Download

1 / 28

280 likes | 288 Views

Health, Prescription, HSA and FSA Benefits Overview. School District of Beloit. SDB Health Care Plan. The School District of Beloit offers employees a High Deductible Health Plan with an HSA (HDHP/HSA):

E N D

Health, Prescription, HSA and FSABenefits Overview School District of Beloit

SDB Health Care Plan • The School District of Beloit offers employees a High Deductible Health Plan with an HSA (HDHP/HSA): The School District makes an annual deposit of $1500 per single contract; $3000 per family contract into a Health Savings Account (HSA) that is owned by the employee. In this plan, unused funds are kept by the employee. • For mid-year enrollees, HSA contributions will be calculated on a pro-rata basis with 1/12th per month of the anticipated service period being pre-funded on the 1st of the month following the enrollment in the Employer Sponsored Group Health Plan. • SDB reviews HSA employer contributions annually based on budgetary constraints.

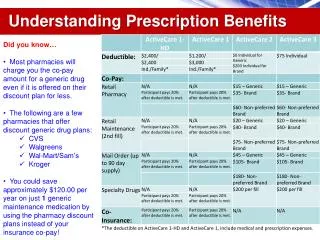

SDB Health Care Plan Under the HSA plan, all prescription drugs are subject to a combined medical/prescription drug plan year deductible of $2500 per single/$5000 per family, before the prescription drug card copay benefit applies. Under the HSA plan, there is no individual deductible cap. Therefore one family member may satisfy the full family deductible of $5,000*. (Remember the School District provides you with $1500/$3000 in an HSA account to assist in covering these expenses)

Prescription Plan Design – Optum REMEMBER – Once you have met out of pocket maximum, you will not pay for prescriptions co-pays. A Mail Order Benefit is also available and information pertaining to this benefit is available at www.catamaranhomedelivery.com The copayments apply AFTER your deductible has been met. Please refer to the SDB Health Plan Document located online for specific plan limitations/exclusions.

SDB Health Care Plan • The following office visit copayments for services obtained at a PPO Network Provider. You are responsible for the copay, in addition to the plan deductibles, for each date of service. • Annual Wellness Benefits – Paid at 100% as required by the Preventive Services Task Force. • Physician Office Copay - $20 per visit (includes Specialists, Therapies and Chiropractic Care) • Urgent Care Copay - $30 per visit (copay waived at Beloit Health System only) • Emergency Room Copay - $75 per visit • (copayment is waived if admitted) applies to all emergency room visits until out of pocket maximum has been met, regardless if deductible has been met or not • You are also responsible for the copayment, however HSA money can be used to pay these expenses.

Health Plan Claims Processing: • The School District of Beloit is self-funding and has partnered with Prairie States Enterprises (PSE) to administer payment of claims. • The School District of Beloit has partnered with the Alliance as our PPO network. In network claims are sent to the Alliance for discounting before PSE processes the claims. • PSE processes claims on a weekly basis. • At the end of the month, PSE mails a consolidated Explanation of Benefits (EOB) of all medical claims processed to your home. Should you wish to have access to your EOBs sooner, you can access those online by setting up an online account with PSE.

What is an HSA? A health savings account (HSA) is an account that you can use to pay medical expenses. Must be in conjunction with a high-deductible health plan (HDHP) You own the account, but both you and your employer can contribute funds Tax-advantages: contribute pre-tax money, funds accrue tax-free and withdraw funds tax-free (if used for eligible medical expenses)

Benefits of an HSA Triple tax advantage means you save money on your health care expenses Funds rollover each year, so you can use your HSA to save tax-free money for medical expenses after retirement You own the account, even if you leave the company

High-Deductible Health Plan HSAs can only be offered with a high-deductible health plan (HDHP). This is a plan that must provide coverage as follows: Minimum deductible: $1,300 single, $2,600 family (2016 limits, established by the IRS) Maximum annual out-of-pocket for network providers: $6,550 single, $13,100 family (2016) Though the deductible is higher for this plan than traditional plans, your monthly premium is lower, and HSA funds can pay for medical expenses subject to the deductible.

How Does The HSA/HDHP Work? You contribute money to the HSA in the following ways: Through payroll deduction on a pre-tax basis. SDB has a preferred arrangement with a financial institution, or you can work directly with your own bank/credit union. SDB will withhold and appropriately transfer deposits to your financial institution of choice; OR A lump sum deposit usually made on an after tax basis. Amounts deposited in this manner can be taken as a deduction when filing IRS taxes. Please see your tax advisor for assistance with lump sum deposits.

Who is Eligible for an HSA? Anyone who is: Covered by an HDHP Not enrolled in Medicare Not covered under other health insurance* Not another person’s dependent * Other health insurance does not include: specific disease or illness insurance, accident, disability, dental care, vision care and long-term care insurance

HSA Contribution Limits Each year, the IRS sets contribution limits These limits are for the total funds contributed, including company contributions, your contributions and any other contributions. 2017 limits: $3,400 for individual coverage $6,750 for family coverage 2018 limits: $3,450 for individual coverage $6,900 for family coverage $1,000 catch up allowed for those over age 55

HSA Contributions You are allowed to contribute the entire year’s limit when you first become eligible for the HSA, as long as you are still eligible on the first day of the last month of your tax year (December 1 for most taxpayers). However, if you join mid-year and contribute the maximum amount to your HSA, you must remain eligible for at least 12 months after the last day of the last month of that tax year (December 31 for most taxpayers), or you will be subject to taxes and penalties on the amount you contributed. We encourage you to work with your tax consult or financial planner in setting up these types of accounts.

