Download

1 / 54

540 likes | 543 Views

Learn about the dangers of cigarette diversion, including the movement of cigarettes from low-tax jurisdictions, the risks of counterfeit cigarettes, and the impact on government revenue and public health.

E N D

Internet Cigarette Diversion Bureau of Alcohol, Tobacco, Firearms & Explosives Chief Counsel’s Conference June 28-30, 2005

What is Diversion? • Diversion generally refers to the movement of a lawful commodity from the stream of regular commerce to the stream of unlawful commerce. • In the case of cigarettes, the term is often used to refer to the movement of cigarettes from no/low tax jurisdictions to high tax jurisdictions. • It can also refer to the clandestine or open movement of counterfeit cigarettes into the stream of regular lawful commerce. • The goal in both instances is the same; to earn profits through the evasion of applicable Federal, State and local excise taxes. • Cigarette diversion is also referred to as Cigarette Trafficking.

Harms of Tobacco Diversion • Cigarette traffickers deprive the Federal government and States of vital revenue used for essential programs such as health care and education • Cigarette diversion is used by organized crime and terrorist organizations to finance their operations • Cigarette traffickers subvert government policies intended to protect the public health and to prevent underage smoking • Cigarette traffickers involved in the distribution of counterfeit cigarettes can pose a substantial health risk to consumers as the cigarettes are often manufactured under unsanitary conditions and may contain additional harmful chemicals • Cigarette traffickers often succeed at the expense of small legitimate business • In the process of cigarette trafficking, those involved can violate numerous Federal and State criminal and civil laws

The Internet & Cigarette Diversion • Over the past several years, the diversion of cigarettes over the Internet has exploded. • A report prepared by the U.S. General Accountability Office in 2003 identified 147 websites involved in tax-free cigarette sales via the Internet. There are likely hundreds, if not thousands, more. • These Internet businesses operate from (1) low tax States, (2) Indian Reservations, and (3) foreign countries. • The success of these businesses is dependent on marketing (1) an exemption from State and/or Federal cigarette excise taxes to the consumer, and (2) the ability to maintain nondisclosure of purchasers’ identities.

Criminal Investigations Federal law enforcement agencies have initiated numerous criminal investigations targeting those involved in cigarette trafficking activities via the Internet and through other means These investigations have resulted in cigarette seizures and forfeitures as well as criminal prosecutions Our most recent investigations have targeted untaxed cigarettes distributed through Internet sites based primarily in Switzerland and Germany There have also been investigations of sales made by Native Americans located on reservations; these investigations often result in seizures and forfeitures

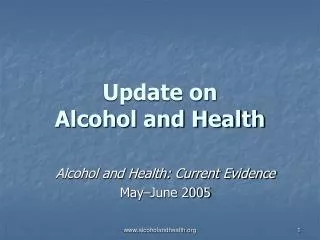

The States • Most States have extensive permit and licensing requirements to regulate the distribution of tobacco products. • Those engaged in Internet cigarette diversion, either through the sale, purchase, or distribution, will often be in violation of State laws • All States impose a tax on tobacco products and 47 States require tax stamps to be placed on packs or containers of cigarettes • Tax Stamps are affixed by a State stamping agent or wholesale distributor in the State • State cigarette tax rates vary from as low as $.03 per pack in Kentucky to $3.00 per pack in New York City

STATE EXCISE TAX RATE ON CIGARETTES 20 Cigarette Pack/ In Cents WA ME Chicago $1.55 .52 $1 1.425 1.19 ND MT VT .44 MN .70 OR NH NY .48 MA 1.51 WI 1.28 ID 1.50 SD RI 2.46 .77 .57 MI .53 CT 1.11 PA WY 2.00 NYC $3 .60 $ 1.35 NJ 2.40 IA NE OH .36 DE .55 NV .64 IL IN .55 .80 WV MD $1 UT VA .98* .555 CO .55 .695 CA .20 DC $1 MO KS .20 KY .79 .03 .87 .17 NC .05 TN .20 AZ NM OK AR SC 1.18 .23 .91 .59 .07 GA AL .12 MS .165 HIGH TAX STATE .18 LA TX .41 .36 LOW TAX STATE AK STATE WITH NO TAX STAMP $1 HI 1.30 As of October 2004

Manner & Means of Internet Cigarette Trafficking Operations • Internet cigarette traffickers profit and succeed through the marketing and sale of untaxed or low-tax cigarettes to consumers who would otherwise pay higher cigarette excise taxes • Many cigarette traffickers also engage in mail and phone order operations • The cigarette traffickers will often advertise in newspapers and other periodicals, over the Internet, and through direct mailings • On their websites and in advertisements, they will offer to purchasers, low-tax or tax-free cigarettes • They will often claim that they do not report the sales to State taxing authorities • They mislead consumers into believing that their operations are completely legal

