Download

1 / 44

440 likes | 559 Views

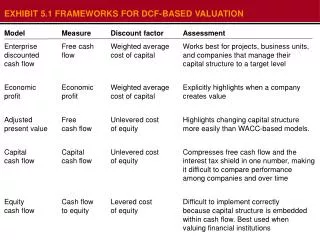

Frameworks for Valuation. Chapter 8 Summary Paula Heathcoat April 9, 2003. Valuing a company using the discounted cash flow approach. 4 models Enterprise DCF model Economic Profit Model Adjusted Present Value (APV) Model Equity DCF Model All models provide the same results

E N D

Frameworks for Valuation Chapter 8 Summary Paula Heathcoat April 9, 2003

Valuing a company using the discounted cash flow approach • 4 models • Enterprise DCF model • Economic Profit Model • Adjusted Present Value (APV) Model • Equity DCF Model • All models provide the same results (demonstrated later in this presentation)

140 130 100100 90 70 Debt Value = 50 43 33 26 20 Equity Value + 90 87 67 64 50 Enterprise Discounted Cash Flow Model • Formula: Single-Business Company • Equity Value = Operating Value - Debt Value

140 130 100100 90 70 Debt Value = 50 43 33 26 20 Equity Value + 90 87 67 64 50

Enterprise Discounted Cash Flow Model • Formula: Multi-business Company • Equity value = Sum of the values of the individual operating units + Marketable securities - Corporate overhead - Value of company debt and preferred stock

Enterprise Discounted Cash Flow Model • Reasons for recommending the enterprise DCF model: • The model values the components of the business (each operating unit) that add up to the enterprise value • The approach helps to identify key leverage areas • It can be applied consistently to the company as a whole or to individual business units • It is sophisticated enough to deal with the complexity of most situations, yet easy to carry out with personal computer tools

Enterprise Discounted Cash Flow Model • Value of operations • Equals the discounted value of expected future free cash flow • Free cash flow= after tax operating earnings + non-cash charges - investments in operating working capital, property, plant, and equipment, and other assets • Free cash flow = sum of the cash flows paid to or received from all the capital providers

Enterprise Discounted Cash Flow Model • Value of operations • The discount rate applied to the free cash flow should reflect the opportunity cost to all the capital providers weighted by their relative contribution to the company’s total capital, or WACC • opportunity cost is the rate of return the investors could expect to earn on other investments of equivalent risk

Enterprise Discounted Cash Flow Model • Value of operations • Indefinite life of a business • Separate the value of the business into two periods • during a precise forecast period • after a precise forecast period • Value = present value of cash flow during precise forecast period + present value of cash flow after precise forecast period • The value after the precise forecast period is the continuing value Continuing value = NOPLAT (1-g/ROICi) WACC-g

Enterprise Discounted Cash Flow Model • Value of debt • Equals the present value of the cash flow to debt holders discounted at a rate that reflects the riskiness of that flow • Value of equity • Equals the value of the operations plus non-operating assets, less the value of its debt and any non-operating liabilities

Enterprise Discounted Cash Flow Model • Drivers of Free Cash Flow and Value • The rate at which the company is growing • Growth Rate = ROIC x Investment rate • Return on invested capital (relative to the cost of capital, or WACC) • ROIC = NOPLAT / Invested capital • If ROIC > WACC , then value is greater • If ROIC = WACC, then value is neutral • If ROIC <WACC, then value is destroyed

Enterprise Discounted Cash Flow Model • Drivers • To increase value, a company must do one or more of the following • Earn a higher return on invested capital on legacy assets • Ensure that ROIC(new) exceeds WACC • Increase the growth rate (keeping ROIC above WACC) • Reduce WACC

Economic Profit Model • Useful measure for understanding a company’s performance in any single year • Economic Profit equals the spread between the return on invested capital and the cost of capital times the amount of invested capital • Economic profit = Invested capital x (ROIC - WACC) • Translates the two value drivers (growth and ROIC) into a single dollar figure

Economic Profit Model • Economic Profit is the after-tax operating profits less a charge for the capital used by the company • Economic Profit = NOPLAT - Capital charge = NOPLAT - (invested capital x WACC) • The approach says that the value of a company equals the amount of capital invested plus a premium or discount equal to the present value of its projected economic profit • Value = Invested capital + present value of projected economic profit

Free Cash Flow Valuation Summary Equity Value 9,385 Economic Profit Valuation Summary Equity Value 9,385

Adjusted Present Value (APV) Model • The APV model discounts free cash flows to estimate the value of operations, and ultimately the enterprise value, where the value of debt is then deducted to arrive at an equity value. • This is very similar to the enterprise DCF model, except: • APV model separates the value of operations into two components • The value of operations as if the company were entirely equity-financed • The value of the tax benefit arising from debt financing

Adjusted Present Value (APV) Model • The APV model reflects the findings from the Modigliani-Miller propositions on capital structure • In a world with no taxes, the enterprise value of a company (the sum of debt plus equity) is independent of capital structure (or the amount of debt relative to equity) • The value of a company should not be affected by how you slice it up Remember these guys from Finance 602?

