Download

1 / 48

480 likes | 755 Views

PRICE. Yes, But What Does It Cost?. Price is the value that customers give up or exchange to obtain a desired product Payment may be in the form of money, goods, services, favors, votes or anything else that has value to the other party. Opportunity Costs.

E N D

Yes, But What Does It Cost? • Price is the value that customers give up or exchange to obtain a desired product • Payment may be in the form of money, goods, services, favors, votes or anything else that has value to the other party

Opportunity Costs • The value of something that is given up to obtain something else also affects the “price” of a decision • Example: the cost of going to college is charged in tuition and fees but also includes the opportunity cost of what a student cannot earn by working instead

The Importance of Pricing Decisions • Price is the only P which represents revenue rather than an expense • Pricing and the Marketing Mix • Price and Place • Price and Product • Price and Promotion

Steps in setting price Identify objectives & constraints Estimate demand & revenue Determine cost, volume and profit Set an approximate price level Set List or Quoted price Make adjustments to list price

Identifying Pricing constraints • Demand for the Product Class, Product, and Brand • Newness of the Product: Stage in the Product Life Cycle • Single Product versus a Product Line • Cost of Producing and Marketing the Product • Cost of Changing Prices & Time Period They Apply • Types of Competitive Markets - Competitors’ Prices

Pricing Objectives • Sales or market share objectives • Profit objectives • Competitive effect objectives • Customer satisfaction objectives • Image enhancement objectives • Social Responsibility

Estimating Demand • Demand refers to customers’ desire for products • How much of a product do consumers want? • How will this change as the price goes up or down? • Identify demand for an entire product category in markets the company serves • Predict what the company’s market share is likely to be

The Price Elasticity of Demand • How sensitive are customers to changes in the price of a product? • Price elasticity of demand is a measure of the sensitivity of customers to changes in price. • Price elasticity of demand = Percentage change in quantity demanded / Percentage change in price

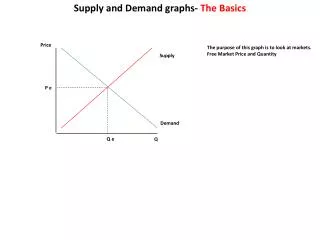

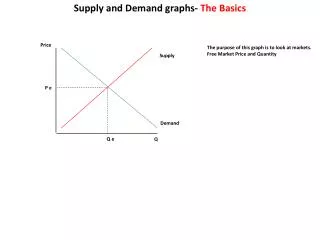

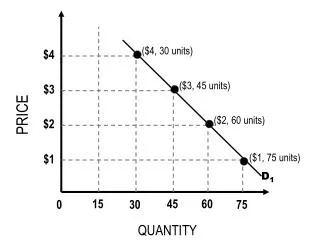

Demand Curves • Shows the quantity of a product that customers will buy in a market during a period of time at various prices if all other factors remain the same • Vertical axis represents the different prices a firm might charge • Horizontal axis shows the number of units

Influences on Price Elasticity of Demand • Availability of substitute goods or services • If a product has a close substitute, its demand will be elastic • Time period • The longer the time period, the greater the likelihood that demand will be more elastic • Income effect • Change in income affects demand for a product even if its price remains the same • normal goods, luxury goods, inferior goods

Types of Costs - 1 • Variable costs - per-unit costs of production that will fluctuate depending on how many units or individual products a firm produces • Fixed costs - do not vary with the number of units produced. Costs remain the same regardless of amount produced

Types of Costs - 2 • Average fixed cost is the fixed cost per unit produced (total fixed costs / number of units produced) • Total costs = variable costs plus fixed costs

Break-Even Analysis • Technique used to examine the relationship between cost and price and to determine what sales volume must be reached at a given price before the company will completely cover its total costs and past which it will begin making a profit • All costs are covered but there isn’t a penny left over

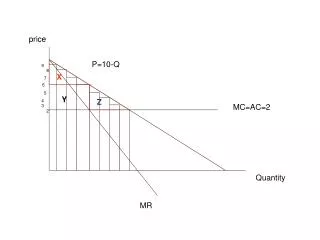

Marginal Analysis • Provides a way for marketers to look at cost and demand at the same time • Examines the relationship of marginal cost to marginal revenue • marginal cost is the increase in total costs from producing one additional unit of a product • marginal revenue is the increase in total income or revenue that results from selling one additional unit of a product

Advantages Simple to calculate Relatively risk free Disadvantages Fail to consider several factors target market demand competition product life cycle product’s image Difficult to accurately estimate costs Pricing Strategies Based on Cost

Cost-Plus Pricing • Most common cost-based approach • Marketer figures all costs for the product and then adds desired profit per unit • Straight markup pricing is the most frequently used type of cost-plus pricing • price is calculated by adding a pre-determined percentage to the cost

Steps in Cost-Plus Pricing • Estimate unit cost • Calculate markup • Markup on cost • Markup on selling price - markup percentage is the seller’s gross margin • gross margin is the difference between the cost to the wholesaler or retailer and the price needed to cover overhead and profit

