Download

1 / 52

540 likes | 640 Views

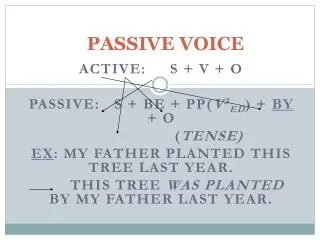

Passive Loss Rules. Matthew K. Becker, CPA BDO Douglas J. Patch, Godfrey & Kahn, S.C. November 4, 2010. mw5514693. History of Passive Loss Rules. Prior to TRA 1986, few limitations were placed on ability to use deductions from one activity to offset income from another activity.

E N D

Passive Loss Rules Matthew K. Becker, CPA BDO Douglas J. Patch, Godfrey & Kahn, S.C. November 4, 2010 mw5514693

History of Passive Loss Rules • Prior to TRA 1986, few limitations were placed on ability to use deductions from one activity to offset income from another activity. • Tax Shelters were designed to generate large deductions with minimal investment. • TRA 1986 addressed this situation with many lines of attack: expansion of AMT, extension of at-risk rules to real estate and passage of the passive loss rules.

Effect of Passive Loss Rules • Loss from passive activities can not offset active income or portfolio income. • Exceptions to general rule of disallowance: • Dispositions • Former passive activity rules • $25,000 Rental/Real Estate Activity Rule

Effect of Passive Loss Rules - Dispositions • Dispose of entire interest in activity in a fully taxable transaction allows utilization of suspended losses. • What is an activity? • What is a qualifying disposition?

Effect of Passive Loss Rules - Dispositions • Appropriate Economic Unit to determine “activity.” • Facts and circumstances relevant in grouping. • Decision made at entity level. • Limitations • Rental Activity/Non-rental activity • Real Property Rental/Personal Property Rental

Effect of Passive Loss Rules - Dispositions • Must dispose of entire interest in activity • Disposition must be fully taxable • Related Party Rule • Installment sales

Effect of Passive Loss Rules – Other Triggering Events • Activity ceases to be passive • Not a disposition • Can use suspended losses to offset income from the same activity • $25,000 Rental Real Estate Rule • Can treat $25,000 as active if active in the rental • Otherwise, real estate is per se passive

Determining Whether an Activity is Passive • Trade or Business in which the Taxpayer does not materially participate. • Rental Activity.

Material Participation Standard • Material Participation means involvement is regular, continuous and substantial. • Regulations provide Material Participation standard met if and only if one of seven tests met. • First six tests are narrowly quantitative, the seventh is a facts and circumstances test.

Material Participation – Test One • Taxpayer must participate more than 500 hours • Taxpayer must own activity at time of services for services to count • Certain hours disregarded: • Non-owner work done to meet 500 hour test • Work done in investor capacity unless taxpayer involved in day-to-day management

Material Participation – Test Two • Met if the taxpayer’s participation constitutes substantially all of the participation in the activity. • If test met, does not matter how few hours taxpayer spends participating in activity. • Services of non-owners is considered.

Material Participation – Test Three • Met if a taxpayer participates in an activity for more than 100 hours and his participation is not less than that of any other individual during the same year. • Work performed by non-owners is considered. • Not clear whether number of hours is sole determinant of who participates more.

Material Participation – Test Four • Met if aggregate participation in all “significant participation activities” exceeds 500 hours. • A SPA is a non-rental trade or business in which taxpayer participates for more than 100 hours and none of the other tests are met. • If fail the 500 hour aggregate test, income from SPAs is considered active, but loss is considered passive.

Material Participation – Test Five • If materially participated (based on other tests) in five of past ten years, then considered to materially participate in current year. • Test designed to prevent flip-flops, i.e., treatment of an activity as nonpassive when it generates losses and active when it generates income.

Material Participation – Test Six • Met if participated in a personal service activity for any three prior taxable years. • Personal service activity means any business where capital is not a material income-producing factor including, but not limited to, health, law, engineering, architecture, accounting, performing arts or consulting. • Several cases in the area.

Material Participation – Test Seven • Met if, based on all the facts and circumstances, a taxpayer establishes regular, continuous and substantial involvement in the activity. • Regulations specify this test cannot be met if taxpayer participates in an activity for 100 hours or less. • Management services are disregarded unless: (1) no other individual is compensated for providing management services and (2) no other individual performs a greater number of management hours.

