Download

1 / 7

70 likes | 203 Views

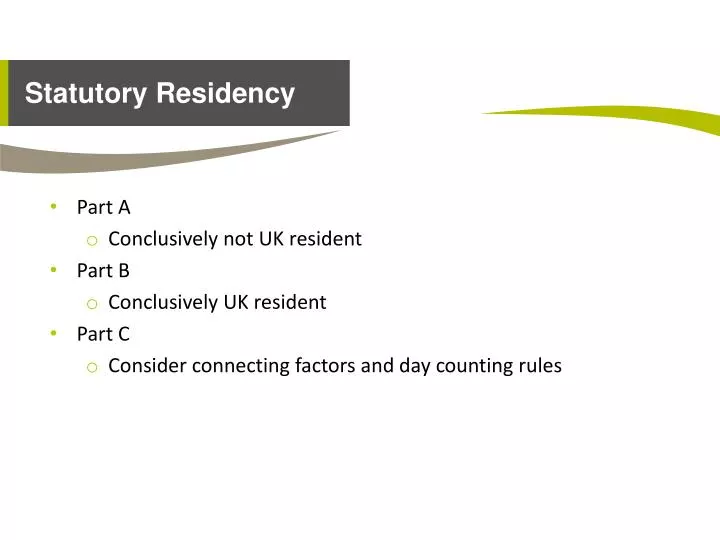

Part A Conclusively not UK resident Part B Conclusively UK resident Part C Consider connecting factors and day counting rules. Statutory Residency. Not resident in the UK in any of the previous three tax years and are present in the UK for fewer than 45 days in the current tax year; OR

E N D

Part A Conclusively not UK resident Part B Conclusively UK resident Part C Consider connecting factors and day counting rules Statutory Residency

Not resident in the UK in any of the previous three tax years and are present in the UK for fewer than 45 days in the current tax year; OR Resident in the UK in one or more of the previous three tax years and are present in the UK for fewer than 10 days in the current tax year; OR Leaves the UK to carry out full time work abroad, provided they are present in the UK for fewer than 90 days in the tax year and no more than 20 days are spent working in the UK during the tax year; Part A – Conclusively not resident

Present in the UK for 183 days or more in a tax year OR Only have one home and that home is in the UK or have 2 or more homes and these are all in the UK OR Carry out full time work in the UK Part B – Conclusively resident

Applies when neither part A or part B apply Consider ‘Connecting Factors’ Different rules for ‘leavers’ and ‘arrivers’ Part C

Individuals resident in 1 or more of the 3 previous tax years Relevant connecting factors: Family UK resident Substantive UK employment Available accommodation in UK Spent 90 days or more in the UK in either of the previous 2 tax years Spends more days in the UK than any other single country Leavers

Individuals not resident in all of the 3 previous tax years Relevant connecting factors: Family UK resident Substantive UK employment Available accommodation in UK Spent 90 days or more in the UK in either of the previous 2 tax years Arrivers

Current basis considered no longer sufficient IR20 / HMRC6 / case law Conclusive rules to remove uncertainty Most UK expats will be non resident under Part A “Leaves the UK to carry out full time work abroad, provided they are present in the UK for fewer than 90 days in the tax year and no more than 20 days are spent working in the UK in the tax year” Connecting Factors then of no relevance Should be considered as a good thing not an attempt to collect more tax Summary