Manner & Means of Internet Cigarette Trafficking Operations • Because their activities necessitate the movement of their cigarettes from no or low-tax jurisdictions to high tax jurisdictions, the conduct will almost always involve the movement of cigarettes in interstate or foreign commerce • Customers view the websites, communicate with the traffickers, and initiate payments through electronic communications in interstate commerce • In turn, the cigarette traffickers return communications, and process orders and payments, engaging in interstate electronic communications. The traffickers also deliver cigarettes to consumers via U.S. mail or common carriers, also in interstate or foreign commerce • These activities are facilitated primarily through credit card transactions, though some also accept payment via checks and wired funds

Manner & Means of Internet Cigarette Trafficking Operations • Online cigarette traffickers will often expand distribution through the creation of pyramid-type schemes, whereby they offer commissions to other websites and customers that refer sales • Traffickers may also engage in other types of fraud, whereby they defraud the consumer as well as the Federal and State governments • This is most often accomplished through the sale of counterfeit premium brand cigarettes, though may involve other types of fraud as well • Some traffickers may sell to purchasers in volume, allowing the purchasers to resell the untaxed cigarettes in “brick & mortar” stores, street corners, or elsewhere. • The cigarette traffickers often do not report their sales to applicable State taxing authorities as required by Federal law

Manner & Means of Internet Cigarette Trafficking Operations • For foreign-based websites, the cigarette traffickers may make false or misleading customs declarations, or structure cigarette shipments to avoid detection by U.S. authorities • Often, the foreign-based websites distribute untaxed cigarettes that do not bear required U.S. warning labels • They often distribute and import U.S. brand cigarettes without the permission of the trademark holder • They often distribute cigarette brands that have not been approved for sale in the U.S. • In addition to evading applicable State and local excise taxes, these traffickers evade U.S. excise taxes as well

Federal Statutes Implicated by Internet Cigarette Diversion 15 U.S.C. § 376 Jenkins Act 15 U.S.C. § 1333 Cigarette Labeling & Advertising Act 18 U.S.C. § 545 Smuggling 18 U.S.C. § 1341 Mail Fraud 18 U.S.C. § 1343 Wire Fraud 18 U.S.C. § 1956-57 Money Laundering 18 U.S.C. § 1962 R.I.C.O. 18 U.S.C. § 23 14-15 Counterfeit Tax Stamps 18 U.S.C. § 2320 Trafficking in Counterfeit Goods 18 U.S.C. § 2342 Contraband Cigarette Trafficking Act 19 U.S.C. § 1618 Tariff Act 26 U.S.C. chapter 52 Internal Revenue Code

Contraband Cigarette Trafficking Act (CCTA) • 18 U.S.C. §§ 2341-46 • The CCTA makes it unlawful for any person to ship, transport, receive, possess, sell, distribute or purchase contraband cigarettes • Contraband Cigarettes are: • - Cigarettes in a quantity in excess of 60,000 (60,001 cigarettes = 300 cartons = 5 cases + 1 cigarette), and • - That bear no evidence of the payment of State taxes, and • - Are found in a State that requires a stamp, impression, or other indication on the individual packs or other containers of cigarettes to evidence payment of the cigarette tax • - In the possession of person not authorized to possess • 47 States require tax stamps (SC, NC, ND do not)

CCTA • CCTA also imposes a record keeping requirement on any person who ships in excess of 60,000 cigarettes in a single transaction • CCTA provides exceptions for common and contract carriers with proper bills of lading, government agencies, persons licensed by the State in compliance with record keeping requirements, and persons holding licenses or permits issued under the IRC

Why the CCTA is Violated • Some U.S. purchasers acquire in excess of 60,000 cigarettes bearing no State tax stamps from the Internet cigarette traffickers • Often the purchaser is acquiring for the purpose of resale without payment of applicable taxes • Both the trafficker and purchaser are in violation of the CCTA • In some instances involving domestic Internet cigarette traffickers, the trafficker may not be authorized to possess unstamped, untaxed cigarettes in the State in which operations are based, though they routinely maintain an inventory in excess of 60,000 cigarettes

The Jenkins Act • 15 U.S.C. §§ 375-78 • It is unlawful for a person to sell or offer to sell cigarettes to a person not licensed by the state without filing a monthly report of the sale(s) to the State tobacco tax administrator • Any person who sells cigarettes in interstate commerce into a State taxing their sale to other than a licensed distributor must: • A. File with the State tobacco tax administrator their name and place of business • B. By the 10th of each month, provide a report detailing the shipments made into the State during the previous month, including the purchaser, brand, and quantity Note that there is currently legislation before the Senate called the Prevention Against Cigarette Trafficking Act or PACT Act, that would make the Jenkins Act a felony – it would also lower the CCTA threshold to 20,001 cigarettes.

