Download

1 / 15

150 likes | 261 Views

Global role of mobile companies in the world. Infobalt 2002 Darius Masionis , Chief Executive Officer UAB Bite GSM. About Bit ė GSM Slowdown on the global market European telecommunication sector development What can we expect in the future of telecoms? Conclusions. Outline.

E N D

Global role of mobile companies in the world Infobalt 2002 Darius Masionis, Chief Executive Officer UAB Bite GSM

About Bitė GSM Slowdown on the global market European telecommunication sector development What can we expect in the future of telecoms? Conclusions Outline

Bitė GSMin brief • Bite GSM was established in 1995 • Full scale provider of mobile and internet services • GSM 900 and 1800 mobile network • Data and Internet license • Roaming with 155 operators in 74 countries • 427 employees • TDC is 100% shareholder

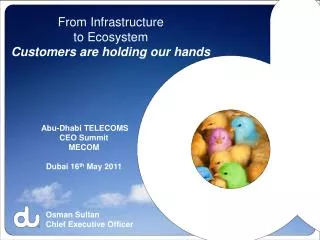

100% 100% 78.7% 100% 100% 100% 100% TDC Tele Danmark TDC Mobile International TDCSwitzerland TDC Internet TDCDirectories TDC Cable TV TDCServices Bite is 100% owned by TDC Mobile International, the member of TDC group TDC group consists of 20 companies, operating in 12 Europe countries In first half of 2001 Bitė GSM has been listed by independent international experts as one of the most effectively operating companies in TDC group

TDC Mobile International • Talkline (100%) • TDC Mobil (100%) • Bité • (100%) • Polkomtel (19.6%) • UMC • (16.3%) • Connect Austria (15.0%)

A capital markets’ perspective on the recent evolution Early 2000 Number of customers Increased penetration Third generation, m.data Optimistic growth prognosis Long term growth, UMTS Hype over new economy Consolidation Early 2002 Increase ARPU, reduce customer acquisition costs Penetration peak Mobile data disappointment Heavy debts, growth slowdown Cash, short term return Back to balance sheet approach Consolidation

Data as the ARPU driverEstimations seen in 2000 and 2002 90 80 70 60 50 40 30 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 Nokia 2002perspective CreditSuisse

60% 50% Mobile 40% Data 30% Telecom Revenues 20% GDP 10% 0% Fixed -10% 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 Slowdown ahead in the absence ofa new killer application Annual revenue and GDP growth for telecoms operating in EU15 Source: WEFA-WMM; Dataquest; ITU

In wireless:concentration around six large groups European market share (subscribers), percent 1997-2000 • Aggregate share of six largest operators is over 70% of European Market • Vodafone • Telecom Italia • British Telecom • France Telecom/ Orange • Deutsche Telecom • Telefonica, Spain Source EMC Database; Company websites; Eurotel Analysis

Horizon 3 • Horizon 2 • Horizon 1 In wireline:incumbents will face challenges along three horizons + • Magnitude of opportunities • Technologyinnovation • Broadband content/ services • Broadbandaccess • Level of uncertainty - + • Infrastructure competition • SME battle • Price decline • Wireless substitution • Attacker consolidation • New attackers (new business models) • Technology substitution • Magnitude of threats + • Regulatory issues(e.g., rebalancing, separation of network) Potential real threat • Challenges identified, but still unclear dimensions • Incumbents have to set-up enhanced capabilities to face challenges • Challenges/opportunities unclear • Challenges clearly identified • Incumbents have a chance to achieve positive outcome through excellent execution • Characteristics

Search of growth opportunities Development within current businesses • Continues to be top priority • Current markets • New markets Expansion within the value chain • + • + • Option to explore • Content provider • Content owner/ developer • Device design, offering and installation • Service outsourcing for clients • Redeploying intangibles into adjacent industries Deployment of intangibles into other industries • + • +

European landscape today • Small • Integrated • Large Integrated • Focused • Wireline • Data • Wireless The landscape of the European Telecom Industry will evolve towards larger and more focused players via restructuring at BU level rather than at group level • Future European landscape • Small • Integrated • Large Integrated • Focused • Incumbents maintain local positions • Possibly some turnaround plays • Wireline • Some small players will shred data assets • Some large players will grow internationally • Increased focus • Data • Some small players will shred wireless assets • Possible moves to complete/develop pan-European coverage and regional plays • Increased focus • Wireless

Integrated players should opt to become multifocused operators with a value-added corporate role Operationally integrated company • Operational • Current situation for many Telco's, leading to significant discounts in many cases • Strategic • Group configuration • Development of synergies and shared skills • Management of critical resources • For telecom players that will remain integrated, this is the configuration to adopt • Integrated multi-focused player with value adding corporate • center • Role of corporate center Financial holding • Not suited for value adding, integrated model • Financial • Unrelated, autonomous businesses • Same business systems and dynamics • Degree of Business Unit Integration

Consequences and implications Balance sheet restructuring and focus on earnings • Balance sheet restructuring is a first priority for players with high debt levels • Performance improvement needed to address the turnaround play • Responding to changed priorities from the capital markets perspective: from growth to ROI, EBITDA. Cash is king: efforts to reduce Capex and Opex Focus or multi-focus strategy in the context of sector restructuring • Corporate strategy: decide on core areas to strengthen, businesses on which control will be maintained, revise value of options developed • Have an M&A roadmap in place to strengthen core-areas and, potentially, to divest non-core areas • Organizational model for the corporation and role of the corporate center Search of growth opportunities • Cope with the growth challenge; organic, inorganic, business building • Explore activities to grow new business and leverage skills and intangibles • Develop and cultivate networks of partners. Critical for new businesses