Download

1 / 5

50 likes | 53 Views

Private insurers offer Medisave-approved Integrated Shield Plans (IP), which act as add-ons to MediShield Life and offer more comprehensive protection. Read the blog for more details.

E N D

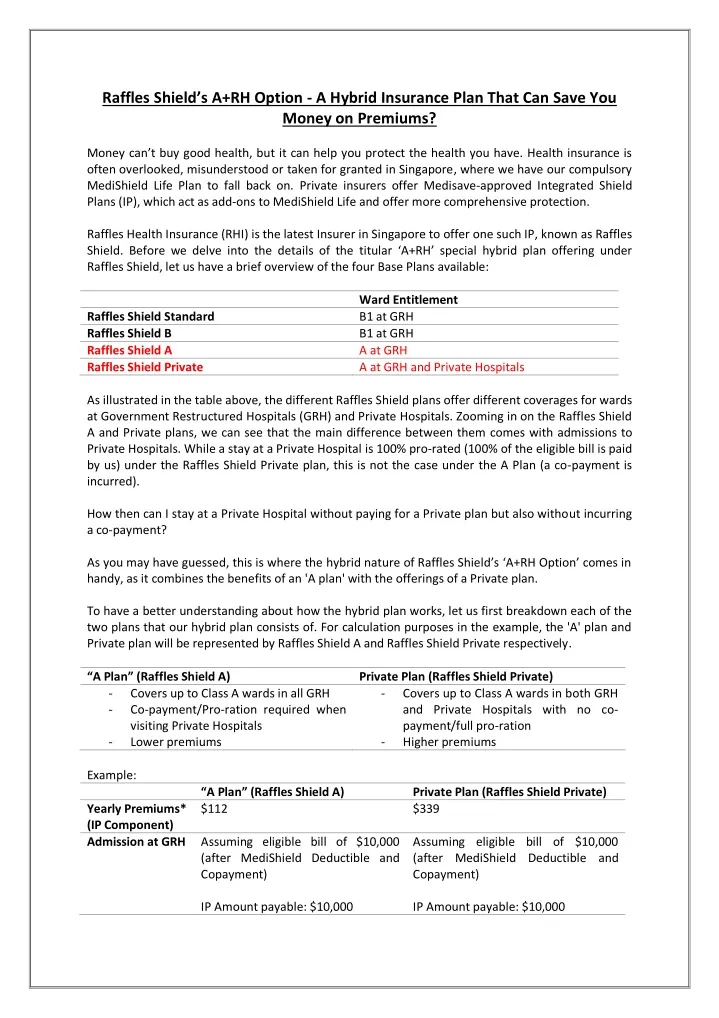

Raffles Shield’s A+RH Option - A Hybrid Insurance Plan That Can Save You Money on Premiums? Money can’t buy good health, but it can help you protect the health you have. Health insurance is often overlooked, misunderstood or taken for granted in Singapore, where we have our compulsory MediShield Life Plan to fall back on. Private insurers offer Medisave-approved Integrated Shield Plans (IP), which act as add-ons to MediShield Life and offer more comprehensive protection. Raffles Health Insurance (RHI) is the latest Insurer in Singapore to offer one such IP, known as Raffles Shield. Before we delve into the details of the titular ‘A+RH’ special hybrid plan offering under Raffles Shield, let us have a brief overview of the four Base Plans available: Ward Entitlement Raffles Shield Standard B1 at GRH Raffles Shield B B1 at GRH Raffles Shield A A at GRH Raffles Shield Private A at GRH and Private Hospitals As illustrated in the table above, the different Raffles Shield plans offer different coverages for wards at Government Restructured Hospitals (GRH) and Private Hospitals. Zooming in on the Raffles Shield A and Private plans, we can see that the main difference between them comes with admissions to Private Hospitals. While a stay at a Private Hospital is 100% pro-rated (100% of the eligible bill is paid by us) under the Raffles Shield Private plan, this is not the case under the A Plan (a co-payment is incurred). How then can I stay at a Private Hospital without paying for a Private plan but also without incurring a co-payment? As you may have guessed, this is where the hybrid nature of Raffles Shield’s ‘A+RH Option’ comes in handy, as it combines the benefits of an 'A plan' with the offerings of a Private plan. To have a better understanding about how the hybrid plan works, let us first breakdown each of the two plans that our hybrid plan consists of. For calculation purposes in the example, the 'A' plan and Private plan will be represented by Raffles Shield A and Raffles Shield Private respectively. “A Plan” (Raffles Shield A) Private Plan (Raffles Shield Private) - Covers up to Class A wards in all GRH - Co-payment/Pro-ration required when visiting Private Hospitals - Lower premiums Example: “A Plan” (Raffles Shield A) Yearly Premiums* (IP Component) Admission at GRH Assuming eligible bill of $10,000 (after MediShield Deductible and Copayment) IP Amount payable: $10,000 - Covers up to Class A wards in both GRH and Private Hospitals with no co- payment/full pro-ration Higher premiums - Private Plan (Raffles Shield Private) $339 $112 Assuming eligible bill of $10,000 (after MediShield Deductible and Copayment) IP Amount payable: $10,000

