Download

1 / 23

230 likes | 473 Views

Infrastructure Finance via the Yen Capital Markets ~ Exploring opportunities. February 14 th . 2008, New Delhi Tetsuya Kodama Managing Director, Global Capital Markets Deutsche Securities Inc. Tokyo, Japan. Growth of Yen Markets for International Issuers Section 1.

E N D

Infrastructure Finance via the Yen Capital Markets ~ Exploring opportunities February 14th. 2008, New Delhi Tetsuya Kodama Managing Director, Global Capital Markets Deutsche Securities Inc. Tokyo, Japan

Growth of Yen Markets for International Issuers • The following dynamics continue to increase interest among Japanese investors to look for new quality investment opportunities, allowing the yen markets for international issuers to grow • Continuation of low interest rates in Japan vs other major currencies • Investors need to look for spread products • Absolute yield could be attractive to issuers • Supply of domestic corporate bonds are stable, and the spreads remain tight • Since mid 2007, spread levels available in international markets have become extremely attractive from the domestic investors’ viewpoint (while still being attractive to issuers) • With most of the above conditions expected to be sustained well into 2008 or even 2009, we expect a continued growth of the Yen markets for international issuers • So far, strong concentration in Financial names ⇒Interest to see non financial names/ credits • Samurai Bonds (Domestic Bonds) vs Euro-yen Bonds (International Bonds) • Many Japanese pension funds and regional financial institutions can still only buy domestic bonds (Samurai format is domestic) but not International Bonds (Even in Yen, Euro-yen / Global-Yen bonds are treated as international bonds)

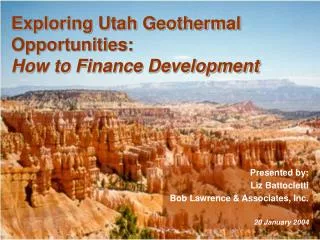

Samurai Issuance (2000~) Samurai Issuance

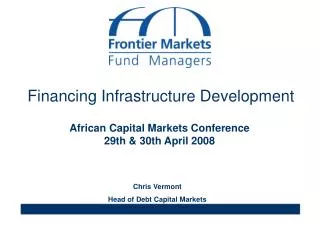

Samurai Issuance (2007~) *FRN **Structuerd

Who is behind the growth? Section 2

Major Investors in Japan (1) Description Investment Criteria Target maturity Minimum Required Rating (R&I / JCR) Investment size(100mil) City Banks • City banks offer banking services to relatively many large corporate customers in Japan. Due to the series of mergers, Japan is now left with several mega banks. Currently there are 10 City Banks. • Liquidity • Spread • BIS risk weight • 2~10 years. (Mainly up to 5 years) • 3~5 years FRN • BBB • 10~ Regional Banks • The principal mission is to contribute to the social and economic development of the Japanese regions. Traditionally, there were 64 banks which were referred to as "regional banks" in Japan, but due to the conversion of Sogo banks , this number has now doubled. • Yield • BIS risk weight • Spread • Liquidity • 1~10 years. • Mainly up to 5 years for non-Japanese • 3~5 years FRN • BBB • Preferred A~AA • 5 or 10~ Trust Banks • Trust banks are unique among Japanese financial institutions in that they combine financing services with asset management services. Pension funds are big player of public corp. bond and Samurai. • Liquidity /Spread • BIS risk weight • 2~10 years • 3~5 years FRN . • Own portfolio • BBB • 10~ • Index • Spread / Liquidity • 2~20 years. • BBB • Preferred A~AA • Pension trust • Active10~ • Passive1~ Life Insurance Companies • The number of life insurance companies operating in Japan is 38, as of March 2006. More than 90% of the population owned life insurance and the amount held per person was at least 50% greater than in the United States. The most important player of long dated bond (10 year or longer). • Yield • Duration (ALM) • Spread • Liquidity • 2~40 years. • Preferred 10~20 years • BBB • Preferred A or better • 10~ Non-life Insurance Companies • As of December 1, 2006, a total of 48 general insurance companies are operating in Japan. A total of 26 companies were licensed as domestic insurers, including 4 foreign capital domestic insurers, while 22 companies were licensed as foreign insurers. • Liquidity • Yield • Spread • 2~30 Years • Up to 5 years preferred • BBB • Preferred A or better • 5 or 10~

