Download

1 / 12

130 likes | 302 Views

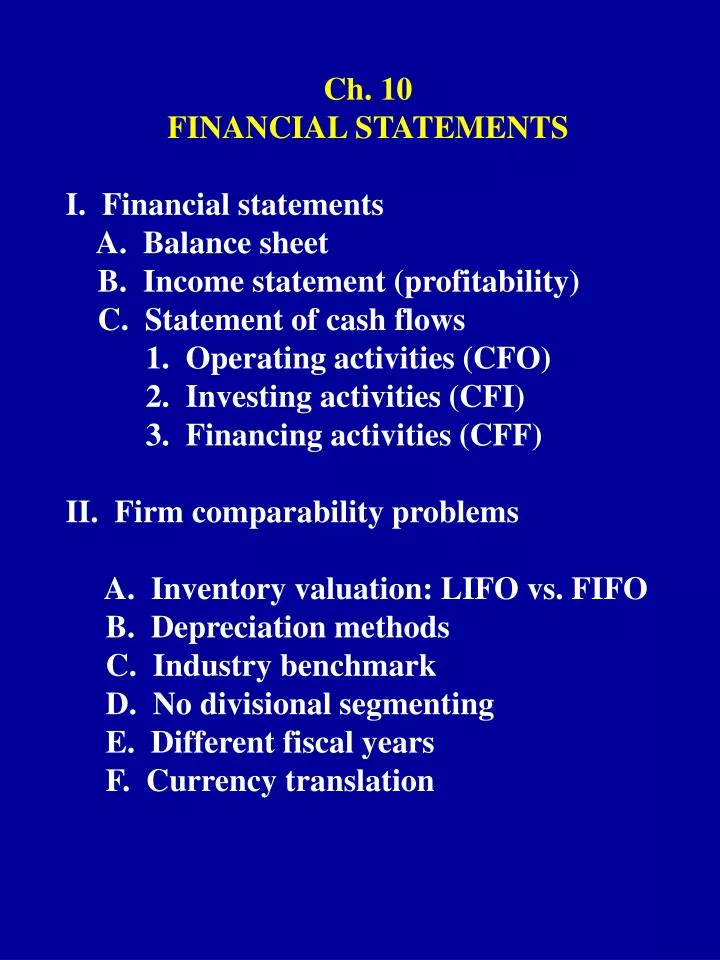

Ch. 10 FINANCIAL STATEMENTS I. Financial statements A. Balance sheet B. Income statement (profitability) C. Statement of cash flows 1. Operating activities (CFO) 2. Investing activities (CFI) 3. Financing activities (CFF) II. Firm comparability problems

E N D

Ch. 10 FINANCIAL STATEMENTS I. Financial statements A. Balance sheet B. Income statement (profitability) C. Statement of cash flows 1. Operating activities (CFO) 2. Investing activities (CFI) 3. Financing activities (CFF) II. Firm comparability problems A. Inventory valuation: LIFO vs. FIFO B. Depreciation methods C. Industry benchmark D. No divisional segmenting E. Different fiscal years F. Currency translation

QUALITY OF EPS I. Reported EPS A. Core (Primary) B. Diluted II. Non-operating/non-recurring items III. Differential disclosure A. Annual reports B. SEC filings 1. 10-K 2. 10-Q IV. Changes in discretionary expenses A. Earnings smoothing

FINANCIAL STATEMENT ANALYSIS I. Purpose A. Evaluate historical performance B. Help predict future course of firm II. Primary users A. Investors B. Creditors C. Internal management

FINANCIAL RATIO ANALYSIS I. Evaluate relative performance A. Economy B. Competitors (cross-sectional analysis) C. Industry standards D. Comparisons 1. Horizontal analysis (trend analysis) 2. Vertical analysis (common size) II. Limitations: A. Calculated from historical data B. Only one evaluation tool C. Direct industry comparison difficult D. Ratio calculations not standardized

FINANCIAL RATIOS I. Categories A. Liquidity: Pay bills on time? B. Operating: Assets utilization? C. Profitability: Earnings potential? D. Risk (leverage) 1. Business: Operating income risk? 2. Financial: Repay creditors? E. Cash flow: Financially healthy? F. Market value: Relative valuation?

LIQUIDITY RATIOS • I. Current ratio = • current assets (CA)/current liabilities (CL) • II. Quick ratio = acid test ratio = • (CA - inventories)/CL • Days sales outstanding (DSO)= • avg. accounts receivables/(sales/365) • IV. Days of inventory processing (DIP)= • avg. inventory/(CGS/365) • V. Days to payables payment (DPP)= • avg. accounts payable/(CGS/365) • VI. Cash conversion cycle = • DSO + DIP - DPP

OPERATING RATIOS I. Asset turnover = investment turnover A. Total asset turnover (TATO) = sales/avg. total assets B. Fixed asset turnover = sales/ avg. fixed assets C. Accounts receivable turnover = sales / avg. accounts receivable D. Inventory turnover = CGS/ avg. inventory

PROFITABILITY RATIOS I. Gross profit margin = gross profit/sales II. Operating profit margin (OPM) = EBITDA*/sales * earnings before int., taxes, depr. & amort. III. Net profit margin (NPM) = net income/sales IV. Operating return on assets = EBITDA/avg. total assets V. Return on assets (ROA) = net income/avg. total assets VI. Return on equity (ROE) = net income / avg. equity

DuPONT SYSTEMS OF ROE COMPONENTS I. DuPont analysis decomposition of ROE = NPM*TATO*Finl. leverage multiplier (FLM) where FLM = (avg. total assets/avg. equity) A. Sustainable growth: ROE * retention ratio (B) = R * B II. Extended DuPont System A. Negative effects of financial leverage 1. Interest expense rate (IER) = Interest exp./ avg. total assets B. Positive effects of financial leverage 1. Tax retention rate (TRR) = [1 - (Income tax expense/pretax income)] ROE = NPM*TATO*FLM*IER*TRR

FINANCIAL LEVERAGE RATIOS • I. Long-term debt/common equity • II. Long-term debt/long term capital • III. Total debt/total capital = ??? • Interest coverage = TIE • (EBIT - int. exp.) /int. exp. • V. Fixed charge coverage = • (EBIT - int. exp - lease exp.) / • (int. exp. + lease exp.)

CASH FLOW RATIOS I. Cash flow (CFO) /interest expense = II. Cash flow coverage = (CFO – (interest exp. + lease exp.)) / (int. exp. + lease exp.) III. Cash flow/ long-term debt = CFO/ (BV of long-term debt + PV of leases) IV. CFO / total debt V. Free cash flow = CFO - cap. exp. - dividends

VALUATION RATIOS I. Relative models A. Price/earnings multiplier (P/E): = P0/E1 1. Problems with multiplier models a. EPS0 vs. EPS1 b. Useless if firm loses $ c. Ignores TVM B. Market price-to-book value (P/B) 1. Problems using book value a. Inflation not considered b. Function of reporting choice C. Dividend yield = D1 / P0