Download

1 / 3

30 likes | 38 Views

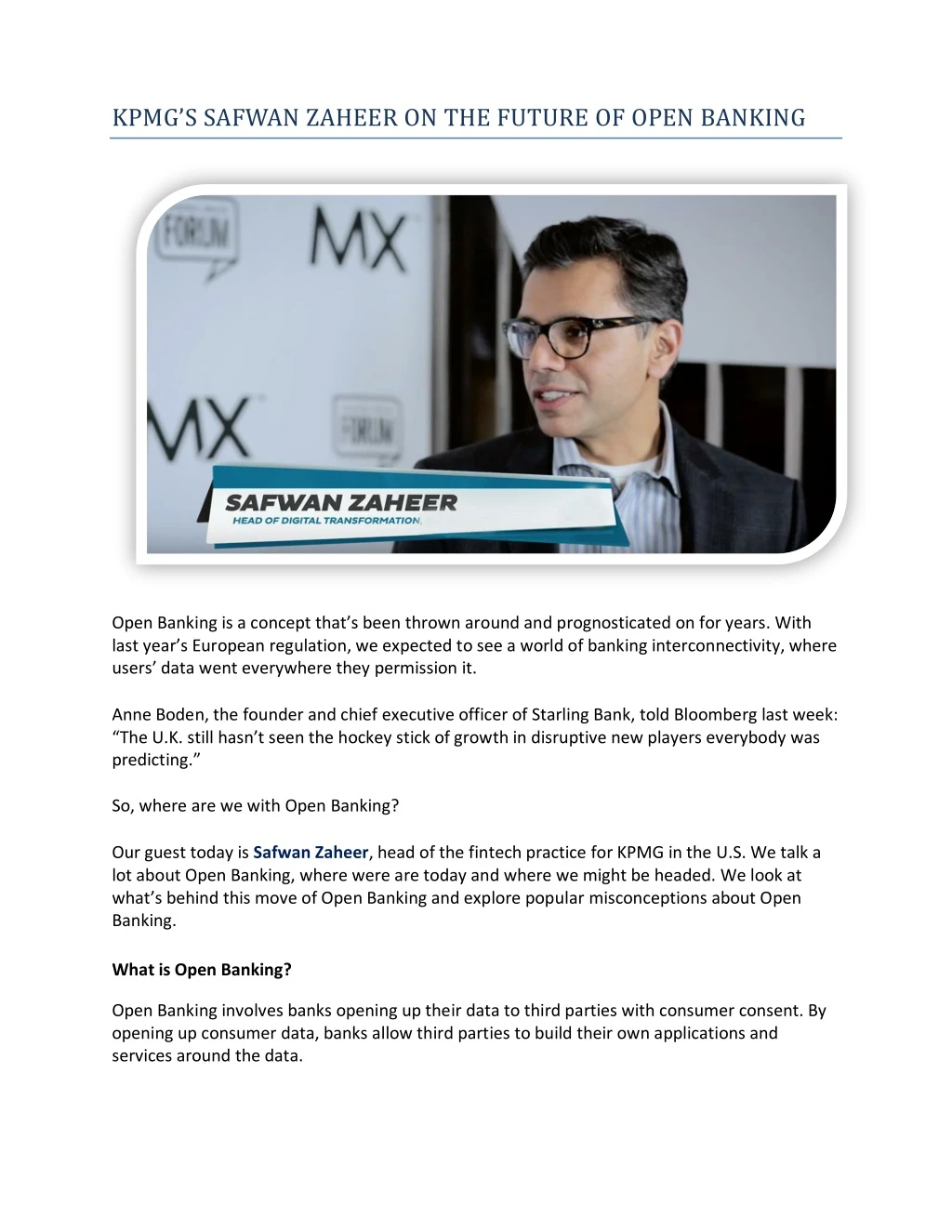

Safwan Zaheer is an accomplished Digital Financial Services executive with track-record of launching Digital Banking businesses, shaping business strategies and executing digital banking and FinTech products in market; including spearheading Digital Transformation programs. Most of these initiatives have been drivers for expanded market footprints and growth for his clients and former employers. His career span includes working for Technology and Financial Services firms with experience in global markets, specifically in South East Asia and Europe.

E N D

KPMG’S SAFWAN ZAHEER ON THE FUTURE OF OPEN BANKING Open Banking is a concept that’s been thrown around and prognosticated on for years. With last year’s European regulation, we expected to see a world of banking interconnectivity, where users’ data went everywhere they permission it. Anne Boden, the founder and chief executive officer of Starling Bank, told Bloomberg last week: “The U.K. still hasn’t seen the hockey stick of growth in disruptive new players everybody was predicting.” So, where are we with Open Banking? Our guest today is Safwan Zaheer, head of the fintech practice for KPMG in the U.S. We talk a lot about Open Banking, where were are today and where we might be headed. We look at what’s behind this move of Open Banking and explore popular misconceptions about Open Banking. What is Open Banking? Open Banking involves banks opening up their data to third parties with consumer consent. By opening up consumer data, banks allow third parties to build their own applications and services around the data.

Typically, the sharing is done with APIs but they’re not the only way to share data. One misconception in the industry around Open Banking is that banks would share consumer data without proper monitoring and permissions. That’s not the case — sharing with the proper monitoring and permissioning is one of the key aspects of Open Banking. Where is the move toward Open Banking coming from? In the EU and the UK, there’s a mandate driving banks to open up their data to third parties. It started with the PSD2 requirement which asked UK banks to share payment data. There are two forces behind the push toward Open Banking: the first is customers demanding secure, convenient, and faster access to banking information as part of that information being available for use in other services and applications. For example, I’m a user and want to open up an account with a cryptowallet or payments wallet and I want my bank account information to be accessible to this wallet. That can only be done if the customer data is readily shared and available for the products to incorporate. The other driver is that banks are no longer to develop products and services on their own. Co- creation is going the critical in banks to build new products and experiences to be launched in the market. However, in the US, there is no mandate, so some of the protocols and sharing standards have been created by the banks on their own. How far along are we with Open Banking? In the US, we’re pretty far behind but in 2019, I expect banks to be more active in sharing data with third parties. But in general, in the absence of a mandate, banks are just using their own priorities to rank and stack open banking approaches in the market. Net-net, it is a priority-driven initiative versus something they have to do, like in the EU. Citibank, JPMorgan Chase, US Bank and even Wells Fargo have certainly enabled developer portals. They seem to understand the importance of co-creation and third party access to data. For some banks, open APIs and Open Banking might not be among their top priorities and they’ll be trumped by other projects. What are the hurdles to Open Banking? I think there are three key hurdles to Open Banking. First, many banks are sitting on legacy technology and enabling APIs requires a certain level of agility for these platforms. Second, any new project requires funding and this is tied to business priorities. The third reason is around culture and boils down to how motivated leadership is and how quickly they want to press on the co-creation element.

What can banks do to embrace Open Banking? The one thing they can do is getting started. It is about continuously learning, testing, and experimenting. Banks can create a small use case around payments and customer accounts with selected partners. That’s the best approach I’ve come to know and what I evangelize with our clients.