Insured Payable: $0 Assuming eligible bill of $20,000 (after MediShield Deductible and Copayment) Insured Co-payment: 40% IP Amount payable: $12,000 Insured Payable: $8,000 Amt Paid in Premiums: $560 Amt Paid for Admission to GRH: $0 Amt Paid for Admission to Private Hospital: $8,000 Total Paid for admission to GRH: $560 Total paid for admission to Private Hospital: $8,560 Insured Payable: $0 Assuming eligible bill of $20,000 (after MediShield Deductible and Copayment) Insured Co-payment: 0% IP Amount payable: $20,000 Insured Payable: $0 Amt Paid in Premiums: $1,695 Amt Paid for Admission to GRH: $0 Amt Paid for Admission to Private Hospital: $0 Total Paid for admission to GRH: $1,695 Total paid for admission to Private Hospital: $1,695 Admission Private Hospital at Assuming admission 5years 1 after *The yearly premiums for the example above is based on the premiums for a 31 year old individual. From the example above, we can see that the benefit of getting an ‘A’ plan over getting a Private plan mainly stems from the savings in yearly premiums. Over 5 years, someone with an ‘A’ plan pays more than $1,000 less in premium payments than another person with a Private plan. The downside to getting an ‘A’ plan is that you need to be sure that a Private Hospital stay is not something you are interested in, as just one admission to a Private Hospital would incur a heavy co- payment and see all the savings you got on your yearly premiums wiped out. Conversely, if you purchased a Private Plan, the example indicates how you should always stay at a Private Hospital to get your “money’s worth” out of your plan. If you decide to stay at a GRH instead, the coverage would be the same, but you would have spent over $1,000 more than someone covered under an “A Plan”. This clear segregation between GRH and Private Hospitals can be upsetting to some of us due to the limited flexibility of choice afforded to us. After all, we are looking ideally for the best of both worlds, with comfortable healthcare at affordable prices. This is where Raffles Shield’s special ‘Raffles Hospital (RH) Option’ comes into play. As part of Raffles Medical Group (RMG), Raffles Health Insurance has special access to Raffles Hospital, a 380-bedded Tertiary Private Hospital with specialists spanning 35 disciplines. The “RH option” is a feature exclusive to Raffles Shield. It is an add-on to a Raffles Shield A plan, hence its hybrid nature and the term “A+RH”, and allows you to stay at any GRH Class A ward or Raffles Hospital with full pro-ration. Admissions to other Private Hospitals are still possible, although youwill incur the co-payment element in the same was as an “A Plan”.

Essentially, the Raffles Shield A+RH Option acts as a middle ground,offering you access to Private Healthcare at lower premiums than a Private plan. Yearly premiums for this plan are about 30% lower than other Private plans available on the market. In this way, the A+RH Option gives you the cost savings of an ‘A’ plan, while also providing you with the option of Private Healthcare, allowing you the availability of choice. Add on to Raffles Shield ‘A’plan to have the choice of staying at Raffles Hospital, a Private Hospital, with no co-payment. Example: “A Plan” (Raffles Shield A) Yearly Premiums* (IP Component) Admission at GRH $10,000 (after MediShield Deductible and Copayment) IP Amount payable: $10,000 Insured Payable: $0 Insured Payable: $0 Admission at Private Hospital (excluding Raffles Hospital) and Copayment) Insured Co-payment: 40% IP Amount payable: $12,000 Insured Payable: $8,000 Insured Payable: $8,000 RH Option Raffles A+RH Option Private Plan (Raffles Shield Private) $339 $112 $223 Assuming eligible bill of Assuming eligible bill of $10,000 MediShield and Copayment) IP Amount $10,000 Assuming eligible bill of $10,000 MediShield Deductible and Copayment) IP Amount $10,000 Insured Payable: $0 Assuming eligible bill of $20,000 MediShield Deductible and Copayment) Insured Co-payment: 0% IP Amount $20,000 Insured Payable: $0 (after (after Deductible payable: payable: Assuming eligible bill of $20,000 MediShield Deductible Assuming eligible bill of $20,000 MediShield and Copayment) Insured Co-payment: 40% IP Amount $12,000 (after (after (after Deductible payable: payable: Admission at Assuming eligible bill of Assuming eligible bill of Assuming eligible bill of

Raffles Hospital $20,000 MediShield Deductible and Copayment) Insured Co-payment: 40% IP Amount $12,000 Insured Payable: $8,000 Amt Paid in Premiums: $560 Amt Paid for Admission to GRH: $0 Amt Paid for Admission to Private $8,000 Total paid for admission to Private $8,560 (after $20,000 MediShield and Copayment) Insured Co-payment: 0% IP Amount $20,000 Insured Payable: $0 Amt Paid in Premiums: $1,115 Amt Paid for Admission to GRH: $0 Amt Paid for Admission to Private $8,000 Amt Paid for Admission to RH: $0 Total paid for admission to Private (Raffles $1,115 (after $20,000 MediShield Deductible and Copayment) Insured Co-payment: 0% IP Amount $20,000 Insured Payable: $0 Amt Paid in Premiums: $1,695 Amt Paid for Admission to GRH: $0 Amt Paid for Admission to Private Hospital: $0 Total paid for admission to Private $1,695 (after Deductible payable: payable: payable: Assuming admission after 5 years 1 Hospital: Hospital: Hospital: Hospital Hospital): Hospital: *The yearly premiums for the example above is based on the premiums for a 31 year old individual. The scenario above illustrates how an admission to a Private Hospital, Raffles Hospital, would cost less with the A+RH hybrid plan than with a conventional Private plan, saving you close to $600. Yearly premiums for the Raffles Shield A+RH plan also lie in between an ‘A’ plan and a Private plan. This makes it a cost-effective choice for anyone who would like Class A ward coverage at GRH with the option of Private Healthcare as well.

Raffles Shield A+RH Option allows access to Private Healthcare at one of the lowest premiums on the market. This is possible as RHI is the only insurer backed by a medical group. Speak to our Raffles Health Advisor today to learn more about Raffles Shield A+RH option! For more details about Raffles Shield plans, click here.