Download

1 / 8

90 likes | 246 Views

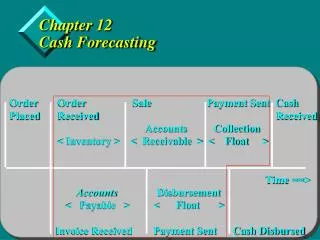

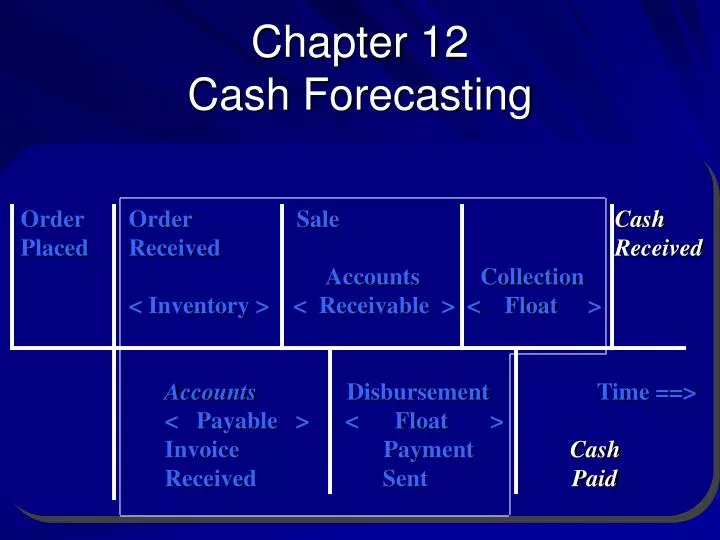

Chapter 12 Cash Forecasting. Order Order Sale Cash Placed Received Received Accounts Collection

E N D

Chapter 12Cash Forecasting • Order Order Sale Cash • Placed Received Received • Accounts Collection • < Inventory > < Receivable > < Float > • AccountsDisbursement Time ==> • < Payable > < Float > • Invoice Payment Cash • Received Sent Paid

Learning Objectives • Explain importance of short-term cash forecasts • Indicate why the monthly cash budget is important to top management, and specify the two objectives for its development • Indicate how daily cash forecasting differs from monthly forecasting • Explain the receipts and disbursements, pro forma balance sheet, and distribution methods of cash forecasting

Forecasting Monthly Cash Flows • Importance to top management: “valuable” • Typical billing and payment cycle is monthly • Monthly interval adequate for anticipating funding requirements (but quarterly may hide intra-quarter imbalances) • Monthly cash forecast objectives • Accuracy (+/- 5% or +/- 10% on year-ahead forecast) • Usefulness (allows timely and appropriate managerial responses to foreseen shortages or surpluses) • Forecasting philosophy (see next slide) • Forecast parameters (see 2nd following slide) • Statistical tools (see Appendixes 12A and 12B)

Forecasting Philosophy • Number and type of forecasts • Expenditure on forecasts • External versus internal forecasts • Quantitative versus judgmental forecasting

Forecast Parameters • Forecast horizon • Variable identification • Modeling the cash flow sequence • Format of the receipts and disbursement forecast • Interpreting the receipts and disbursement forecast • Developing the receipts and disbursement forecast • Modified accrual method • Pro forma balance sheet method • Model estimation • Model validation

Forecasting Daily Cash Flows • Horizon • Variable identification • Modeling the cash flow sequence • Structuring the daily cash forecast • Distribution method • Model estimation • Model validation

The Distribution Method • Using the distribution method for disbursements • Using the distribution method for collections • Example • Final comments

Summary • The chapter began with a discussion of the philosophy and environment within which cash forecasts are made • The primary value of forecasts is to borrow less or extend investment maturities • The two major cash forecasting time intervals (monthly and daily) were presented and the processes for variable identification, modeling the cash flow sequence, model estimation, and model validation discussed