Why the Jenkins Act is Violated • Almost no one engaged in the trafficking of untaxed cigarettes over the Internet is in compliance with the Jenkins Act • Though the traffickers ship untaxed cigarettes in interstate commerce to unauthorized individuals, they do not report these sale as required by the statute • As one of the marketing tools employed by traffickers, they claim on the websites that they will not report sales to reassure customers that they will not receive a tax bill from the State taxing authority

Wire & Mail Fraud • 18 U.S.C. §§ 1341, 1343 • Purpose: To prevent the instrumentalities of interstate commerce be used to facilitate criminal activities. • Unlawful to use U.S. mail, wire, radio or T.V. in interstate commerce for the purpose of executing a scheme to defraud, including schemes to defraud the government of tax revenue. • Scheme need not be successful. Note that mail fraud also applies to interstate common and contract carriers and that the conduct may be entirely intrastate Note that for wire fraud, the conduct must actually be interstate

Why the Wire & Mail Fraud Statutes are Violated • The success of the Internet cigarette trafficking activities is dependent on the ability of the traffickers to provide purchasers with savings on the cigarettes; these savings are created as an incident to the traffickers’ failure to collect applicable State and Federal excise taxes and their refusal to report the sales to State taxing authorities • In furtherance of this necessity, many websites tout their ability to sell cigarettes tax-free • The intent of these traffickers is to profit through the evasion of Federal and State taxes • Those distributing counterfeit cigarettes would also be in violation of these statutes • The traffickers necessarily utilize the instrumentalities of interstate and foreign commerce to facilitate their fraud, including wires and mail facilities

Why the Wire & Mail Fraud Statutes are Violated • The Federal Courts have held that these activities violate the wire/mail fraud statutes: • Fountain v. U.S., 357 F.3d 250 (2d Cir. 2004) • U.S. v. DeFiore, 720 F.2d 757 (2d Cir. 1983) • U.S. v. Melvin, 544 F.2d 767 (5th Cir. 1977) • U.S. v. Brewer, 528 F.2d 492 (4th Cir. 1975) • US v. 1.920,000 cigarettes 2003 WL 21730528 (WDNY 2003) • The Supreme Court has held that International Diversion schemes using wire transmissions violate the Wire Fraud Statute in Pasquantino v. US, __US __ (2005)

Money Laundering • 18 U.S.C. § 1956 • General purpose is to penalize the use of proceeds from one crime to facilitate another crime. • Makes it unlawful to conduct or attempt to conduct a financial transaction which involves the proceeds of a Specified Unlawful Activity, with the intent to: • - promote the carrying on of a SUA, or • - to violate the IRC (26 USC 7201 or 7206), or • - to conceal or disguise the nature, source, or ownership or control of the proceeds of a SUA, or • - to avoid a Federal/State transaction reporting requirement.

Why the Money Laundering Statute May be Violated • Wire/Mail Fraud, CCTA, and the Counterfeit Goods/Stamps provisions are all specified unlawful activities under the money laundering statute • Internet cigarette traffickers utilize the proceeds from their cigarette trafficking activities to acquire more cigarettes and to facilitate their activities through the payment of operational expenses, such as credit card transaction fees and shipping costs • May also engage in other financial transactions with proceeds derived from the cigarette trafficking activities

Racketeering Influenced & Corrupt Organizations Act 18 U.S.C. §§ 1961-1968 RICO was enacted to prevent legitimate companies from being infiltrated by organized crime, but also can apply to organized criminal enterprises that were never legitimate RICO is implicated if there is evidence of: 1. The existence of an enterprise 2. The enterprise affected interstate commerce 3. Defendants were employed by or associated with the enterprise 4. Defendants participated, directly or indirectly, in the conduct of the affairs of the enterprise, and 5. Defendants participated through a pattern of racketeering activity

