Download

1 / 0

0 likes | 127 Views

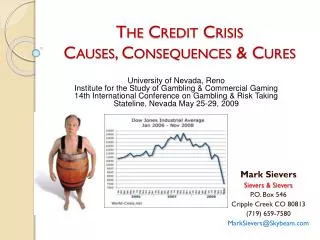

5.4 Credit and Consequences . Credit. Credit is the promise to repay borrowed money (principle) with interest over a certain period of time. Credit cards, mortgages, car loans, student loans, etc. would be examples of credit. Credit is given by a lender to a borrower, also known as a debtor.

E N D