Download

1 / 23

230 likes | 339 Views

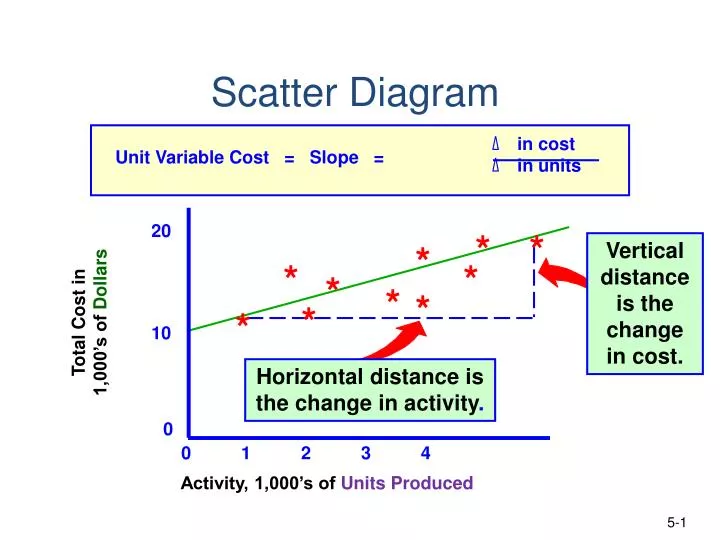

Δ in cost Δ in units. Unit Variable Cost = Slope =. 20. *. *. *. *. *. *. *. *. Total Cost in 1,000’s of Dollars. *. *. 10. 0. 0 1 2 3 4. Activity, 1,000’s of Units Produced. Scatter Diagram.

E N D

Δin costΔin units Unit Variable Cost = Slope = 20 * * * * * * * * Total Cost in1,000’s of Dollars * * 10 0 0 1 2 3 4 Activity, 1,000’s of Units Produced Scatter Diagram Vertical distance is the change in cost. Horizontal distance is the change in activity. 5-1

The High-Low Method The following relationships between units produced and costs are observed: Using these two levels of activity, compute: • the variable cost per unit. • the total fixed cost. 5-2

$8,500$50,000 Δin costΔin units • Unit variable cost = = = $0.17 /unit • Fixed cost = Total cost – Total variable cost Fixed cost = $29,000 – ($0.17 per unit × $67,500) Fixed cost = $29,000 – $11,475 = $17,525 The High-Low Method 5-3

Process Manufacturing Operations C1 • Used for production of small, identical, low-cost items. • Mass produced in automated continuous production process. • Costs cannot be directly traced to each unit of product. 3-4

Job Order Systems Custom orders Heterogeneous products Low production volume High product flexibility Low to medium standardization Process Systems Repetitive operations Homogeneous products High production volume Low product flexibility High standardization Comparing Job Order and Process Production A1 3-5

Sameobjective:to determine the cost of products Sameinventory accounts:raw materials, work in process, and finished goods Sameoverhead assignment method:predetermined rate times actual activity Job and Process Costing Similarities A1 3-6

The difference between job order and process costing lies in how the cost of goods transferred to finished goods is determined. Journal entries for both job order and process costing are the identical Job and Process Costing Similarities and Differences A1 3-7

Job Order and Process Costing Differences A1 Process costing The cost of goods transferred to finished goods equals the number of completed units times the cost per equivalent unit Job order costing The cost of goods transferred to finished goods is equal to the sum of all of the completed jobs for that period 3-8

+ = Equivalent Units of Production C2 Equivalent units is a concept expressing a number of partially completed units as a smaller number of fully completed units. Twoone-half full pitchers are equivalent to one full pitcher. 3-9

Equivalent Units C2 40% ofMaterial 60% ofMaterial Stage 1 Stage 2 Stage 3 25% ofLabor andOverhead 25% ofLabor andOverhead 50% ofLabor andOverhead The process is now complete. 3-10

Cost perequivalent unit Product costs for the periodEquivalent units for the period = Cost Per Equivalent Unit C2 3-11

FinishedGoods DeliveredtoCustomers Process Manufacturing Operations GenX C3 Direct Materials Indirect Goods in Process FactoryOverhead AllocatedOverhead Indirect Direct Labor 3-12

Accounting for GenX C3 3-13

Accounting for GenX C3 3-14

Accounting for GenX C3 GenX uses a weighted average cost flow system with the following steps: • Determine the physical flow of units. • Compute equivalent units of production. • Compute the cost per equivalent unit. • Assign and reconcile costs. 3-15

Determine Physical Flow of Units C3 3-16

Compute Equivalent Units of Production – Direct Labor and Factory Overhead C2 3-18

In the cost reconciliation, we willaccount for all costs incurredby assigning unit costs to the: • A. 100,000 units transferred out. • B. 20,000 units remaining in ending inventory. Cost Reconciliation C3 3-21

C3 3-22

C3 3-23