accumulated Depreciation A/c- Dr. To Asset A/c

Asset Disposal A/c Asset Disposal A/c can be prepared for the asset which is being disposed Asset’s sale, its profit/loss are recorded The opening balance of the asset (in the year of sale) is transferred to “Asset Disposal A/c” This A/c can be prepared with either of the method used for depreciation

Profit/Loss on asset Profit or loss on sale of assets = Sale price of asset - Book value/WDV of the asset on the date of sale Book value of the asset on the date of sale = Original cost of the asset – Total depreciation on the asset till that date The profit/loss is transferred to P&L A/c If asset is sold over Cost (Sales – Original Cost) – “Capital Reserve” Profit till Cost : P&L A/c

Illustration A firm purchased on 1st January, 2015 certain machinery for ` 58,200 and spent ` 1,800 on its erection. On July 1, 2015 another machinery for ` 20,000 was acquired. On 1st July, 2016 the machinery purchased on 1st January, 2015 having become obsolete was auctioned for ` 38,600 and on the same date fresh machinery was purchased at a cost of ` 40,000. Depreciation was provided for annually on 31st December at the rate of 10 per cent p.a. on written down value. Prepare the necessary accounts.

Change in method of depreciation As per Consistency concept , the Accounting policy should be consistently applied. Change is allowed when: • Required by the Statute • Required by Accounting Standard • Change result in better true & fair view of financial statements • Change in the depreciation method of the asset is applied retrospectively.

Change in method of depreciation Depreciation is to be compared under both the methods from the Date of purchase If the depreciation under old method is > Depreciation under new method, then excess (surplus) depreciation is taken back (Credited in P&L A/c) If the depreciation under old method is < Depreciation under new method, then short (deficit) depreciation is charged(Debited in P&L A/c) Prospectively (from date of change), the new method is applied (to be applied on revised WDV- if new method is WDV)

Illustration A firm purchased on 1st January, 2014 certain machinery for ` 52,380 and spent ` 1,620 on its erection. On January 1, 2014 another machinery for ` 19,000 was acquired. On 1st July, 2015 the machinery purchased on 1st January, 2014 having become obsolete was auctioned for ` 28,600 and on the same date fresh machinery was purchased at a cost of ` 40,000. Depreciation was provided annually on 31st December at the rate of 10 per cent on written down value. In 2016, however, the firm changed this method of providing depreciation and adopted the method of providing 5 per cent per annum depreciation on the original cost of the machinery with retrospective effect.

Change in Useful Life a periodical review of useful life should be done In case of revision, WDV should be depreciated over remaining life (as per the revision)

Revaluation of asset As per AS-6, upward/downward revaluation of asset may be done. (on the reduced balance) Depreciation is charged on the revalued asset over the remaining estimated useful life

Treatment of Revaluation In case Asset revalued upward, the revaluation profit credited to “Revaluation Reserve A/c” Asset A/c – Dr. To Revaluation Reserve A/c When subsequently revalued downward, Revaluation loss debited/charged from “Revaluation Reserve” (to the extent available), otherwise from P&L A/c Revaluation Reserve A/c – Dr P&L A/c - Dr. To Asset A/c For downward revaluation for the first time, Revaluation loss charged to P&L A/c P&L A/c – Dr. To Asset A/c

Provision for repairs & renewals An estimated expenditure is debited to Profit and Loss Account and credited to Provision for Repairs and Renewals Account P&L A/c – Dr. To Prov. For Repairs A/c The actual expenses are taken from the Provision A/c Prov. for repairs A/c – Dr. To Repairs A/c Balance in Provision A/c is transferred to Asset A/c

MCQs Q.1. Original cost of a machine = Rs. 1,30,000, Salvage value = Rs. 4,000, Useful life = 6 years, Depreciation for the 1st year under sum of year's digit method will be :

MCQs Q.2. What would be treatment when plant and machinery is sold for Rs. 1,40,000 whose cost is Rs. 1,00,000 and WDV is Rs. 40,000

MCQs Q.3. A new machine costing ` 1 lakh was purchased by a company to manufacture a special product. Its useful life is estimated to be 5 years and scrap value at ` 10,000. The production plan for the next 5 years using the above machine is as follows: Year 1 5,000 units Year 2 10,000 units Year 3 12,000 units Year 4 20,000 units Year 5 25,000 units The depreciation expenditure for the 3rd year will be

MCQs Q.4. Method of depreciation - SLM; Rate of depreciation-20% Year ending on 31st March every year. 1-04-04 Purchased second hand machinery for Rs.80,000 1-04-04 Spent Rs.20,000 on its repairs Find out the profit or loss on sale of machinery if machinery is sold on 30-09-2006 for Rs.45,000

MCQs Q.5. If depreciation is charged on an asset by Straight line and Reducing balance methods, what will be the respective amount of depreciation in subsequent years?

MCQs Q.6. Which method of charging considers that the business besides losing the original cost of the asset also loses interest on the amount used for buying the asset?

MCQs Q.7. For charging depreciation, on which of the following assets, the depletion method is adopted?

MCQs Q.8. The portion of the acquisition cost of the asset, yet to be allocated is known as

MCQs Q.9. Which of the following expenses is notincluded in the acquisition cost of a plant and equipment?

MCQs Q.10. In the case of downward revaluation of an asset which is for first time revalued, the account to be debited is