Catch-Up Contributions For individuals ages 55-plus, the IRS allows additional “catch-up contributions.” Eligible individuals may contribute an extra $1,000 for the year This rule is meant to help save additional money for retirement.

HSA Distribution Rules Distributions from your HSA are tax-free if they are taken for “qualified medical expenses.” Your HSA can only be used for expenses that are incurred on or after the date the HSA was established. However, HSA funds can be used for expenses from a prior year, as long as the expenses incurred on or after the date the HSA was established.

HSA Distribution Rules HSA distributions can be taken for qualified medical expenses for the following people: The account holder (person covered by the HDHP) Spouse of that individual Even if not covered by the HDHP IRS eligible Dependents of that individual Even if not covered by the HDHP Please note that the definition of a Dependent under your Health Plan is not the same as the IRS definition of an eligible dependent and could provide some gaps in coverage. A separate HSA account can be set up for the dependent if they are not an IRS dependent of another individual

Qualified Medical Expenses The IRS defines expenses that are considered “qualified medical expenses” for HSA distributions. Expenses must be primarily to treat or prevent a physical or mental defect or illness. If you use HSA funds for expenses beyond what the IRS defines as qualified, you will be subject to income tax on the distribution and an additional 20 percent penalty.

Distributions – Age 65-plus For individuals age 65 and older, HSA distributions can be used for non-qualified medical expenses without facing the 20% penalty. However, income taxes will apply for non-medical distributions. This rule is regardless of whether the individual is enrolled in Medicare. We strongly encourage you to work with your tax consultant or financial planner if using your HSA for expenses other than qualified medical expenses.

Qualified Medical Expenses Examples of qualified medical expenses include: Most medical care that is subject to your deductible (copays, coinsurance, doctor visits, inpatient or outpatient treatment, etc.) Prescription drugs Over-the-counter drugs, only if you obtain a prescription Insulin (with or without a prescription) Dental and vision care Select insurance premiums COBRA, qualified long-term care insurance, health insurance premiums paid while receiving unemployment benefits, health insurance after you turn 65 except for a Medicare supplemental policy If you have previously had coverage under an FSA plan, the eligible qualified medical expenses are the same.

Ineligible Medical Expenses Expenses that are not considered “qualified medical expenses” include: Insurance premiums (other than the exceptions listed on the previous slide) Over-the-counter drugs (unless a prescription is retained from a physician – insulin is an exception) Surgery purely for cosmetic reasons Expenses covered by another insurance plan General health items such as tissues, toiletries, hand sanitizer

Recordkeeping Whenever you use HSA funds to pay for a medical expense, you should keep your receipt. You may need to demonstrate to the IRS that HSA distributions were for qualified medical expenses. If the IRS requests receipts for verification purposes, failure to provide those receipts could result in having to pay a penalty.

Limited Purpose Flexible Spending Plan • A Section 125 Limited Purpose Flexible Spending Account allows employees to put money away on a pre-tax basis to pay for: • Dental and Vision expenses • Tax Advantage - Estimated Employee Savings: • 25% - 30% of the contribution based on employee tax bracket. • No Federal, State or FICA taxes taken on deduction amount.

Limited Purpose Flexible Spending Plan • The maximum amount you can put in a Flexible Spending Account to pay for these expenses is $2,500. • The deduction for 26 pays would be $96.15 from each paycheck. • The full election amount of $2,500 is available September 1st to help pay for qualified dental and vision expenses.

Dependent Care Expenses Dependent Care FSA • Allows employees to put away up to $5,000 on a pre-tax basis to pay for day care expenses incurred so the employee can work. • Eligible Expenses must satisfy the following: • The day care provider must file taxes and be willing to write you a receipt for services. • Dependents must be less than 13 years of age and claimed on your taxes. • Dependent Care may also apply to a physically or mentally challenged spouse or family member for whom you are legally responsible and claim as an exemption on your taxes. • Employee Note: You can only be reimbursed for amounts previously withheld from your paycheck.

How Does It Work? • If you decide to enroll in the program you will be required to make an Annual Electionregarding the amount of money you wish to put into each account. • This amount will be taken out of each paycheck — before taxes — in equal installments throughout the plan year. These dollars are then placed into your FSA. • Employees cannot change the Annual Election unless they have a qualified family status change, or a loss of other coverage. • Expenses must be carefully determined as funds not used by the employee will be forfeited to the plan. Use it or Lose it! • Employee Advantage – Cash Flow– Your full Annual Election for your medical FSA will be available to you as of the first day of the plan year. If you use more money than you have had deducted from your paycheck, you will pay back the amount over the course of the plan year.

Remember: • Claims must be incurred between September 1, 2017 and August 31, 2018. • Claims must be filed for reimbursement within 90 days following the end of the plan year or prior to November 28, 2018.