Download

1 / 4

40 likes | 133 Views

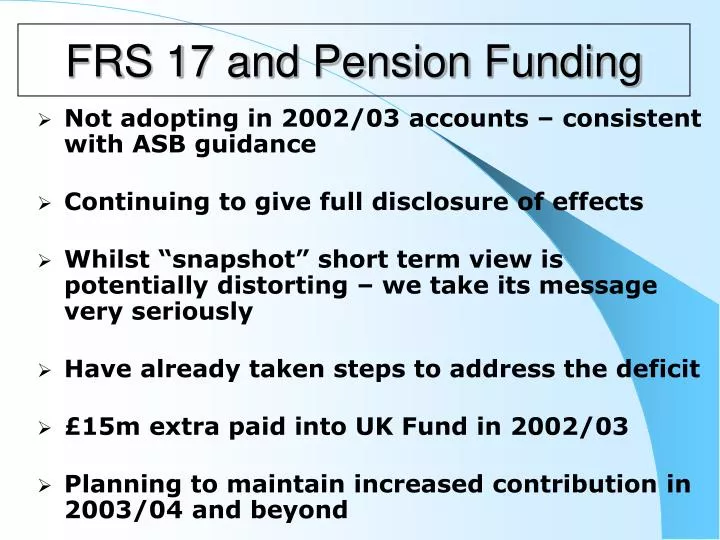

FRS 17 and Pension Funding. Not adopting in 2002/03 accounts – consistent with ASB guidance Continuing to give full disclosure of effects Whilst “snapshot” short term view is potentially distorting – we take its message very seriously Have already taken steps to address the deficit

E N D

FRS 17 and Pension Funding • Not adopting in 2002/03 accounts – consistent with ASB guidance • Continuing to give full disclosure of effects • Whilst “snapshot” short term view is potentially distorting – we take its message very seriously • Have already taken steps to address the deficit • £15m extra paid into UK Fund in 2002/03 • Planning to maintain increased contribution in 2003/04 and beyond

FRS 17 Excludes assets and liabilities relating to corporate disposals

Pensions Impact on Profit and Loss Account SSAP 24 gives a greater charge to the Profit and Loss than FRS 17 The reduction in the charges year on year is a function of the scheme being closed to new members as of 1st January 2002