Download

1 / 54

540 likes | 679 Views

History, Status, and Implications of the Subprime Mortgage Market. A Presentation for The Fuqua School of Business at Duke University October 30, 2007. Doug Breeden, Mike Giarla, Pete Nolan, Tapas Panda, and B.J. Whisler. Agenda. Creation and Evolution of the Subprime Mortgage Market

E N D

History, Status, and Implications of the Subprime Mortgage Market A Presentation for The Fuqua School of Business at Duke UniversityOctober 30, 2007 Doug Breeden, Mike Giarla, Pete Nolan, Tapas Panda, and B.J. Whisler

Agenda • Creation and Evolution of the Subprime Mortgage Market • Subprime Impact on the Secondary Mortgage Market • Subprime Impact on Other Markets and the Broader Economy • Policy Issues and Implications

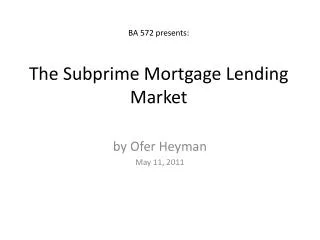

Subprime Mortgage Issuance Has Dominated ABS Supply in Recent Years

U.S. FICO score distribution Current composition of U.S. mortgage debt Subprime Mortgage Borrower Base Relative to General U.S. Population Source: MBA, Deutsche Bank Global Markets Research, Fair Isaac Corporation. Data as of: October 23, 2006. Note: All information is provided for informational purposes only and should not be deemed as a recommendation to buy or sell securities. This information is taken from sources that we deem reliable, but no warranty is made as to accuracy.

Subprime Mortgages Cover Many High Value Homes • Smith Breeden Analysis includes zip code level geographic detail loan data. • Cost of foreclosure is less than many might expect (due to large average loan size). • Homes liquidated will be attractive to a wide range of homeowners. • Losses, given foreclosure, should be contained. Subprime HPA Returns (Cumulative) Source: Smith Breeden Analytics. Data as of 1Q 2007.

Securitization Provides Opportunity for Investors of Various Risk Appetites AAA Principal Payments AA+ AA AA- A+ Subprime Loans (1000s) A A- BBB+ BBB losses BBB- 8% Subordination BB+ BB 2% overcollateralization Residual Source: Smith Breeden Analytics. Note: All information is provided for informational purposes only and should not be deemed as a recommendation to buy or sell securities.

Subprime ABS Yield Spreads Widened Dramatically in July and August

Causes of Recent Subprime Troubles • Deterioration of loan underwriting standards • Low margins, high demand (CDOs). • Variable rate resets • 2/28 and 3/27 loans. • Softening employment • Local economies an important factor in subprime default. • Slowdown in home price appreciation • Previously erased effects from other factors. This presentation is provided for informational purposes only and should not be deemed as a recommendation to buy or sell securities.

Opportunity Created by Subprime Woes • Systematic pricing of idiosyncratic markets • Liquidity providers to forced-sellers • Lack of necessary analytics in the investment community • Uncertain value This material has been prepared or is distributed solely for informational purposes only and is not a solicitation of offers to buy any security or instrument or to participate in any trading strategy. Past results are not necessarily indicative of future performance. No assurance can be made that profits will be achieved or that substantial losses will not be incurred. All investments involve risk including the loss of principal.

Agenda • Creation and Evolution of the Subprime Mortgage Market • Subprime Impact on the Secondary Mortgage Market • Subprime Impact on Other Markets and the Broader Economy • Policy Issues and Implications

Rating Agency Mass Downgrade Action • June 15th: Moody’s announced the first mass scale downgrade action (267 bonds). Since then, rating agency downgrades have been running at full steam.

Risk Repricing in Subprime MBS • Investors re-priced risk in subprime mortgage-backed bonds, leading to severe marked-to-market losses. • BSAM funds liquidation aggravated the death spiral: Two hedge funds of Bear Stearns Asset Management (BSAM) liquidated • High Grade Structured Credit Strategies Enhanced Leverage Fund • High Grade Structured Credit Strategies Fund

Liquidity Crunch • Liquidity crunch manifested in four market components A: LIBOR rates B: ABCP rates C: Jumbo rates D: Funding rates for levered players

