Download

1 / 14

160 likes | 285 Views

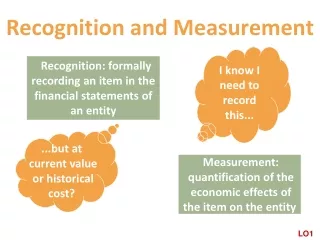

Recognition and Measurement Issues. Introduction. Off balance sheet -Issue on true and fair view. Does it refer to numbers in balance sheet only or balance sheet together with the notes? See Case study, pg 257- 261. Research and development.

E N D

Introduction • Off balance sheet -Issue on true and fair view. • Does it refer to numbers in balance sheet only or balance sheet together with the notes? • See Case study, pg 257- 261.

Research and development • R & D expenditure – raise issue on disclosure, recognition and measurement. Quality vs. quantity? • Research-original and planned investigation for gaining new scientific knowledge. • Development- application of research findings into a plan or design for the production of new improved material, products, processes, systems etc.

Recognition • R & D- how to recognize it? 2 methods: • a) Prudence concept- an immediate write-off • b) Matching- costs is carried forward where there is reasonable future benefit. • General rule-R & D should be recognized as an expense in the period in which they are incurred. IAS 38 allows matching principle. • IAS-research cost is recognized as an expense, not deferred. • IAS-development cost-can be deferred and recognized as an intangible asset and amortized on straight line basis by the extent of future benefit.

Conditions for R&D as an asset: • The technical feasibility of the product or process can be demonstrated. • The entity intends to market or produce the products. • The ability to use/sell the intangible asset. • How intangible asset can generate future economic benefits. • The adequate technical, financial and other sources. • Ability to measure the expenditure to intangible assets.

Measurement • R & D cost- raise issue on measurement of its cost and the amortization. • It is argued that R& D cost can be recorded as capitalized assets and amortized rather than expensed as they occur. ( FASB-SFA No 86) • Based on technological feasibility test • However, there is a problem of subjectivity in the capitalization of asset.

Measurement • Hooks (1995)- suggests how to measure for R& D cost; • a) Both R & D cost are expensed in the period in which they are incurred. • b) Some costs are expensed and some are capitalized – i.e. selective capitalization. • Expense R&D – based on matching current expenses with future benefits of the research. • Capitalized R&D- if they meet recognition criteria, carried forward and amortized on a systematic basis.

Contingencies • Contingency- a condition of existing at balance date which may give rise to loss or gain at later date. • Contingent assets- an asset that arises from past events and whose existence can only be confirmed by the occurrence or non occurrence of uncertain future events which are not within the control of enterprise. Eg. Law suit • That asset should not be recognized but can be disclosed if there is economic benefits.

Contingencies • Contingent liabilities –obligation that arise from past events and whose existence can only be confirmed by the occurrence or non occurrence of uncertain future events which are not within the control of enterprise. • A present obligation that arise from past events is not recognized because: IAS 37 • a) it is not probable that an outflow of resources with economic benefits, will be required to settle the obligation. • b) the obligation cannot be measured with reliability.

Contingencies • Contingencies should be disclosed when it is probable that cost or benefits to or from organization in the future and the benefit or obligation cannot be measured reliably. • If there is a loss, the loss should be accrued immediately in Fin. Statement as recognition criteria is met.

Investment and properties for resale • Issue of recognition and measurement in properties and investment intended for resale. Either for: • IAS 2- intended for sale-realized in the normal business. • IAS 16-property owner occupied • IAS 16 and 40- investment properties for capital growth and rental income. • IAS 16- as for development property

Property • Intended For sale- recognized as an ASSET when there is probable future benefit and cost of asset can be measured. • Measured as lower of cost or NRV. • Owner occupied – recognized as an ASSET • when there is probable future benefit and cost of asset can be measured. • Use fair value or market value.

Investment and development property • IAS 40- investment property may use the fair value or cost model. Gain or loss should be included in net profit or loss for the relevant period. • There are various accounting treatment for measuring and recording Value of Investment Property: • i.e. at fair value, at cost, for gain and loss either in P& L a/c or Inv. Prop. revaluation reserve. • Property for sale- record at net current value unless its NRV is lower. The write down value to P& L a/c. • The inclusion of unrealized gain on Inv. Prop in P& L a/c breaches the concept of prudence and conservatism. It is relevant or reliability?

Conclusion • Distinguishing between research costs and development costs is the main recognition problem for R & D. • Contingencies are noted in the report but the quality of information is insufficient and also uncertain. ( NZ Co. avoid environmental contingency due to reliability issue). • Property investment has less problem of recognition- but issue raise on the use of net current value vs. historical cost and realized gain & losses. • Raise the dilemma in reliability and relevance issue.