Download

1 / 21

220 likes | 428 Views

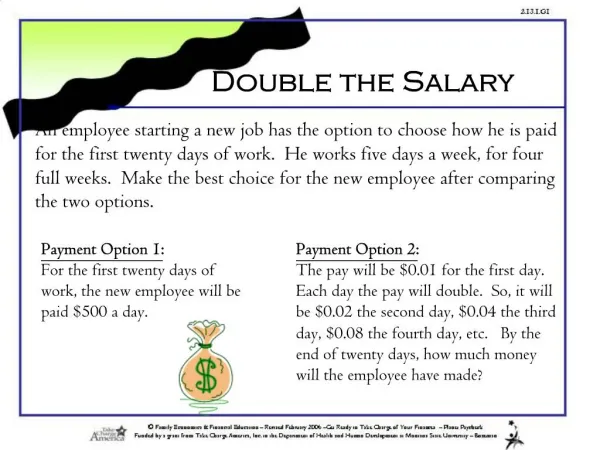

DI Can Protect Your Client’s Paycheck — and Increase Yours Disability Insurance Call Series. Presented By:. David Berdow, Corporate Financial Services Keith Hoffman, NFP Kat Freeman, NFP. Agenda. Disability Insurance Awareness Month Campaign

E N D

DI Can Protect Your Client’s Paycheck — and Increase YoursDisability Insurance Call Series Presented By: David Berdow, Corporate Financial Services Keith Hoffman, NFP Kat Freeman, NFP

Agenda • Disability Insurance Awareness Month Campaign • Why is part of your Due Diligence to discuss DI with your clients? • Common Misconceptions on Disability Coverage • Advantages of Selling DI • How to Sell DI • Case Study: David Berdow • NFP DI Resources

Creating a solid financial foundation Don’t miss the opportunity to help them protect their most valuable asset. Are your clients protected in the event of a disabling injury or illness?

Don’t Let These Misconceptions Stop You from Getting Your Client the Proper Coverage

#2 “I don’t need it – I don’t work in a dangerous profession.”

#3 “The government provides assistance when people get disabled.” • Less than half - 35% - of the 2.8 million workers who applied for Social Security Disability Insurance (SSDI) benefits in 2009 were approved.- Social Security Online, disabled worker beneficiary statistics, ssa.gov • Pays Benefits for Total disability only: severely impaired, physically or mentally, can’t perform any substantial gainful work and must last 12 months or result in death.

#4 “I have disability coverage at work.” Group LTD Considerations: • Taxability of Employer paid benefit • Salary Only- Bonuses and incentive pay typically not covered • Reverse discrimination for key employees (cap on benefits may be too low for higher-paid employees) • Benefit provisions within the policy are typically conservative • Policy is usually not portable for the employee • Individual DI Insurance Benefits: • Premiums and benefits are guaranteed through age 65. • Tax-free benefits (when paid with after-tax dollars) • Quality benefit provisions • Bonuses and incentive pay can be covered • Policy and discounts are portable • Payment options available (employer-paid or employee-paid)

DI Affordability Premiums typically cost 1% to 3% of gross income for a benefit that could pay out millions of dollars in the event of a disability. ’s affordable too – sample premiums Assumptions: 5A Occupation Class, To Age 65 Benefit Period and Your Occupation Period, 180 day Elimination Period, $1,000/monthly benefit, 10% Select Occupation Discount, Residual Disability and Recovery Benefit rider, Colorado resident, non-smoker. * Based on unisex rates. 20% Multi-life Discount given if three or more lives with a common employer participate. Getting a discount couldn’t be easier!

Advantages of DI: • Income. Brokers who sell disability insurance enjoy generous commission rates, up to 70%. That means if you sell two "professional" cases each month at $4,500, your annual income could be $75,600 or $891,000 over a 10-year period. And with the highest renewal rate in the industry - between 5% and 15% - those commission dollars really add up. • Declining Health Commissions. With healthcare reform, many employee benefit producers are facing commission cuts. Unless you're prepared for a lifestyle adjustment, it's a good idea to start augmenting your income stream! • Easy Underwriting. Selling disability insurance is easier than it used to be with many guaranteed standard issue (GSI) and simplified underwriting options. In many cases, there's no medical underwriting involved. • Differentiation.By becoming a disability insurance expert, you can differentiate yourself from other brokers and establish yourself as a convenient one-stop resource. • Support. Don't believe the myth that disability insurance is too complicated. With our support and the support of our carrier partners, you'll be comfortable with DI in no time at all!

Tips on How to Sell DI Say “Paycheck Protection.” Don’t tell me what it is. Tell me what it does! Most people cannot envision being disabled but they can understand the importance of protecting the paycheck – their most important asset. Change your client’s perspective by using one key phrase - paycheck protection. Sell the Need for Disability Insurance with Stats. The likelihood of being disabled during your working life is much more common than you would think. Use statistics to emphasize the likelihood of being disabled when meeting with clients. If they understand the need, they'll be more likely to buy. Sell Disability Insurance to Business Owners. There are many good candidates for DI, but business owners need the most protection. Protect business owners’ paychecks with individual disability insurance along with a Business Overhead Expense (BOE) policy to protect the business. Only 5 percent of business owners have a Business Overhead Expense policy. Sell Multi-Life Cases. Sell three or more lives from the same workplace or organization, and your clients will receive major paycheck protection discounts. Females can save up to 45% on their annual premiums! Why sell one disability insurance case if it’s better to sell three? Overcome Price Objections: Compare the Cost of DI to Home and Auto Insurance…or a cup of coffee! BUT MOST IMPORTANTLY…..

The secret to selling Disability Insurance… You need to ask.

David Berdow, CFPFinancial PlannerCorporate Financial Services

Voluntary Simplified Multi-Life Case Success Story Compensation1 $3,831.55First Year Commission $1,277 Renewal Commission $2,874 Quality Business Bonus (years 2-10) $4,789 (Over 20 years) • Background: Cold call on janitorial company, learned they were currently experiencing a claim issue under their LTD plan and dissatisfied with the LTD plan’s definition of Total Disability • Solution: Voluntary Simplified DI (with Multi-Life Discount) for the Executives • Results: • 14 Eligibles offered coverage • 43% participation among eligible employee group • $6,385.92 in annualized premium • Renewals currently at 5% but once at $5k of First Year Commission, renewals will be at 10% • Ongoing relationship with employer to potentially enroll more lives • Opened door to other revenue opportunities from the client 1 - Series 700 compensation, persistency, 50% FYCs and no annual coverage increases, renewals based on 10 year projection.

NFP DI Capabilities & Resources • Multi Life DI Sales Center • Customizable Marketing Material • Income Analysis Tools • Request for Proposal System • Uconnect for DI • Impaired Risk Outlet • High Limit DI Outlet • Existing Coverage Reviews • Underwriting Advocacy • Claims Expertise • Point of Sale Assistance • Carrier and Product Information • Training & Education • NFP DI Partnerships