Material Participation – Other Considerations • Distinction between investors and entrepreneurs • Treatment of limited partners • Material Participation by legal entities

Definition of Rental Activity • A rental activity is an activity where payments are for the use of tangible property. • Exception One: Average customer use period of seven days or less. • Exception Two: Average use of 30 days or less and significant personal services. • Exception Three: Extraordinary personal services.

Definition of Rental Activity, cont. • Exception Four: Rentals incident to nonrental activities of taxpayer. • Exception Five: Property customarily made available for nonexclusive use by various customers. • Exception Six: Property rented to a pass through entity or joint venture in which the taxpayer owns an interest. • Exception Seven: Rental of taxpayer’s residence.

Real Estate Operators • Taxpayers who qualify as real estate operators must treat their rental activities as nonpassive upon a showing of material participation. • Definition of real estate operator: • Closely held C corporation with more than 50% of gross receipts from real property. • Individuals who perform more than 50% of services in a real property trade or business AND more than 750 hours in real property trades or businesses in which he materially participates.

Real Estate Operators • Must group all real estate activities together as a whole or treat separately. • Must still meet one of the seven activity tests for trade or business to be considered active.

Net Income from Nonshelterable Passive Activities (“NOPAs”) • Six situations in which net gain, but not net loss, from a passive activity is treated as nonpassive. • Can use suspended loss from NOPA to offset income from the NOPA. • NOPA #1: Significant Participation Passive Activities

NOPAs, cont. • NOPA #2: Rental of Nondepreciable Property. • NOPA #3: Equity-Financed Lending Activity. • NOPA #4: Property Rented Incidental to Development Activity

NOPAs, cont. • NOPA #5: Property Rented to a Nonpassive Activity of the Taxpayer. • NOPA #6: Certain Royalties Received Through a Pass Through Entity.

Self-Charged Interest Rule • Interest income is portfolio income generally not available to offset loss from a passive activity. • Self-charged interest rule allows offset of interest expense of debtor passive activity attributable to loan from owner.

Self Charged Interest Example X owns 50%; Y owns 50% of LLC. LLC conducts per se passive rental activity. X loans $1,000,000 to LLC at 10% interest rate. X can treat $50,000 of interest income as passive income. 26

Self Charged Interest Example, Cont. • What if $1,000,000 were contributed as preferred equity with a 10% priority return? • Economics between X and Y would be the same • Entire special allocation is passive income and could be offset with passive loss. • Must take care to avoid having the special allocation treated as a guaranteed payment. 27

Rev. Proc 2010-13 • Requires taxpayers to report their groupings and regroupings of activities. • Also requires reporting additions of activities to current groupings. • Effective for tax years beginning on or after January 25, 2010.

Reporting Requirements – New Groupings • The taxpayer must file a statement identifying the activities. • Statement must be attached to the original return for the first taxable year in which two or more activities are grouped.

Reporting Requirements – Existing Groupings • No disclosure is required for existing groupings that are unchanged. • Statement must be attached to the tax return in any year that an activity is added to an existing group. • When adding an activity, the entire group must be disclosed.

Regrouping Activities • Regrouping is required for groups that are clearly inappropriate or have a material change in facts and circumstances. • Failing to regroup inappropriate activities will cause each activity to be treated separately.

Special Rules –Partnerships and S-Corps • Partnerships and S Corporations must report groupings to partners and shareholders. • Grouping is reported by separately stating income and loss for each group on attachments to the entity’s Schedule K-1.

Reporting Requirements – Partners and Shareholders • Partners and shareholders are generally not required to report groupings disclosed by the entity. • Separate disclosure is required if the partner or shareholder: • Groups together activities that the entity does not group together, • Groups entity activities with activities conducted directly by partner or shareholder, and/or • Groups entity activities with activities conducted through other passive entities.

Partners & ShareholdersExample – Grouping Partnerships • Assume the taxpayer holds a partnership interest in a grocery distributor as well as a partnership interest in a separate entity that owns the warehouse rented to the distributor. • Assume both partnerships are under common control and that the warehouse is rented predominantly to the distributor.

