Download

1 / 33

330 likes | 518 Views

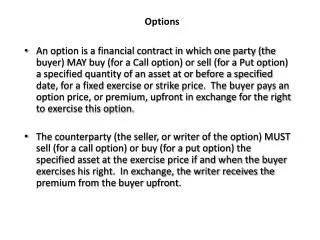

Options. Prepared by Paul A. Spindt. A Call Option. Gives its owner the right (not obligation) to buy an asset (the underlying ) at a specified price (the exercise price ) on (and perhaps before) a given date (the expiration date ). A Put Option.

E N D

Options Prepared by Paul A. Spindt

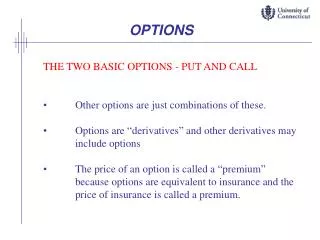

A Call Option Gives its owner the right (not obligation) • to buy an asset (the underlying) • at a specified price (the exercise price) • on (and perhaps before) a given date (the expiration date)

A Put Option Gives its owner the right (not obligation) • to sell an asset (the underlying) • at a specified price (the exercise price) • on (and perhaps before) a given date (the expiration date)

Options Lingo • option premium • intrinsic value; time value • European; American • long; short • covered; naked

Example • Here’s a quote from Wednesday’s Wall Street Journal: -Call- -Put- SunMic 583/4 60 Jan 540 35/8 1105 37/8 Wednesday’s closing stock price Premium Expiration date Option strike price Volume

Option Payoff: Calls Payoff Stock Price (at Expiration) 0 Strike Price

Option Payoff: Puts Payoff Stock Price (at Expiration) 0 Strike Price

Option Value • Intrinsic value • The intrinsic value of a call is max(0,S-X) • The intrinsic value of a put is max(X-S,0) • Time value • Time value is the option premium minus intrinsic value

} (S-X) S When S is greater than X, the intrinsic value of the call is $(S-X) The Value of a Call Value X This call option has an intrinsic value of $3.75 and time value of $3.50 -Call- -Put- SunMic 583/4 55 Jan 166 71/4 109 2

When S is less than X, the intrinsic value of the call is $0 The Value of a Call Value X This call option has an intrinsic value of $0 and time value of $3.625 -Call- -Put- SunMic 583/4 60 Jan 540 35/8 1105 37/8

The Value of a Put Value X This put option has an intrinsic value of $1.25 and time value of $2.625. When S is less than X, the intrinsic value of the put is $(X-S) -Call- -Put- SunMic 583/4 60 Jan 540 35/8 1105 37/8

The Value of a Put Value X This put option has an intrinsic value of $0 and a time value of $2.00 When S is greater than X, the intrinsic value of the put is $0 -Call- -Put- SunMic 583/4 55 Jan 166 71/4 109 2

Put-Call Parity • In an efficient market two investments with the same payoff ought to have the same price.

Put-Call Parity This principle implies that • the current stock price plus the price of a put

Put-Call Parity should equal • the price of a call plus the PV of the exercise price

The Payoff on a Stock Payoff Terminal value of investment in stock A stock is currently selling at $45. A call and a put each with a strike price of $50 and an expiration date 6 months from now are available. Stock Price at Expiration $50 $50

The Payoff on a Put Payoff Terminal value of investment in stock (minus $50) Terminal value of investment in put Stock Price at Expiration $0 $50

The Payoff on a Stock and a Put Payoff Terminal value of investment in both stock and put Stock Price at Expiration $50 $50

The Payoff on a Call Payoff Terminal value of investment in call Stock Price at Expiration $0 $50

The Payoff on a Bond Payoff Terminal value of investment in call (plus $50) Stock Price at Expiration $50 $50 Terminal value of investment in bond

The Payoff on a Call and a Bond Payoff Terminal value of investment in call and bond Stock Price at Expiration $50 $50 Terminal value of investment in bond

For Example: • Here’s a put and a call on SunMic. Each has a strike price of $60. The current stock price is $58.75, so the call is out of the money and the put is in the money. Both expire in one month. -Call- -Put- SunMic 583/4 60 Jan 540 35/8 1105 37/8

For Example: • Put-call parity implies that -Call- -Put- SunMic 583/4 60 Jan 540 35/8 1105 37/8

Determinants of Option Value • The price of the underlying asset The value of a call rises (the value of a put falls) as the price of the underlying asset rises, all other things equal. The amount an option’s premium changes when the price of the underlying asset changes is called the option’s delta.

Determinants of Option Value • The strike price The value of a call falls (the value of a put rises) as the strike price rises, all other things equal.

Determinants of Option Value • Time to expiration The value of both puts and calls rises as the time to expiration increases, all other things equal. The amount an option’s premium changes when its time to maturity changes is called the option’s theta.

Determinants of Option Value • Volatility The volatility of the underlying asset is a measure of how uncertain we are about future changes in an asset’s value. The more volatility increases, other things equal, the greater the chance that an option will do very well. The value of both puts and calls rises as the volatility of the underlying asset increases.

Determinants of Option Value • The risk-free rate of interest The value of a call rises (the value of a put falls) when the risk-free interest rate rises.

The Black-Scholes Formula The Black-Scholes pricing formula for a “plain vanilla” call option when the stock price is S, the strike price is X, the risk-free rate is r per annum and the time to expiration is t years is: N(*) is the cumulative standard normal distribution evaluated at *, and

The Black-Scholes Formula d1 and d2 are functions of the stock price, the strike price, the interest rate, time and volatility: compare

Example TelMex Jul 45 143 CB 23/8 -5/16 472,703

Assignment • Option Price Calculator • Ito’s Dilemma (A) • Ito’s Dilemma (B)