Download

1 / 28

380 likes | 595 Views

Portfolio Monitoring and Rebalancing. 03/04/09. Monitoring and Rebalancing. Why do we need to monitor a portfolio? What should we monitor? What are the costs and benefits of rebalancing a portfolio? What methods can we use to rebalance?

E N D

Portfolio Monitoring and Rebalancing 03/04/09

Monitoring and Rebalancing • Why do we need to monitor a portfolio? • What should we monitor? • What are the costs and benefits of rebalancing a portfolio? • What methods can we use to rebalance? • What are the differences between the rebalancing methods?

The Need for Monitoring a Portfolio • Portfolios need to be monitored because any or all of the following factors may change: • Client’s needs and circumstances • Capital market conditions • Portfolio asset weights

Monitoring: Client’s Needs and Circumstances • Periodic meetings with the client can be used to assess if the client’s needs and circumstances have changed. • Changes should be used to revise the IPS.

Monitoring: Client’s Needs and Circumstances • Changes in investor circumstances and wealth: • Any major events in a client’s life may require the IPS to be reworked. • For institutional clients, changes to mandates or required returns may required the same.

Monitoring: Client’s Needs and Circumstances • Changes in investor circumstances and wealth: • For individuals, increases in wealth typically make clients more risk tolerant. • Permanent increases in wealth requires the reassessment of the client’s risk tolerance and return requirements.

Monitoring: Client’s Needs and Circumstances • Changes in liquidity requirement: • This can be caused by factors such as unemployment, divorce, house purchase, etc. for individuals • For institutions, changes in pension plan benefits, capital project funding, etc. can lead to different liquidity requirements. • The manager needs to ensure that a sufficient portion of the portfolio is in assets such as money-market instruments to satisfy withdrawals

Monitoring: Client’s Needs and Circumstances • Other changes: • Time horizon • Tax circumstances • Laws and regulations • Unique circumstances – concentrated stock positions, socially responsible investing, etc.

Monitoring: Market and Economic Changes • The economy moves through phases of expansion and contraction, each with unique characteristics. • Financial markets, which are linked to economic expectations, reflect the resulting changing relationships among asset classes and individual securities.

Monitoring: Market and Economic Changes • Changes in asset risk attributes: • The historical relationship between asset mean returns, standard deviations and correlations may change meaningfully. • These changes may require changes to allocations. • It may provide active managers profitable opportunities if the market’s view is pessimistic.

Monitoring: Market and Economic Changes • Market cycles: • Market cycles allow for short-term views on asset classes and securities. • Historically, cyclical tops and bottoms are examples of the opportunity to take advantage of mean reversion of asset classes. • For broader asset classes, we can compare earnings yields to bond yields.

Monitoring: Market and Economic Changes • Central bank policy: • Immediate impact of Fed policy in bond markets is on short-term yields (not long-term). • Higher interest rates usually hurt stock returns and lower interest rates usually enhance stock returns.

Monitoring: Market and Economic Changes • Yield curve: • The yield curve tends to be steep (and upward sloping) during recessions, flatter during expansions and inverted prior to recessions. • Unusually steep curves tend to presage bond rallies.

Monitoring: Portfolio • A portfolio is never exactly optimal even after one day. • Do the costs of adjustment outweigh any expected benefits from eliminating small differences between the current portfolio and the best possible one?