Partners & ShareholdersExample – Grouping Partnerships cont. • Each partnership attaches a statement of activity to the partner’s K-1. • The taxpayer may elect to group these activities into a single activity. • If grouped, the taxpayer’s material participation is measured by testing both activities together as one activity.

Partners & ShareholdersExample – Grouping at Entity Level • Assume the same facts as the previous example except that the distributor activity and the warehouse activity are part of one partnership. • Further assume that the partnership chooses to group the activities. • Assume the taxpayer materially participates in the distribution activity but not the warehouse activity.

Partners & ShareholdersExample – Grouping at Entity Level cont. • The activities must remain grouped on the partner’s return. • If the taxpayer’s material participation in the distributor activity is not enough to make him a material participant in the entire economic unit, both activities become passive.

Grouping Factors • Any reasonable method can be used to group activities. • Grouped activities must constitute appropriate economic units. • Similarities and differences in types of trades or businesses. • The extent of common control and/or ownership. • Geographical location. • Interdependencies between or among the activities.

Grouping Factors cont. • Business interdependencies can arise from: • Having the same customers, • Having the same employees, and/or • Having a single set of books or records. • Interdependencies among activities can also arise when: • Activities purchase or sell goods to each other, or • Products or services are normally provided together.

Grouping Factorscont. • Taxpayers may not combine or separate activities each tax year. • Regrouping is only allowed in circumstances where the initial grouping was: • “clearly inappropriate or there has been a material change in the facts and circumstances that makes the original grouping inappropriate.” • Commissioner can regroup a taxpayer’s activities when clearly inappropriate.

Grouping FactorsExample – Appropriate Economic Unit • Taxpayer owns a bakery and a movie theater in a mall located in Chicago, IL. • He also owns a bakery and a movie theater in a mall located in Houston, TX. • Depending on other circumstances, the taxpayer may: • Group all the activities into a single activity, • Group them as a movie theater activity and a bakery activity, • Group them as a Chicago activity and a Houston activity, or • Treat them as four separate activities.

Benefits of Grouping • Taxpayers can potentially combine passive rental activities with profitable active trade or business activities. • Activities can only be combined if the activities constitute an appropriate economic unit and: • The rental activity is insubstantial in relation to the trade or business activity, • The trade or business activity is insubstantial in relation to the rental activity, or • They have the same proportionate ownership.

Benefits of GroupingExample – Proportionate Ownership • Husband is the sole owner of an S corporation that conducts a grocery store trade or business activity. • Wife is the sole owner of an S Corporation that owns and rents out a building. • Part of the Wife’s building is rented to the Husband’s grocery store. • Both activities are reported on a joint tax return. • The activities can be combined as if the grocery store S Corporation owned the portion of the rented building used by the grocery store.

Regrouping ActivitiesExample – Material Change • Assume the same facts as the previous example except that the grocery store business was moved to an unrelated location. • The rental property is now rented to an unrelated party. • A material change in facts and circumstances has occurred and the activities must be regrouped separately.

Suspended Losses – General Rules • Losses can generally be suspended for two reasons: • Passive activity loss rules • At-Risk Basis Rules • Passive losses can only offset passive income. • Passive losses are carried forward until used or activity is disposed. • All losses are limited to amount investor has “at risk”.

Suspended Losses – Combined Passive Activities • Total losses from combined passive activities are allocated among each separate activity. • The ratable portion of each separate activity’s deductions that are suspended are determined as follows:

Suspended LossesExample – Allocation • Assume these are treated as a single passive activity with the following results: • The loss would be allocated as follows:

Suspended Losses – Example – Allocation (cont.) • Assume that the taxpayer disposed of the movie theater the next year. • The taxpayer can elect to treat the movie theater as a separate activity in the year disposed. • The $12,000 suspended loss would be deductible in full to offset non-passive income upon disposition.

At-Risk Basis • In general, limits losses to what the taxpayer actually has “at risk”. • At-risk losses are suspended until the taxpayer increases at-risk basis through income or contributions. • Suspended at-risk losses are subject to the passive loss rules in the year in which the loss is allowed.

At-Risk BasisExample – Suspended Losses (Year 1) • Assume the taxpayer purchased an interest in a passive activity with the following transactions in Year 1. • The taxpayer has a $15,000 suspended loss due to the passive activity rules and a $5,000 suspended loss due to the at-risk rules.