Why RICO is Violated • CCTA, wire fraud, and mail fraud are defined as types of racketeering activities; if the internet cigarette traffickers violate one of these statutes at least twice within a 10 year period, this is considered to be a pattern of racketeering activity • The websites are often on-going businesses employing a number of people, and fall w/in the definition of an enterprise • The traffickers are associated with the enterprise and are involved, directly or indirectly in the conduct of affairs of the enterprise • The activities will almost always affect interstate commerce • RICO was recently used to convict a New York Stamping Agent in upstate New York who was involved in CCTA violations

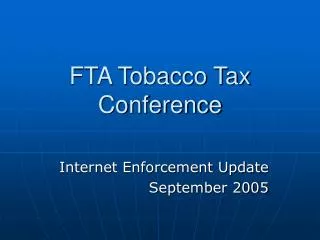

Trafficking in Counterfeit Goods/Stamps • 18 U.S.C. § 2320 • Makes it unlawful for any person to traffic or attempt to traffic in goods or services and knowingly using a counterfeit mark • 18 U.S.C. § 2314 • Unlawful for any person with unlawful or fraudulent intent to transport in interstate or foreign commerce any falsely made or forged State tax stamp, knowing the same to have be counterfeit • 18 U.S.C. § 2315 • Unlawful for any person in interstate or foreign commerce to receive, possess, conceal, store, barter, sell, or dispose of any counterfeit State tax stamp • Unlawful for any person in interstate or foreign commerce to receive, possess, conceal, store, barter, sell, or dispose of any tool, implement, or thing to be used to forge a State tax stamp

Why the Counterfeit Good/Stamps Statutes are Violated • There have been a number of investigations that have identified cigarette traffickers dealing in counterfeit cigarettes • The counterfeited cigarettes are often premium brands, such as Marlboro or Newport, and require the counterfeiters and traffickers to deal in goods bearing counterfeit marks • Sometimes, to create the additional appearance of legitimacy, the cigarette traffickers will also stamp the cigarettes with counterfeit tax stamps; this is done to further mislead the consumer into believing that he/she is purchasing a genuine product • Many times in which the cigarette traffickers offer cartons of cigarettes at very low prices (e.g. under $14-15), the cigarettes are counterfeit • Those involved in counterfeit product evade Federal as well as State excise taxes

Counterfeit Stamps Counterfeit California stamp seized in Vancouver in 2001 Counterfeit New Jersey Stamps seized at the border crossing in Laredo, Texas

Internal Revenue Code, Chapter 52 • The IRC imposes an excise tax on all tobacco products manufactured or imported in the United States • The IRC also imposes permit/licensing requirements on importers and manufacturers • The tax “attaches” upon time of manufacturing or importation • The tax rate on cigarettes is $.39 per pack ($3.90 per carton) • 26 U.S.C. § 5762(c) makes it unlawful for any person to refuse to pay any Federal cigarette excise tax, or to attempt in any manner, to evade or defeat the tax or payment thereof

Why the IRC is Violated • Foreign-based Internet cigarette traffickers distribute cigarettes on which no Federal excise tax is paid • Although the cigarette trafficker is not technically the importer, they conspire with and aid and abet domestic purchasers in evading taxes • The traffickers also structure shipments by placing no more than 2 cartons in any one shipping package, even if the purchaser orders substantially more cigarettes, to avoid detection by U.S. officials and to attempt to come within a misconstrued importation exception • Those traffickers involved in the distribution of counterfeit cigarettes, whether foreign- or domestically-based, do not pay Federal excise taxes and do not report the entry of the cigarettes when imported into the U.S.

Cigarette Labeling and Advertising Act • 15 U.S.C. § 1331 et seq – administered by Federal Trade Commission • The CLAA sets forth the precise wording, capitalization, and punctuation of the warnings required for all packaging and advertising of cigarettes sold, distributed, or advertised in the United States • It requires that Surgeon General warnings rotate quarterly in both advertising and packaging in accordance with a plan submitted to the FTC • Any company wishing to sell or advertise its cigarettes in the U.S. must submit a plan to the FTC explaining how it will comply with the FTC warning label display requirements

Why the CLAA is Violated • Cigarettes sold by Foreign-based Internet cigarette traffickers generally do not contain required U.S. warning labels, and warnings, if present, do not rotate on a quarterly basis • The traffickers generally do not submit a plan to the FTC explaining how they will comply with the CLAA and as such, do not receive approval from the FTC to advertise or distribute cigarettes within the United States

The Tariff Act 19 U.S.C. §§ 1681a, 1681b Provides that cigarettes may only be imported into the U.S. if - the original manufacturer has submitted a list of ingredients added to the tobacco to the Secretary of Health & Human Services - the packaging complies with the Cigarette Labeling and Advertising Act - if the cigarettes bear a U.S. Trademark registered for cigarettes, the trademark owner has consented to the importation of the cigarettes - requires importers to submit and make a number of certifications stating compliance with the act There is a personal use exception for cigarettes imported into the United States that are not subject to tax under Chapter 98, Subchapter IV, of the Harmonized Tariff Schedule of the United States