Cost Plus Pricing Excerpt • Fixed costs = $2,000,000 • Number of jeans produced = 400,000 • Fixed costs per unit = $5 • Variable costs per unit = $15 • Markup as % of costs = 25% • Markup on cost • Price = total cost + (total cost * markup percentage) • Price = $20 + ($20 * .25) = $20 + $5 = $25

on Cost Price paid = $30 Markup = 40% Price = total cost + (total cost * markup percentage) Price = $30 + ($30 *.40) = $42 on Selling Price Price paid = $30 Markup = 40% Price = cost/1.00 – markup % Price = $30/ 1-.40 = $50 Markup on Cost versus Markup on Selling Price

Price Floor Pricing • Method for calculating price that considers both costs and what can be done to assure that a plant can operate at capacity • Typically used when market conditions make it impossible for a firm to sell enough • If the price-floor price can be set above the variable costs, the firm can use the difference to increase profits or cover fixed costs

Pricing Strategies Based on Demand-1 • Demand-based pricing means that the selling price is based on an estimate of volume or quantity that a firm can sell in different markets at different prices • Demand-backward pricing starts with a customer-pleasing price and works backward to costs

Pricing Strategies Based on Demand-2 • Chain-Markup Pricing extends demand backward pricing from end consumer back to the manufacturer • Example: • Price customers are willing to pay = $39.99 • Markup required by retailer = 40% • Price retailer will pay $39.99 * .60 = $23.99

Pricing Strategies Based on Competition • Competitive parity - price products at near the competition • Price leadership - price products based on prices of industry leaders • Loss leaders - price products below competition

Pricing Strategies Based on Customers’ Needs • Cost of ownership strategy - price consumers pay for product, plus the cost of maintaining and using the product, less any resale value (e.g., Sanyo batteries) • Value pricing (EDLP*) - offers a fair value to consumers (e.g., Kmart’s blue light specials) ** EDLP = everyday low pricing

New Product Pricing • Skimming price - firm charges a high, premium price for its new product with the intention of reducing it in future response to market pressures • Penetration pricing - new product is introduced at a very low price • Trial pricing - product carries a low price for a limited time period

Pricing Tactics • Pricing for Individual Products • two-part pricing (e.g., country clubs) • payment pricing (e.g., easy payments for new cars) • Pricing for Multiple Products • Price bundling (e.g., monitor, keyboard, CPU in a computer package) • Captive pricing (e.g., razors and razor blades)

More Pricing Tactics • Geographic pricing • F.O.B. pricing • Zone pricing • Uniform delivered pricing • Freight absorption pricing

Discounting for Channel Members • Trade or functional discounts • Quantity discounts • Cash discounts • Seasonal discounts

Trade Discounts • Pricing structure built around list price • List price, also called suggested retail price, is the price that the manufacturer sets as the appropriate price for the end consumer • Manufacturers offer discounts because channel members perform selling, credit, storage and transportation services

Pricing with Electronic Commerce • Dynamic pricing strategies • price can be adjusted to meet changes in the marketplace • online price changes can occur quickly, easily, and at virtually no cost • Auctions • sites offer chance to bid on items • sites offer reverse-price auctions

Price Discrimination • Means that marketers classify customers based on some characteristic that indicates what they are willing or able to pay • Acceptable when price differences are in response to • changes in cost of product • changes in competitive activity • changes in marketplace

Psychological Issues in Pricing • Internal Reference Prices - consumers have a set price or price range in their mind • If the actual price is higher, consumers will feel the product is overpriced • If it is too low below the internal reference price, consumers may assume its quality is inferior • Competition as Reference Price - If the price is close, the assimilation effect will encourage the customer to think the products are similar enough and choose the lower priced product

Price-Quality Inferences • If consumers are unable to judge the quality of a product through examination or prior experience, they usually will assume that the higher-priced product is the higher-quality product

Price and Quality Consumers tend to associate high prices with high quality. This Belgian ad for Chat Noir coffee tries to suggest otherwise. It reads, “Quality coffee. But we’ve really squeezed the price.”

Psychological Pricing Strategies • Odd-even pricing • Price lining

Legal and Ethical Considerations in Pricing • Deceptive pricing practices • Price discrimination

Deceptive Pricing Practices • Retailers must not claim prices are lower than competitors unless it is true • A going out-of-business sale should be the last sale before going out of business • Bait-and-switch - consumers are lured into store for a very low price, but then the item is not available. A more expensive product is offered instead • Trading up is acceptable

Price Discrimination • Means selling the same product to different wholesalers and retailers at different prices if practices lessen competition

Price Fixing • Occurs when two or more companies conspire to keep prices at a certain level • Horizontal price fixing occurs when competitors making the same product jointly determine what price they each will charge • Vertical price fixing occurs when manufacturers attempt to force the retailer to charge the suggested retail price

Predatory Pricing • Means that a company sets a very low price for the purpose of driving competitors out of business

Dumping (US) • Selling in foreign market at or below cost • Selling in a foreign market more than 5% below price in home market