Download

1 / 21

420 likes | 1.02k Views

Mexican Peso Crisis. Mandi, Govinda & Jasmine. Inflation Foreign investments Central banks had $billions in reserves NAFTA took effect early 1994. Blue Skies. Mexican economy seemed healthy in early 90s…. What happened?.

E N D

Mexican Peso Crisis Mandi, Govinda & Jasmine

Inflation Foreign investments Central banks had $billions in reserves NAFTA took effect early 1994 Blue Skies Mexican economy seemed healthy in early 90s…. What happened?

Current account deficit peso becoming overvalued exports , imports foreign reserves being depleted A fall in domestic savings and a rise in domestic consumption contributed to the current account deficit http://www.galbithink.org/topics/mex/cad.htm http://www.galbithink.org/topics/mex/invest.htm Current Account Deficit Current account = balance of trade + net factor income (interest, dividends) + net transfer payments (foreign aid)

R = Real exchange rate P = Domestic price level (pesos) P* = Foreign price level ($) E = Mkt exchange rate (peso/$) %ΔP = domestic inflation rate %ΔP* = foreign inflation rate R = P/(P*E) In Mexico’s case: R because %ΔP > %ΔP* + %ΔE Real Appreciation & Overvalued Peso Due to policy reforms and NAFTA, a lot of capital ($102 billion from 1990-1994) (1) was flowing into Mexico making the peso appreciate in value. The Mexican government kept the value of the peso within a crawling peg exchange rate with the USD. The exchange rate was controlled within a narrow target band whose upper limit was raised bit by bit for gradual nominal depreciation. But in real, price adjusted terms the peso was appreciating, contributing to the current account deficit %ΔR = %ΔP - %ΔP* - %ΔE Thus the peso became overvalued, meaning the exchange rate became too high for a sustainable equilibrium in the balance of payments. Higher interest rates (which causes external debt to rise even more) are needed to prop up an overvalued currency until the inevitable devaluation takes place.

From Problem to Crisis Rise in U.S. interest rates Elections Shift from cetes tesobonos Political Shocks

Elections • Because of an upcoming presidential election on August 21, 1994, • Mexican authorities were reluctant to take action in the spring and summer of 1994 to fix the inconsistencies in the economy. The choices open to them were to: • raise interest rates even more to bring back capital inflow • reduce government expenditures to reduce domestic demand, decrease imports and relieve pressure on the peso • devalue the peso to make exports more competitive The first two options were unattractive in a presidential election year because they could have led to a significant downturn in economic activity and could have further weakened Mexico’s banking system. (PRI wanted to stay in charge). Devaluing the peso would have undermined its commitment to maintaining a stable exchange rate – the basis of its success in attracting foreign capital.

http://www.galbithink.org/topics/mex/uint.htm Rise in U.S. interest rates In February 1994, the Federal Reserve raised its federal funds rate target because of inflationary pressures. The Mexican government thought it was only temporary and made no substantial policy changes.

The Central Bank blamed a series of assassinations and other discouraging acts that political risk and investor confidence.(2) March 1994 Assassination of presidential candidate Luis Donaldo Colosio Reserves $11 billion in four weeks June/July 1994 Resignation of Minister of the Interior Jorge Carpizo who was overseeing the national election, kidnapping of prominent businessman Alfredo Harp Reserves $2.5 billion in three weeks September 1994 Assassination of High official Jose Francisco Ruiz Massieu Reserves $4 billion December 1994 Renewed pressure on the peso: Breakdown in talks with Chiapas rebels? Market worries about current account deficit? Leaked rumors of changes in exchange rate policies? Reserves $1.5 billion in three days Political Shocks

http://www.galbithink.org/topics/mex/pbond.htm Shift from cetes tesobonos Banco de México had tried increasing domestic interest rates (from 10.1 % to 17.8% in March) on short-term (91-day), peso-denominated Mexican government bonds (cetes) in an attempt to stem the outflow of capital. Didn’t work. Investors too scared of an upcoming devaluation. In response to these investor concerns, the Mexican government issued large amounts of short-term, dollar-denominated bonds (tesobonos). Now any devaluation would be the government’s problem. Super vulnerable to a financial market crisis; its foreign exchange reserves had fallen to $12.9 billion,18 while it had tesobono obligations of $28.7 billion maturing in 1995.19. (1)

