Download

1 / 25

280 likes | 537 Views

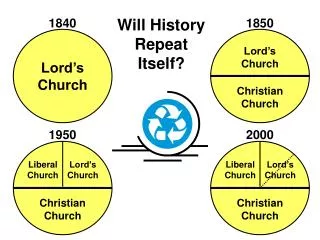

Will History Repeat Itself?. An Assessment of Turkish Current Account Trends and Prospects. Cevdet Akçay & Murat Üçer December 2, 2005. Outline. Why we worry at all, and a few facts and propositions on the current account

E N D

Will History Repeat Itself? An Assessment of Turkish Current Account Trends and Prospects Cevdet Akçay & Murat Üçer December 2, 2005

Outline • Why we worry at all, and a few facts and propositions on the current account • Speculations on the future, taking history and convergence as reference • Some empirical observations • Conclusions: Don’t worry be happy?

…and because of conventional wisdom “What are sustainable rates of real appreciation or of current account deficits and what invites a crisis? ...it is safe to say that a rapid real appreciation – say over 2 or 3 years – amounting to 25 percent or more, and an increase in the current account deficit that exceeds 4 percent of GDP, without the prospect of a correction, takes a country into the red zone” Excerpt from “A Primer on Emerging Market Crises” R. Dornbush, June 2001

Current account deficit will likely continue this way in the near term; financing composition and prospects are improving, but still mostly debt and unidentified inflows…

Basic sustainability arithmetic: Non-Interest Current Account Balance + Non Debt Creating Flows > (Real Foreign Interest Rate – Real Appreciation – Real Growth Rate) X Initial Net Debt Ratio Assumptions: NICA = -5% NDCF = 2.5% Interest rate = 4% Real growth = 5% Real appreciation = 0% Initial net debt ratio = 30% But sustainable only under fairly benign assumptions while decline in “measured” debt reflects temporary factors, measurement issues, and real exchange rate appreciation

The widening in the deficit was driven by investment, and the corporate sector; good news, with caveats…

And given the international backdrop, policy response could have been hardly different…

Speculations on the future, taking history and convergence as reference… • How does the latest boom compare to history? • How does Turkey compare to convergence economies when they started the chapter-by-chapter negotiations?

We have conducted two empirical exercises • Searched for the Balassa-Samuelson effect in the data • Looked at the sort-run determinants of the current account in a vector autoregression setup

On the Balassa-Samuelson (B-S) Effect • Trade integration → higher productivity increases in the traded goods sector (TG S) → higher wages → (under the assumptions of full employment and perfect labor mobility across sectors) → higher wages in the non-traded goods sector (NGS) → No matching productivity increase in NGS → profitability concerns push up PNGS → CPI ↑ while (PTGS/PNG) ↓ → Real Exchange Rate (RER) appreciation given that the counter-party productivity differential is smaller. • ПNGS = ПTGS (common to all trading partners) + the rate of depreciation (provided that the exchange rate is not constant) + a productivity differential measure reflecting the asymmetry of the productivity gains between the home country and the trading partners. • Periods of prolonged appreciation due to periods of persistent productivity differentials OR periods of real exchange rate disequilibria?

Regression Output: Real Exchange Rate and Productivity Differential

RER Regression Inferences • The sum of the current and lagged productivity ratio coefficients is 0.746, thus over the long run a 1% Δ change in the productivity differential → a 0.746% Δ in the RER. • For the whole sample period (1990Q1 through 2005Q2), the Δ in productivity differential is 30.7%, and the change in RER is 42.6%, implying that 53.8% of the Δ in the RER can be attributed to the Δ in productivity differential. • The residual series from this regression is taken as an RER series that is cleared from effects of relative productivity changes, and thus encompasses all other drivers of the real exchange rate except for the productivity differential variable. • The purpose is to gain insight into the impact of RER Δs on the current account deficit in the absence and in the presence of a Balassa-Samuelson effect.

On the Short Run Determinants of the Current Account • In the VAR framework, we included capital inflows, the real exchange rate(actual in one version and the residual in the other), output growth, and current account balance as endogenous variables. • To the extent that a significant portion of the RER variation comes from factors other than BS, coefficients of the actual and the residual RER series should be roughly similar in the current account equations. • Better use of VAR models are made through variance decompositions and impulse responses. We utilize both methods to gain insight into current account dynamics in general, and the role of real exchange rate in particular.

On the Short Run Determinants of the Current Account • Coefficients of the actual and the residual RER series did come out to be similar, implying that a significant portion of the real exchange rate variation could be attributed to factors other than BS. • For both set ups, variance decompositions clearly show that the current account is mostly a capital account driven phenomenon. • To the extent that the real exchange rate has any impact on the current account balance, roughly half of that stems from that portion of the change in the real exchange rate that is not linked to productivity differentials. • Impulse response functions also indicate that capital inflow shocks and shocks to both versions of the RER variable have an impact on the current account, the order reflecting the strength of impact very much in the spirit of variance decomposition inferences.

Conclusions • Turkey now is very similar to the convergence economies then; plus we detect some encouraging differences from earlier boom episodes, in addition to flexible exchange rate and a stronger banking sector. • Yet, we are still in transition. • Our VAR exercise confirms a history of mainly capital account-driven current account adjustments, which typically entailed a “correction” in the real exchange rate. • The B-S regressions suggest some overvaluation in this latest episode as well. • But an “old-style reversal” seems highly unlikely as long as EU momentum is maintained, international environment remains benign, and strong fiscal policy is supported by structural reforms.