Why the Tariff Act is Violated • The cigarette traffickers are not in compliance with the Cigarette Labeling and Advertising Act • In some, if not many instances, the original manufacturer has not submitted a list of ingredients to the Secretary of Health and Human Services • In most instances, the cigarette traffickers are selling U.S. Trademarked cigarettes, and the owner has not consented to the importation and distribution of the cigarettes • Importations are not accompanied by the certificates and certifications required by the Act • The Harmonized Tariff schedule refers to cigarettes imported into the United States by U.S. citizens traveling overseas; it does not provide an exception for cigarettes purchased from within the United States over the Internet • Primarily violated by Foreign-based cigarette traffickers

Smuggling • 18 U.S.C. § 545 • Unlawful to knowingly and willfully, with the intent to defraud the U.S., smuggle or attempt to pass any merchandise or false instrument • Unlawful to fraudulently or knowingly import or bring into the U.S., any merchandise contrary to law, or to receive, buy, sell, or transport any such merchandise

Why the Smuggling Statute is Violated • The smuggling statute will often be violated by foreign-based Internet cigarette traffickers as well as domestically-based cigarette traffickers who deal in counterfeit cigarettes • The cigarettes are shipped into the U.S. with the intent to defraud the U.S. in that (1) federal excise taxes are not paid, (2) cigarette shipments are structured to avoid detection and create the appearance that no duties are due, and (3) the trafficker may use a false declaration • The cigarettes are imported contrary to U.S. law in that the (1) cigarettes often do not comply with the CLAA, (2) the Tariff Act is often violated, and (3) importers are not licensed under U.S. law and may not possess non-Federally taxed cigarettes

Refuting Specific Claims made by Internet Cigarette Traffickers

We Sell from a Bonded Warehouse • Foreign based cigarette traffickers often claim that they can sell cigarettes tax free because they are selling from a bonded warehouse • A bonded warehouse is one in which a person is permitted to possess untaxed goods because they have paid a bond to the government, which “protects” the revenue, in the country in which they are located • Because the cigarettes are exported from the originating country, no tax is due in that country • However, selling from a bonded warehouse does not permit the trafficker to distribute untaxed cigarettes in the U.S. with out paying applicable taxes • Selling from a bonded warehouse also does not relieve the trafficker from liabilities associates with the commission of fraud or other crimes in the United States

Postal Conventions Allow for the International Shipment of Cigarettes • It is true that International Postal conventions allow for the international shipment via the mails of cigarettes • This means that it is not per se unlawful to ship cigarettes internationally as certain types of contraband may be • For instance, a legitimate licensed importer in the U.S., otherwise in compliance with all other provisions of U.S. law, could purchase cigarettes for importation and have them shipped via the Postal systems • However, this does mean that it is legal to possess, ship, mail, or distribute untaxed cigarettes, where such conduct would otherwise be in violation U.S. law, simply because of the postal convention – the trafficker and purchasers must be in compliance with all other provisions of U.S. law for the transaction to be lawful • The Postal convention does not shield other unlawful activities

Native Americans are not Subject to State or Federal Law Native Americans must comply with all Federal permit and tax requirements under the I.R.C.Native Americans are also subject to Federal criminal statutes such as the Contraband Cigarette Trafficking Act, the Jenkins Act, and the Wire and Mail Fraud statutes. Grey Poplars v. US, 282 F.3d 1175 (9th Cir. 2002). US 1,920,000 Cigarettes, 2003 WL 21730528 (W.D.N.Y. 2002) Native Americans can also be subjected to State taxing and permit requirements so long as the ultimate incidence of tax does not fall upon the Indian consumer, and the Indian consumer is a member of the tribe on whose reservation the cigarettes are sold U.S. v. Baker, 63 F.3d 1478 (9th Cir. 1995) U.S. v. Gord, 77 F.3d 1192 (9th Cir. 1996) Washington v. Colville, 447 U.S. 134 (1976) N.Y. v. Attea, 512 U.S. 61 (1994)

Otamedia Investigation • After the execution of warrants in the Otamedia investigation, Otamedia stopped shipping cigarettes into the United States. • Soon after the warrants, the major credit card companies revoked their agreements with Otamedia. • As a result, not only did Otamedia shut down U.S. operations, but so did the estimated 50 or so affiliated web sites.