Download

1 / 18

180 likes | 385 Views

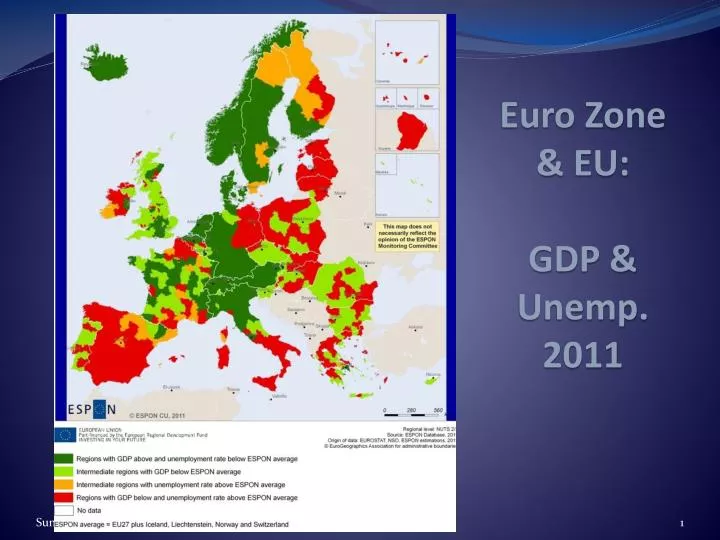

Euro Z one & EU: GDP & Unemp . 2011. Euro- Austerity : 1. Euro- Austerity: 2. www.imf.org/external/pubs/ft/weo/2013/01/index.htm. Euro- Austerity: 3. IMF World Economic Outlook and IMF Fiscal Monitor, Oct. 2012. Inflation Convergence , EMS. Goals of Euro- Zone. Krugman et. al. (2012):

E N D

Euro- Austerity: 2 www.imf.org/external/pubs/ft/weo/2013/01/index.htm

Euro- Austerity: 3 IMF World Economic Outlook and IMF Fiscal Monitor, Oct. 2012

Goals of Euro-Zone • Krugman et. al. (2012): • Unified market: the belief that greater market integration and economic growth would occur. • Political stability: the belief that a common currency would make political interests more uniform. • The belief thatGerman influence under the EMS would be moderated under a European System of Central Banks. • Elimination of the possibility of devaluations/ revaluations: with free flows of financial assets, capital flight and speculation could occur in an EMS with separate currencies, but it would be more difficult for them to occur in an EMS with a single currency.

Theory of OptimumCurrencyArea • Joining fixed exchange rate system would be beneficial for a country if • trade is extensive between it and member countries, because transaction costs would be greatly reduced. • financial assets flow freely between it and member countries, because the uncertainty about rates of return would be greatly reduced. • people migrate freely between it and member countries, because the uncertainty about the purchasing power of wages would be greatly reduced.

Theory of OptimumCurrencyArea • After joining a fixed exchange rate system, economic integration losses not so great from country’s own fall in aggregate demand, if integration greater, since • Relative prices will tend to fall, which will lead other members to increase aggregate demand greatly if economic integration is extensive. • Financial assets and labor will migrate to areas with higher returns or wages if economic integration is extensive, so that the economic loss is not as great. • Therefore, the loss of the automatic adjustment of flexible exchange rates is not as great if goods and services markets are integrated.

US much more integrated • Most EU members export from 10% to 20% of GDP to other EU members • US exports 14% of GDP to rest of the world (World Bank, 2011).

Little ∆ in Intra-Euro Trade Krugman et. al, Fig. 20-7

Conclusion: EurozonenotanOptimalCurrencyArea • Trade Integration in US ≈ 2 x Greater • Labor Mobility in US > 3 x Greater • Financial Integration is minimal due to lack of Euro-zone Bonds • Solution => Stronger European Governance

Barriers to FurtherIntegration: www.pewglobal.org/files/2013/05/Pew-Research-Center-Global-Attitudes-Project-European-Union-Report-FINAL-FOR-PRINT-May-13-2013.pdf

www.pewglobal.org/files/2013/05/Pew-Research-Center-Global-Attitudes-Project-European-Union-Report-FINAL-FOR-PRINT-May-13-2013.pdfwww.pewglobal.org/files/2013/05/Pew-Research-Center-Global-Attitudes-Project-European-Union-Report-FINAL-FOR-PRINT-May-13-2013.pdf

![2011 ITRS Emerging Research Materials [ERM] July 10-13, 2011](https://cdn2.slideserve.com/4220097/2011-itrs-emerging-research-materials-erm-july-10-13-2011-dt.jpg)