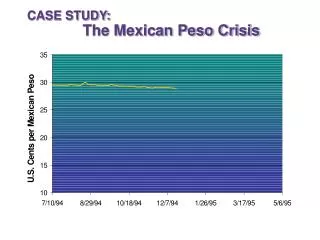

December 20-21 – The government did not announce any new fiscal or monetary measures to accompany the devaluation so foreign reserves $4 billion. Float and Sink December 20 – Mexican authorities sought to relieve pressure on the exchange rate by announcing a widening of the peso/dollar exchange rate band (peso devalued by 15%.) December 22 – Mexican government forced to freely float its currency. The Mexican Peso Crisis of 1994-95 was now full-blown, and at this point, Mexico was forced to turn to international sources for assistance.

International Effects Due to the Mexican Peso Crisis most large Western hemisphere Less Developed Countries (LDCs) experienced turbulence in their foreign exchange markets and significant declines in equity markets. For example Argentina and Brazil experienced heavy trading losses after the Crisis. Some of the LDCs experienced discrimination due to the fact that they had some of the same general characteristics as Mexico: 1. low savings rates 2. large current account deficits 3. weak banking systems 4. significant volumes of short term debt

Solving the Mexican Peso Crisis • Due to the magnitude of the Peso Crisis, the United States and the IMF concluded that outside assistance was required to prevent Mexico’s financial collapse as well as to prevent the spread of the crisis to other LDCs. • United States Assistance • $48.8 billion multilateral assistance package • This package offered $20 billion to Mexico through the use of the Exchange Stabilization Facility • IMF Assistance • 18-month standby arrangement for up to $17.8 billion • Other Assistance • Other countries offered assistance in the form of $ 10 billion under the Bank of International Settlements *NOTE: The response to the Peso Crisis was one of the largest multilateral economic assistance packages ever extended to one country.

Goals of Assistance • Restore financial stability • Strengthen public finances and the banking sector • Regain investor confidence • Reinforce the groundwork for long-term sustainable growth

Assistance From the United States in Detail • Three Mechanisms: • Short-term currency swaps for up to 90 days, with renewals for a maximum term of 1 year for Treasury swaps and renewals up to three times for the Fed swaps • Medium-term currency swaps for up to 5 years • Securities guarantees under which ESF funds could be used to back up securities issued by the Mexican gov’t for up to 10 years

Ways to Respond to a Current Account Deficit • 1. Attract more foreign capital • 2. Allow currency to depreciate • This makes imports more expensive and exports cheaper • 3. Tightening monetary/fiscal policy to reduce the demand for all goods • 4. Using foreign exchange reserves to cover deficit

Post-Crisis • Economic Recovery (1996-1999) • Sounder macroeconomic decisions/practices • Improvement of trade balance • Increase in private consumption Post Crisis Trade Balance (1996-Present)

Post-Crisis • Investor confidence has been increasing • Economic growth slowly continues GDP Growth Post-Crisis (1995-Present) Gross Investment Growth Post-Crisis (1995-Present)

Post-Crisis Effects • Lingering Side-Effects? • Improvement in Mexican banking • Youth of Banking sector • Improvement of regulations • Distribution of Wealth • Large gap between the rich and poor remains • Financial Institutions • IMF double Emergency Funds

Post-Crisis Effects (cont.) • Signs of emergence from Crisis • Relatively Low Interest Rates • Around 8.5% as of 2006 • Low Inflation Rates • 3.3% in 2005

An Expensive Lesson • What can we learn from the crisis? • An improvement of economic fundamentals • Increased transparency of economies • IMF periodic economic and financial publications by each member nation • Realization of the speed of capital mobility

(1) Arner, Douglas. “The Mexican Peso Crisis: Implications for the Regulation of Financial Markets.” Essays in International Financial & Economic Law. The London Institute of International Banking, Finance & Development Law, 1996. <http://iibf.law.smu.edu/arner.pdf> (2) Williamson, John. “Causes and Consequences of the Mexican Peso Crisis.” Institute for International Economics March 14, 1995 http://www.galbithink.org/topics/mex/ps.htm#elections