Download

1 / 13

140 likes | 1.14k Views

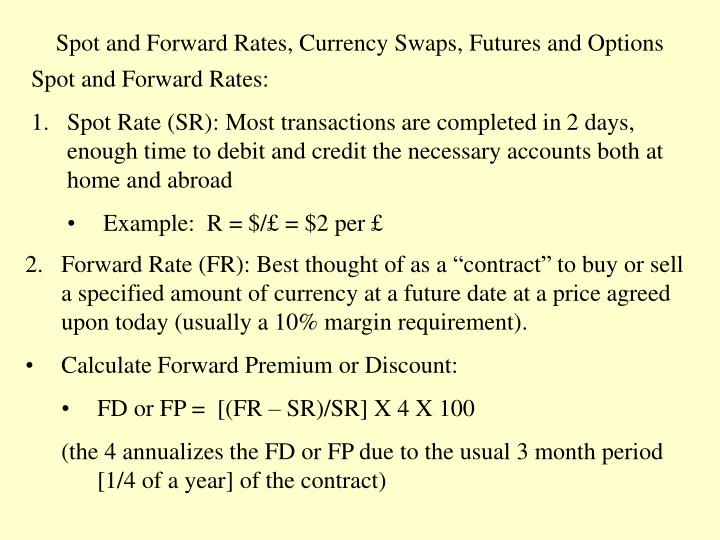

Spot and Forward Rates, Currency Swaps, Futures and Options. Spot and Forward Rates: Spot Rate (SR): Most transactions are completed in 2 days, enough time to debit and credit the necessary accounts both at home and abroad Example: R = $/ £ = $2 per £.

E N D

Spot and Forward Rates, Currency Swaps, Futures and Options • Spot and Forward Rates: • Spot Rate (SR): Most transactions are completed in 2 days, enough time to debit and credit the necessary accounts both at home and abroad • Example: R = $/£ = $2 per £ • Forward Rate (FR): Best thought of as a “contract” to buy or sell a specified amount of currency at a future date at a price agreed upon today (usually a 10% margin requirement). • Calculate Forward Premium or Discount: • FD or FP = [(FR – SR)/SR] X 4 X 100 • (the 4 annualizes the FD or FP due to the usual 3 month period [1/4 of a year] of the contract)

Currency Swaps: Combined transactions are treated as one which saves transactions costs • Sell currency (in the spot market) and simultaneously repurchase the same currency in the forward market: mostly used by banks • Example: Suppose Regions Bank receives 5 million Euros that it will need in 3 months. However, they would prefer to hold dollars for the next 3 months (until they need the Euros). • They execute a currency swap: They sell the Euros in the spot market and simultaneously repurchase Euros in the forward market. • Spot Transactions and Swaps are the most common transactions in interbank trading • 40% spot • 10% forward • 50% swaps

Foreign Exchange Futures: Began in 1972 and they are becoming more popular • Contract size is fixed (approximately $100,000) • Daily limit is set on rate fluctuations • Only 4 dates per year are available: the 3rd Wednesday in March, June, September and December • Only a few currencies are traded: Yen, Mark, Canadian $, British £, Swiss Franc, Australian $, Mexican Peso, Euro and U.S. $ • Only traded in a few locations: Chicago, New York, London, Frankfurt, and Singapore • Amounts are usually smaller than in the forward market • The forward and futures market are connected through arbitrage. • Transactions costs are higher than in the forward market • The market is increasing in size and importance.

Foreign Exchange Options: Began in 1982—limited to the Euro, British £, Canadian $, Japanese Yen and Swiss Franks • Call Option: Contract giving purchaser the right but not the obligation to buy • Put Option: Contract giving purchaser the right but not the obligation to sell European Option: A standard amount of currency on a stated date American Option: A standard amount of currency at any time before a stated date

Foreign Exchange Options (continued) • Buyer of the option can either exercise it or not • Seller must fulfill the contract if the buyer so desires • Therefore: the buyer of the option usually pays a 1-5% premium

Foreign Exchange Risks, Hedging and Speculation: • If a future payment is to be made or received [called an open position], risk is involved. • Reason: Both the spot and forward rate are constantly in motion However, most people are risk averse—especially “bidness” people • Types of Exposure: • Transaction Exposure (future payment/receipt) • Accounting Exposure (valuation of inventories and assets abroad translated into native currency) • Economic Exposure (future profitability valued in domestic currency

Hedging: Covering an open position (avoiding exchange rate risk) Example: A U.S. exporter expects to receive £100,000 in 3 months [possible hedges] • Borrow £100,000 at current spot rate • Deposit in bank and earn interest for 3 months • Cost = difference in interest paid and received • Borrow £100,000 at current spot rat • Exchange for $’s at the current spot rate • Deposit in bank and earn interest for 3 months • Cost = difference in interest paid and received Major Disadvantage: In both cases £100,000 is tied up for 3 months

Alternative to the Previous Hedge: • Importer: Buy £100,000 forward for delivery in 3 months at today’s forward rate • If £’s at the 3 month forward rate are selling at a 4% premium per year, the importer will pay (assuming $/£ = 2) $202,000 in 3 months for £100,000 (or 1% of 200,000) • Exporter: Sell £100,000 forward for delivery in 3 months at today’s 3 month forward rate (because they have already sold the currency they expect to receive in 3 months, they have locked in the rate.) • Notice: None of the Exporters funds have been tied up and no borrowing has occurred It is also possible to do the same transactions with options!

Speculation: Creating an intentional “open position” • Spot Market: • If a foreign rate is expected to rise • buy that currency in the spot market • Deposit in a bank for 3 months to earn interest • Sell at a profit • If the domestic rate is expected to fall • Borrow foreign currency • Deposit in bank for 3 months to earn interest • Buy domestic currency at a profit

Speculation: Creating an intentional “open position” Forward Market: • If the spot rate is expected to be higher in 3 months than the current forward rate • Buy forward • In 3 months, sell at a profit • Example: FR = $2.02/£ and the expected spot rate is $1.98/ £ • Sell at $2.02 in 3 months and buy at $1.98 • Option Market: • Speculator could buy an option to sell £’s at $2.02/ £ • If the spot rate falls to $1.98, exercise the option

Definitional Stuff • Long Position: • A speculator buys a foreign currency in the spot, forward or futures market, or • Buys an option to buy • Short Position: • A speculator borrows (spot), or • Sells forward

Interest Arbitrage Uncovered: Interest rates vary among countries. So, it might be advantageous to invest in another country to earn that county’s interest • Scenario: 3 month T-Bill [6% in N.Y.] [8% in London] • U.S. investor exchanges $’s for £’s at current spot rate and buys British T-Bill. • At maturity, T-Bill is redeemed and U.S. investor uses the proceeds in £’s to buy $’s. • If there is 0 change in spot rate, 2% return is earned • If the £ depreciates 2%, 0% return is earned • Consequently, covered interest arbitrage is the norm!

Covered Interest Arbitrage • Spot purchase of foreign currency • Forward sale of same currency • Us of foreign currency to buy T-Bills in foreign country • Example: T-Bills [6% in N.Y.] [8% in London] • U.S. investor buys £’s in spot market • Sells £’s in forward market at 1% discount • Buys British T-Bills at 8% • T-Bill is redeemed in £’s • £’s are sold at 1% discount • Investor earns 7% [1% more than in U.S.] • As the process continues • The price of British T-Bills and the interest they bear • As £’s are sold forward the discount increases and parity is approached [Thus, we have CIAP (covered interest arbitrage parity)