Adjusted Present Value (APV) Model “Mr. Berra, would you like your pizza cut into six or eight pieces?” “Six please, I am not hungry enough to eat eight.” The pizza is the same size no matter how many pieces you cut into it!

Adjusted Present Value (APV) Model • The implications of MM for valuation in a world without taxes are • the WACC must be constant regardless of the company’s capital structure • Capital structure can only affect value through taxes and other market imperfections and distortions

Adjusted Present Value (APV) Model • The APV model • 1) values a company at the cost of capital as if the company had no debt in its capital structure (the unlevered cost of equity) • 2) adds the impact of taxes from leverage.

APV Free Cash Flow Valuation Summary with Tax Impact APV value of FCF 9,390 Value of debt tax shield 642 Non-operating assets 450 Total enterprise value 10,482 Less: value of debt 1,282 Equity Value9,200

APV Free Cash Flow Valuation Summary Equity Value9,200 Free Cash Flow Valuation Summary Equity Value 9,385 Why is there a difference in the equity values?

Adjusted Present Value (APV) Model • Comparison… • In the enterprise DCF model, this tax benefit is taken into consideration in the calculations of the WACC by adjusting the cost of debt by its tax benefit • In the APV model, the tax benefit from the company’s interest payments is estimated by discounting the projected tax savings • The key to reconciling the two approaches is the calculation of the WACC

Adjusted Present Value (APV) Model • Relating WACC to the unlevered cost of equity assuming that the tax benefit of debt is discounted at the unlevered cost of equity WACC = ku - kb (B/(B+S)) T Where ku = unlevered cost of equity kb = Cost of debt T = Marginal tax rate on interest expenses B = Market value of debt S = Market value of equity

Enterprise DCF Adjusted for Changing Capital Structure The enterprise DCF model assumes that the capital structure and WACC would be constant every period However, the capital structure does change every year A separate capital structure and WACC can be estimated for every year

APV Free Cash Flow Valuation Summary Equity Value9,200 Enterprise DCF Adjusted for Changing Capital Structure Equity Value 9,200

The Equity DCF Model • The equity DCF model discounts the cash flows to the equity owners of the company at the cost of equity

The Equity DCF Model • This model also needs to be adjusted for the changing capital structure. It is necessary to recalculate the cost of equity every period using the following formula • ks = ku + (ku - kb)(B/S) Where ks = levered cost of equity • Once the adjustment is made, the value using the equity DCF approach is the same as the APV approach and the enterprise DCF model with WACC adjusted every period

The Equity DCF Model • Once the adjustment is made, the value using the equity DCF approach is the same as the APV approach and the enterprise DCF model with WACC adjusted every period.

APV Free Cash Flow Valuation Summary Equity Value9,200 Adjusted Enterprise DCF Valuation Summary Equity Value 9,200 Adjusted Equity DCF Valuation Summary Equity Value 9,200

The Equity DCF Model • The equity DCF approach is not as useful as the enterprise model (except for financial institutions) because • Discounting cash flow provides less information about the sources of value creation • It us not as useful for identifying value-creation opportunities • It requires careful adjustments to ensure that changes in projected financing do not incorrectly affect the company’s value • It requires allocating debt and interest expense to each business unit, which creates extra work, yet provides no additional information.

Additional Models and Approaches • Option Valuation Models • Models which adjust for management’s ability to modify decisions as more information is made available. • DCF Approaches • Using real instead of nominal cash flows and discount rates • Discounting pretax cash flow instead of after-tax cash flow • Formula-based DCF approaches

Summary of Models Economic Profit Model Advantage over DCF Model: EP is a useful measure for understanding a company’s performance in any single year, while cash flow is not Enterprise DCF Model Advantage: Values the components Pinpoints key leverage areas Consistent Can handle complex situations Easy to carry out Enterprise DCF Economic Profit Equity DCF Model Advantage: Simple and Straightfoward Disadvantage: Provides less information Requires careful adjustments APV Model Advantage over Enterprise DCF Model: APV is easier to use when the capital structure is changing significantly over the projection period Equity DCF Adjustment Adjustment APV

Frameworks for Valuation Questions?