Download

1 / 18

270 likes | 664 Views

Swap Contracts, Convertible Securities, and Other Embedded Derivatives. Innovative Financial Instruments. Dr. A. DeMaskey. Chapter 25. OTC Interest Rate Agreements. Forward-Based Interest Rate Contracts Forward Rate Agreements Interest Rate Swaps Option-Based Interest Rate Contracts

E N D

Swap Contracts, Convertible Securities, and Other Embedded Derivatives Innovative Financial Instruments Dr. A. DeMaskey Chapter 25

OTC Interest Rate Agreements • Forward-Based Interest Rate Contracts • Forward Rate Agreements • Interest Rate Swaps • Option-Based Interest Rate Contracts • Caps and Floors • Collar • Swap Options

Forward-Based Interest Rate Contracts • Forward Rate Agreement (FRA) • two parties agree today to a future exchange of cash flows based on two different interest rates • one of the cash flows is tied to a fixed rate • the other is determined at a later date (floating rate) • LIBOR is frequently used as the floating rate index • Single settlement date

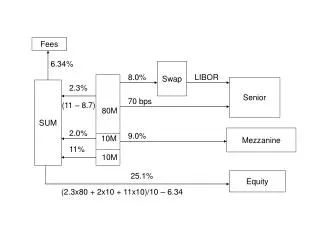

Forward-Based Interest Rate Contracts • Interest Rate Swaps • multiple exposure dates could be hedged using a series of FRAs • swap contract is a prepackaged series of forward contracts to buy or sell LIBOR at the same fixed rate • priced off the LIBOR forward yield curve, but quoted off the Treasury bond yield curve • fixed rate side is • the yield of a Treasury bond with a comparable maturity, and • a risk premium term known as the swap spread

Forward-Based Interest Rate Contracts • Interest Rate Swaps • fixed and floating rate payments Where fixed rate is typically the current yield on the U.S. Treasury note (T-note yield + x bps). Where floating rate used is typically the London Interbank Borrowing Rate (LIBOR + x bps).

Swap Example • Consider a 3-year swap in which every 6 months: • Firm B pays Firm A a 5% annual fixed rate • Firm A pays Firm B the prevailing 6-month LIBOR • Notional amount is $100,000,000

Solution Swap is entered into at time 0.

How Are Swaps Used? • To transform a liability • convert floating-rate loan to fixed-rate loan (or vice versa) • To transform an asset • convert fixed rate paying asset to one paying floating rate (or vice versa)

Transforming a Liability • A firm has 3 years left on its $100 million loan at LIBOR + 0.80 • The firm wants to convert this floating rate loan to a fixed rate loan • To accomplish this, the firm enters into the following swap: • It pays 5% fixed and receives LIBOR • Net cost = LIBOR + 0.80 + 5.0 - LIBOR = 5.8%

Transforming an Asset • Suppose a firm owns a portfolio of bonds that pays a fixed rate of 4.70% • The firm whishes to convert this to a floating rate • So, it enters into the following swap: • Pays 5% fixed and receives LIBOR • Net return = 4.70 - 5.00 + LIBOR = LIBOR - 0.30

Option-Based Interest Rate Contracts • Cap agreement • a series of cash settlement interest rate options, typically based on LIBOR • Floor agreement • makes settlement payments only when LIBOR is below the floor rate

Option-Based Interest Rate Contracts • Collars • combination of a cap and a floor • long in one and short in the other • cap-floor-swap parity occurs when the combination are at the same rates and have a net zero initial cost • can be viewed as a pair of option positions

Option-Based Interest Rate Contracts • Swap Options (“Swaptions”) • the right but not obligation to enter into an interest rate swap having a predetermined fixed rate at some later date • Types: • Receiver swaption • Payer swaption

Swap Contracting Extensions • Currency swaps • denominated in different currencies • Equity index-linked swaps • based on a variable debt rate and an equity index • Commodity swaps • fixes the price of a commodity over a certain period • hedge exposures to commodity prices

Warrants and Convertible Securities • Warrants • equity option issued by the company whose stock serves as the underlying asset • if exercised, the company will create new shares of stock to give to the warrant holder

Warrants and Convertible Securities • Convertible securities • owner has right but not obligation to convert the existing investment into another • Convertible preferred stock • convertible into common stock • conversion value • Convertible bonds • viewed as a regular bond plus an option to exchange the bond for a number of shares of common stock

Other Embedded Derivatives • Structured notes • Dual currency bonds • Equity index-linked notes • Commodity-linked bull and bear bonds • Swap-linked notes

www.altivest.com www.calamos.com www.goldmasachs.com/qa/ www.dir.co.jp/InfoManage/datarsc.html www.optionscentral.com www.optionsanalysis.com www.netservers.com/~waldemar/wl.html The InternetInvestments Online