Inter-bank Lending Suffers, LIBOR Spikes Source: Bloomberg

Asset Backed Commercial Paper Spreads Widen Source: Bloomberg

Unwinding of ABCP • Asset Backed Commercial Paper unwinds and ends up on liquidity provider’s balance sheet… Source: Bloomberg

Jumbo Mortgages Squeezed • … As originators faced with a liquidity crunch increased rates on Jumbo mortgages. Source: Bloomberg

Deleveraging of Portfolios • Funding became less attractive for levered players to carry non-agency products, leading to more deleveraging. Haircut and Funding Rates for Agency and Non-Agency Mortgages

Trading Volume Depressed • Trading volume shrunk, making price discovery difficult. Source: UBS

Non-Agency Hybrid Spreads Source: Morgan Stanley

Investment Advice “Be fearful when others are greedy and be greedy when others are fearful”

ABCP Unwinding and/or Revaluation • Citigroup, J.P. Morgan and Bank of America formation of super-conduit (Master Liquidity Enhancement Conduit) will impact spreads in the short term. • Rate reset will add pressure to the housing market until affordability improves. • Supply of non-agency to shrink and spreads to tighten on high-rated bonds in the long-term.

Subprime ARM Resets Pending • High volume of subprime resets over the next 18 – 24 months Source: PIMCO

Future Mortgage Market Composition • The mortgage market composition will change dramatically. Source: UBS

Agenda • Creation and Evolution of the Subprime Mortgage Market • Subprime Impact on the Secondary Mortgage Market • Subprime Impact on Other Markets and the Broader Economy • Policy Issues and Implications

Response in Corporate Bonds: Overall • General corporate bond spreads wider Data Sources: Moody’s Investors Service Long-Term Single-A Corporate Bond Yields; Bloomberg US Treasuries Indices

Response in Corporate Bonds: Financials • Financial institution bonds wider Data Source: Bloomberg

Housing Economics: Overview Increased Foreclosures Reduced Demand Rising Home Inventories Home Prices Decline Construction Declines Mid-term Impact on Employment Equilibrium Restored in time

Housing Economics: Supply and Demand Source: The Bank Credit Analyst, Volume 59, Number 4

Economics: Unemployment Rate • Recent increases in the unemployment rate Data Source: Bureau of Labor Statistics

Economics: Construction Payrolls • The brunt of the effect is in construction and manufacturing *2007 figures are through Q3 Data Source: Bureau of Labor Statistics

Economics: Consumption • Wealth-based spending source at risk Data Sources: Federal Reserve Estimates based on Bureau of Economic Analysis data

Economics: Global Response • Personal consumption represents 70% of US Gross Domestic Product. • US consumption represents 19% of global GDP. • Global economies arguably highly dependent on US consumer spending.

Agenda • Creation and Evolution of the Subprime Mortgage Market • Subprime Impact on the Secondary Mortgage Market • Subprime Impact on Other Markets and the Broader Economy • Policy Issues and Implications

Subprime “Pain” is Not Limited to Institutional Investors • Financial and psychological damage is being felt by individuals and families (and entire communities) as foreclosures mount. • Without major intervention, more than 1 million of the subprime loans (est. 20%) made in 2005 and 2006 are headed for foreclosure. • A disproportionate share of the pain is felt by minority borrowers.

Subprime “Woes” Disproportionately Affect Minorities “Higher Cost” 1st Lien Loans (2005 HMDA) Source: FFIEC. Data reported by Lenders Under the Home Mortgage Disclosure Act. See p. 23 of “Losing Ground: Foreclosures in the Subprime Market and Their Cost to Homeowners” – Center for Responsible Lending.

Even After Adjusting for Risk Factors, Minority Borrowers Are More Likely to Have a Subprime Loan • 2006 Study Found that African-American and Latino borrowers are at greater risk of receiving high-rate loans than white borrowers, even after controlling for legitimate risk factors. Source: “Unfair Lending: The Effect of Race and Ethnicity on the Price of Subprime Mortgages”, Center for Responsible Lending, May 31, 2006)

About The Center For Responsible Lending (“CRL”) • Non-profit, non-partisan research and policy organization dedicated to protecting homeownership and family wealth by working to eliminate abusive lending practices. • Affiliated with Self-Help, headquartered in Durham, one of the nation’s largest community development financial institutions. • Self-Help Credit Union • Self-Help Ventures Fund • Self-Help Community Development Corporation

Is Subprime = “Evil”? • All subprime loans are not inherently “bad” – only a subset will default. Subprime loans have helped many people achieve their dream of home ownership. • Not all subprime lenders are “scrupulous”. Unscrupulous lenders often hide behind “we help people realize their home ownership dreams” statement. • Unfortunately, predatory practices were common in the subprime lending business.

