Download

1 / 1

E N D

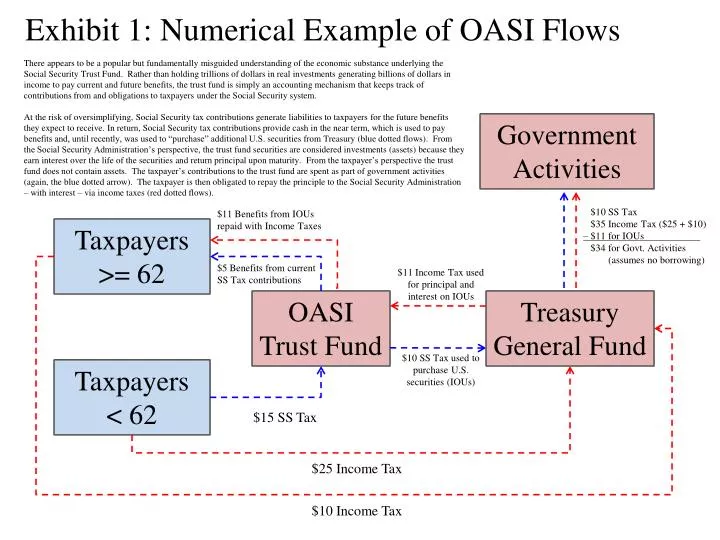

Exhibit 1: Numerical Example of OASI Flows There appears to be a popular but fundamentally misguided understanding of the economic substance underlying the Social Security Trust Fund. Rather than holding trillions of dollars in real investments generating billions of dollars in income to pay current and future benefits, the trust fund is simply an accounting mechanism that keeps track of contributions from and obligations to taxpayers under the Social Security system. At the risk of oversimplifying, Social Security tax contributions generate liabilities to taxpayers for the future benefits they expect to receive. In return, Social Security tax contributions provide cash in the near term, which is used to pay benefits and, until recently, was used to “purchase” additional U.S. securities from Treasury (blue dotted flows). From the Social Security Administration’s perspective, the trust fund securities are considered investments (assets) because they earn interest over the life of the securities and return principal upon maturity. From the taxpayer’s perspective the trust fund does not contain assets. The taxpayer’s contributions to the trust fund are spent as part of government activities (again, the blue dotted arrow). The taxpayer is then obligated to repay the principle to the Social Security Administration – with interest – via income taxes (red dotted flows). Government Activities $10 SS Tax $35 Income Tax ($25 + $10) – $11 for IOUs $34 for Govt. Activities (assumes no borrowing) $11 Benefits from IOUs repaid with Income Taxes Taxpayers >= 62 $5 Benefits from current SS Tax contributions $11 Income Tax used for principal and interest on IOUs OASI Trust Fund Treasury General Fund $10 SS Tax used to purchase U.S. securities (IOUs) Taxpayers < 62 $15 SS Tax $25 Income Tax $10 Income Tax