Download

1 / 0

0 likes | 193 Views

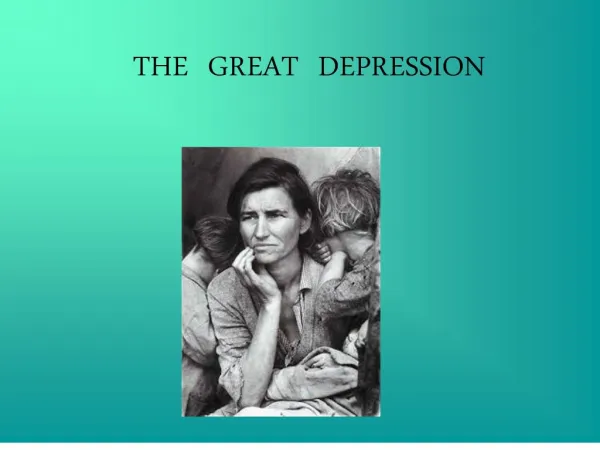

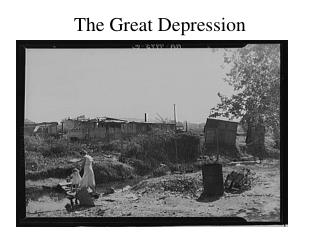

The Great Depression. Topic 12 Economics 2333 Robert A. Margo Spring 2013. Agenda. Background material Finegan and Margo Fishback , Horace, and Kantor Richardson and Troost. The Great Depression. Great Depression: Key macroeconomic e vent of the 20 th Century

E N D