The Market Is Self Correcting, Right? • Normal market forces are not correcting problems. • Subprime mortgage market does not have adequate incentives to police itself. Example – economic incentives for subprime lenders to make harmful loans: • Mortgage brokers not required to offer loans that are in borrowers’ best interests (although many claim they do) and compensation policies are designed to encourage exactly the opposite). • Some lenders provide incentives to brokers to put people into higher interest loans, loans with excessive fees and penalties when they could qualify for better economic terms. • Until recently, investor demand made it easy to avoid accountability - from a moral and credit quality standpoint.

What Needs To Be Done and What Is Likely To Happen? • There are two major policy areas on which to focus. CRL is actively involved in fashioning policy in these two areas: • Helping to keep people in their houses – protecting homeowners threatened with foreclosure. • Protecting Borrowers in the Future

Protecting People Threatened With Foreclosure –Ballast or Bailout? • Who should/will bear the losses that are occurring? • Taxpayers • Investors • Homeowners • Taxpayer sponsored “bailout” of borrowers not needed. Would create a moral hazard and encourage a repeat. Sensible strategies needed to minimize economic impact of large scale foreclosures on families, communities and national economy. Lenders/investors better off as a result – fewer loans in foreclosure, less REO, higher home prices, etc.

Helping Borrowers Keep Their Homes – The Landscape 40% - Refinance existing loans to prime, fixed rate loans (GSEs, FHA…) 20% - Loan modification – extend initial rate (programs are appearing). 20% - Loan modification – reduce rate or loan balance up to 50% - to between fair value and liquidation cost. Avoid Bankruptcy. 10% - Speculative or investor loans. (Not much sympathy for this group.) 10% - Borrowers where feasible assistance will not be enough to avoid bankruptcy.

Targeted Approach To Help Borrowers Keep Their Homes • Direct servicers to make meaningful and sustainable modifications to existing loans. President, Treasury Secretary, FDIC all speaking out. More action is needed and forthcoming. • Eliminate anomaly in the bankruptcy code (Chapter 13), which allows judges to modify unaffordable mortgages on vacation homes and investment properties but not on borrower’s primary residence.

Aren’t Loan Modifications “Un-American”? • Who owns my loan, anyway? It was sliced and diced and sold. Must deal with a servicer – not lender. • Servicers fear investor lawsuits. • Servicers are overwhelmed – set up mainly to process payments. • “Piggyback” seconds on 30+% of recent subprime loans – neither first nor second lien holder has incentive to help the other. No…but loan modifications are often difficult to obtain because:

Possible Standards For Modifying Loans in Bankruptcy Court • Bifurcate into two classes: • First – secured by appraised value of property. If necessary, modify interest rate to a fixed rate and amortize over the remaining life. • Second – remainder of loan – on par with other unsecured debt. • Overall plan structured so borrower emerges with manageable payments, debt load and can sustain further drop in price of house. • Bankruptcy law change will reduce servicers’ fears of being sued and establish standards for sustainable loan modifications.

Protecting Future Subprime Borrowers Expect significant regulation – perhaps “over-regulation” • Joint Banking (Regulatory) Guidance for Non-traditional (’06) and Subprime (’07) Mortgage Loans • Federal Reserve rules under review – Fall 2007 – (FRB has authority to prohibit mortgage loans and refis that FRB finds to be abusive, unfair, deceptive, or not in the interest of the borrower) • Federal legislation – likely to focus on the following items: • Prepayment penalties and payment of yield spread premiums • Escrows for taxes and insurance • Underwriting to fully indexed rate – w/ reasonable debt/income • Income verification/documentation • “Flipping” when net tangible benefit of refi is less than fees charged • Availability of credit counseling

Other Suggestions To Protect Borrowers • Enhance documentation • Less is more – who reads all this “stuff”? • Plain English • Self Defense: • Responsibility of families and educational system to increase level of financial literacy. Knowledge = power! Conclusion: There is much that can and will be done to help borrowers stay in their homes. Expect quite a bit of government/regulatory/ legislative action in the next 6 months as well as overreaction. Stay tuned!