Download

1 / 69

690 likes | 774 Views

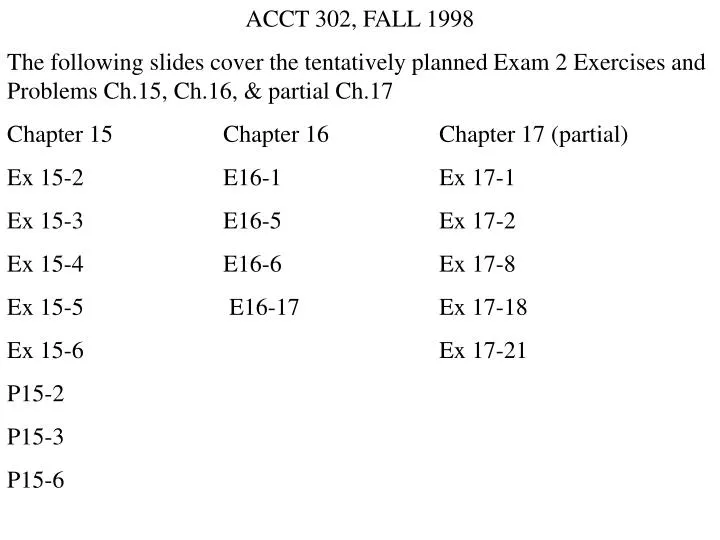

ACCT 302, FALL 1998 The following slides cover the tentatively planned Exam 2 Exercises and Problems Ch.15, Ch.16, & partial Ch.17 Chapter 15 Chapter 16 Chapter 17 (partial) Ex 15-2 E16-1 Ex 17-1 Ex 15-3 E16-5 Ex 17-2 Ex 15-4 E16-6 Ex 17-8 Ex 15-5 E16-17 Ex 17-18

E N D

ACCT 302, FALL 1998 The following slides cover the tentatively planned Exam 2 Exercises and Problems Ch.15, Ch.16, & partial Ch.17 Chapter 15 Chapter 16 Chapter 17 (partial) Ex 15-2 E16-1 Ex 17-1 Ex 15-3 E16-5 Ex 17-2 Ex 15-4 E16-6 Ex 17-8 Ex 15-5 E16-17 Ex 17-18 Ex 15-6 Ex 17-21 P15-2 P15-3 P15-6

Splitting Lump Sums received for Bonds + Stock: 1. Incremental Method: If total received and value of one is known… (See Ill 15-3, p. 768) 2. Proportional Method: If market value of both are known then split cash received based on relative % of total value received. (See Ill. 15-2, p. 767) Ex 15-6: Bonds $5,000,000 5/9 Stock 10,000 x 10 x $40 = $4,000,000 4/9 Total $9,000,000

Part 1a asks for the Incremental Method. The Incremental method is demonstrated next, followed by a discussion of individual Calculations in the JE

Ex. 15-6 Where did the $200,000 bond issue costs come from??? Value of Units Sold: % Bonds 5,000,000 (5/8.8) Stock 9,600 units x 10 shares x $40 = 3,840,000 (3.8/8.8) Total 8,840,000 Total UnderWriting fee 400 units x $880 = $352,000 Amount Allocated to Bonds vs. Stock: Bonds: (5/8.8) x $352,000 = $200,000 rounded (Shown as Bond Issue Cost) Stock: (3.8/8.8) x $352,000 = $152,000 (Reflected as a decrease to PIC Excess, See p. 769)

Where did PIC EXCESS $3,148,000 come from??? PLUG!!! Bond Issue Cost + Cash 200,000 + 8,448,000 = $8,648,000 - Bonds Payable (5,000,000) - Par of Stock Issued ( 500,000) Net Credit to PIC Excess $3,148,000 =========

Part a2. asks for the Proportional Method. The proportional method is demonstrated next, followed by a discussion of individual Calculations in the JE

P15-2 REMEMBER: 5/1: (.7 x $120 x 500)/ 3 = $14,000 6/1: 14,000 - ((.7 x $120 x 100sh)/3)) = $11,200 6/5: 1. Remove CS Subscribed associated with her 2. Remove remaining Subscription Rec Associated with her (100 x $120) x 70% x (2/3) … she made 1 pymt! 3. Balance is due to her 10,000 - 5,600 = 4,400 6/17: Sold for 105 vs 100 orig subscript… She will get Net Excess 10,500 - 10,000 = 500 BUT THIS GETS REDUCED BY $125

Dividends: Can They be Paid vs. Can We Pay Them? Legal Issues Working Capital Issue The trend??? What is a Dividend Yield? Div / Stk Price

Stock Dividends: Permanent transfer from RE to PIC Small (<20 -25%) base transfer on Market Price Large (>25%) base transfer on Par Value Own more shares… each worth proportionately less Not a thing of value? Stock Split: No JE, Just an adjustment of Par

Ex. 16-5 a) Cumulative Preferred, fully participating: Preferred Common Total Remaining 366,000 1 Yr Arrears 14,000 14,000 352,000 Current 14,000 210,000 224,000 128,000 Split Remaining 8,000 120,000 128,000 0 (Based on % of Total Par Value) .2/3.2 x 128,000 = 8,000 3/3.2 x 128,000 = 120,000

Ex. 16-5 b) Noncumulative, non-participating Split $366,000 Preferred Common Total 14,000 352,000 366,000 c) Noncumulative, participating in excess of 10% Preferred Common Total Remaining 366,000 Current 14,000 210,000 224,000 142,000 Last 3% 90,000 90,000 52,000 Split 52,000 3,250 48,750 52,000 0 .2/3.2 x 52,000 = 3,250 3/3.2 x 52,000 = 48,750