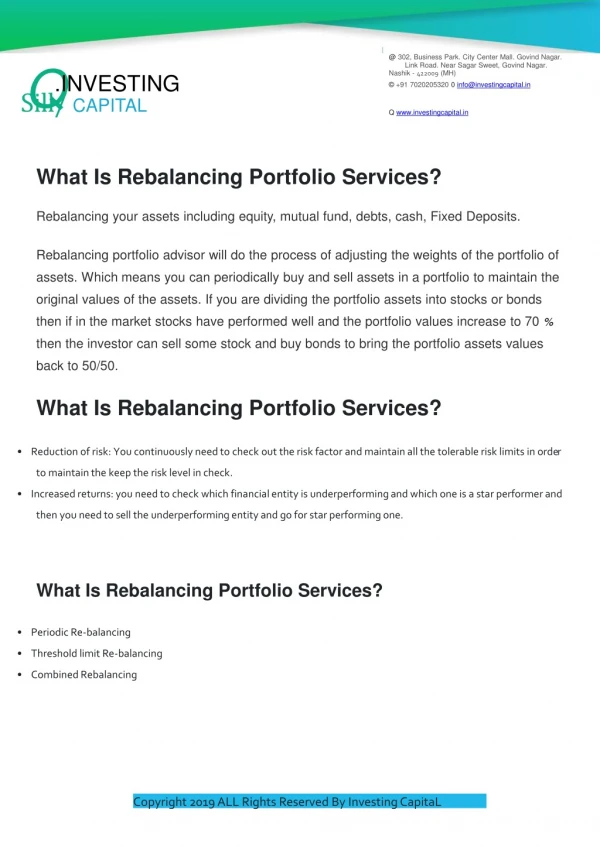

Rebalancing • Rebalancing can include: • Adjusting the actual portfolio to the current strategic asset allocation because of price changes in portfolio holdings • Revisions to the client’s target asset class weights

Rebalancing: Practical Benefits • Higher-risk assets will tend to represent a larger proportion of the portfolio over time. • Over time, the types of risk exposures will change. • Over time, the portfolio may include over-priced assets. • Historically, disciplined rebalancing has shown to increase returns and reduce risk for the portfolio.

Rebalancing: Costs • Transaction costs are sometimes difficult to measure. • They include commissions and illiquidity costs. • Tax costs can also be significant especially when rebalancing requires the sale of appreciated assets.

Rebalancing Discipline • A rebalancing discipline is a strategy for rebalancing. • Most managers adopt either a calendar rebalancing or percentage-of-portfolio rebalancing.

Rebalancing Discipline: Calendar • Calendar rebalancing is the simplest approach to rebalancing a portfolio. • Rebalancing can be done monthly, quarterly or annually, where quarterly is the most popular. • One drawback of this method is that it is unrelated to market behavior.

Rebalancing Discipline: Percentage-of-Portfolio • Percentage-of-Portfolio rebalancing involves setting rebalancing trigger points stated as a percentage of the portfolio’s value. • If the target asset class weight is 40% and the trigger points are 35% and 45%, then the 35% to 45% range is considered the corridor or tolerance band (40% + 5%) .

Rebalancing Discipline: Percentage-of-Portfolio • Rebalancing using the Percentage-of-Portfolio method is directly related to market performance. • Ideally, daily monitoring is required. • Rebalancing trades can occur on any date therefore allowing for tighter control on divergences from target proportions.

Rebalancing Discipline: Percentage-of-Portfolio • Corridors can be set in an ad hoc manner. • However, research suggests that corridors for each asset class should be set based on: • Transaction costs • The greater the costs, the wider the corridor • Correlation (with other asset classes) • Generally, higher correlations should lead to wider corridors • Volatility • The greater the volatility, the narrower the corridor • Risk Tolerance • The higher the risk tolerance, the wider the corridor

Rebalancing Discipline: Strategies Compared • When rebalancing a portfolio to its strategic asset allocation weights, we are implicitly carrying out a constant-mix strategy. • We can compare this strategy to a buy-and-hold strategy and a constant-proportion portfolio insurance (CPPI) strategy.

Rebalancing Discipline: Buy-and-Hold • A buy-and-hold strategy is one where an initial asset mix is purchased and nothing is done subsequently. • The floor value in this strategy is the value of the risk-free assets: Portfolio value = Risky asset value + Floor value Investment in stock = cushion =portfolio value – floor value

Rebalancing Discipline: Constant-Mix • A constant-mix strategy is one where the portfolio is rebalanced to the strategic asset allocation weights. • The target investment in the risky asset is: Target investment in risky asset = m * Portfolio value where m represents the target proportion in the risky asset.

Rebalancing Discipline: Constant-Mix • A constant-mix strategy does better than a buy-and-hold strategy if risky asset returns are characterized more by reversals than trends. • A buy-and-hold strategy works better during strong bull and bear markets.

Rebalancing Discipline: CPPI • A constant-proportion strategy adjusts risky asset investment based on the relationship between portfolio value and floor value: Target investment in risky asset = m * (Portfolio value-floor value) where m is a fixed constant. • The CPPI strategy works best when the markets are momentum-oriented and is therefore exactly the opposite of a constant-mix strategy.

Readings • RM 5