Download

1 / 4

40 likes | 318 Views

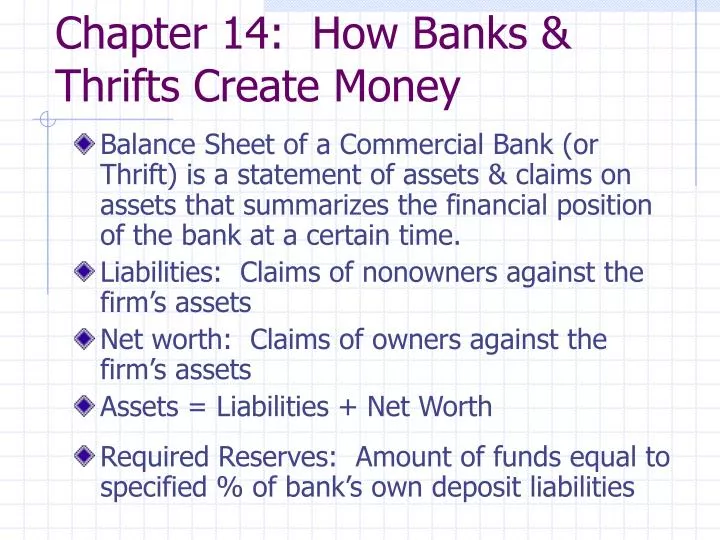

Chapter 14: How Banks & Thrifts Create Money. Balance Sheet of a Commercial Bank (or Thrift) is a statement of assets & claims on assets that summarizes the financial position of the bank at a certain time. Liabilities: Claims of nonowners against the firm’s assets

E N D

Chapter 14: How Banks & Thrifts Create Money • Balance Sheet of a Commercial Bank (or Thrift) is a statement of assets & claims on assets that summarizes the financial position of the bank at a certain time. • Liabilities: Claims of nonowners against the firm’s assets • Net worth: Claims of owners against the firm’s assets • Assets = Liabilities + Net Worth • Required Reserves: Amount of funds equal to specified % of bank’s own deposit liabilities

Profits & Liquidity • The asset items on a commercial bank’s balance sheet reflect the banker’s pursuit of two conflicting goals: • Profit • Why bank makes loans & buys securities 2 major earning assets of commercial banks • Liquidity • Safety in cash & excess reserves • Compromise between assets that earn higher returns & high liquidity that earn no returns

Federal Funds Market • Banks can reconcile goals of profit & liquidity by lending temporary excess reserves held at Federal Reserve Banks to other banks • Excess reserves are lent on an overnight basis as way of earning additional interest w/o sacrificing long-term liquidity • Federal Funds Market: market for immediately available reserve balances at the Federal Reserve • Federal Funds Rate: Interest rate paid on overnight loans

Last Word: The Bank Panics of 1930 - 1933 • Bank panics in 1930 – 1933 led to contraction of money supply, worsening Depression • Many failed banks were healthy, but suffered as worried depositors panicked & withdrew funds all at once • Reserves & lending power fell • Roosevelt declared “bank holiday” closing banks temporarily while Congress started the Federal Deposit Insurance Corporation (FDIC), ending bank panics on insured accounts

![ECN 135 Lecture [M] Chapter 23 Money, Banks Financial Institutions](https://cdn4.slideserve.com/1148654/slide1-dt.jpg)

![How Banks Create Money [ MS ] MS = Currency + DD of Public](https://cdn1.slideserve.com/2752152/slide1-dt.jpg)