Major Investors in Japan (2) Description Investment Criteria Target maturity Minimum Required Rating (R&I / JCR) Investment Size (100mil) Asset Management • Rating • Liquidity • Up to 5 years • Preferred 1~3 years • 1~5 years FRN • BBB • Preferred Aor better • 2 or 3~ 10 • As of July 2007, over 120 asset management companies are operating in Japan. Pension Funds are big player of public corp. bond and Samurai bond. • Investment trust • Pension Fund • Index / Spread • Liquidity • BBB • Preferred BBB~A • Active10~ • Passive1~ • Any maturity Public Entities (Japan Post) • As a institutional investor, Japan Post is the largestin a public sector in Japan. It runs the world's largest postal savings system and is often said to be the largest holder of personal savings in the world. Now it is under the process of privatization toward March 2017. • Yield • Spread • Liquidity • Rating • Issuer’s industry • 3~20 years • Preferred 2~10 years • A • 20 or 30~ Public Entities (Pension) • Gov. Pension Investment Fund is the most biggest pension fund manager and big player of corp. bond. • Index • 2~30 years • BBB • Preferred A or better • 5~ • Large fund 20 or 30~ Public Entities (Regional) • Mainly, Mutual Aid Association which is a pension fund for employees of public sector. • Rating • Yield • A • 10 ~ 50 • 2~20 years • Preferred 5~10 years Upper organization of regional financial Institutions • 2~20 years • Federations of Cooperative Financial Institutions. TheNorichukin Bank which is the central bank for the Japanese agricultural, forestry, and fishery cooperatives is the largest upper organization. • Zenkyoren is managing agricultural insurance money and one of the biggest 10 and 20 year player of high grade bonds. • Relative value • Credit spread • Yield • Risk weight • BBB • 10 or 20 ~100

Major Investors in Japan (3) Description Investment Size (100mil) Investment Criteria Target maturity Minimum Required Rating (R&I / JCR) Regional financial Institutions • ~5 or 10 • Regional financial Institutions, such as Shinkin Bank, Shinkumi Bank, Rokin (Labor) Bank and JA Bank • Yield • Spread • Risk weight • Liquidity • 2~20 years • Preferred 3~10 years • 2~5 years FRN • BBB • Preferred A~AA • Such as foundation, school and religious corp. • 5 or 10 ~ 30 Non-Profit Organization • Yield • Rating • 1~30 years • BBB • Preferred high grade • Over 1,000 corporate are covered by DB and main target are cash rich companies. • 5~50 Corporation • Yield • Rating • 1~10 years • 1~5 years FRN • BBB • Preferred high grade • 10~ • Can be categorized into non-resident and resident. • resident • Not particular International Investors • Public sector • Asset swap spread • 1~40 years • Non-resident (Bank, Asset Manager, Insurance) • 30~200 • Asset swap spread • 1~40 years • Not particular

How to utilise the Yen capital markets? Section 3

Investor Characteristics and Solutions Investor Characteristics • The Japanese investor base tends to have a very “flat” credit curve, until a certain point where it become “vertical” • Past experiences with international credits created a conservative / Risk averse stance • Past “experiences” include; Russia, Xerox, Enron • On the other hand, they would be big investors of credits they feel used to / comfortable with • Examples include; Thailand. Increased interest in India How to bring the investors closer • Increase information flow to increase “familiarity” • Support transaction via structuring to take away the “unacceptable” level of uncertainty • Especially in cases such as cross border project finance / project related financing

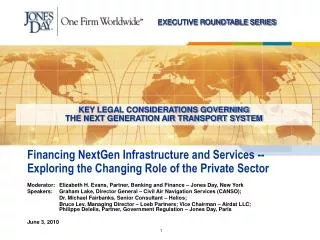

Sample concept ⇒Public Support of project via providing risk money Assets Senior Debt Bond Loans Senior Bond Investors Senior Lenders Sponsors Financial Investors Etc. Capital Mezzanine / Capital Cash Flows Public Funds and/or Support

ICICI Bank Ltd ICICI Bank Ltd State Bank of India State Bank of India UTI Bank UTI Bank UTI Bank UTI Bank USD 2 billion 3 USD 2 billion 3 - - tranche tranche USD 200 million USD 200 million USD 250 million USD 250 million USD 250 million USD 250 million 3mL + 54 bps FRN due 2010 3mL + 54 bps FRN due 2010 Floating Rate Notes due 2011 Floating Rate Notes due 2011 Floating Rate Notes due 2010 Floating Rate Notes due 2010 Floating Rate Notes due 2010 Floating Rate Notes due 2010 5.750% Fixed Note due 2012 5.750% Fixed Note due 2012 6.375% Upper Tier 2 15NC10 6.375% Upper Tier 2 15NC10 Sole Bookrunner Sole Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner January 2007 January 2007 January 2007 January 2007 January 2007 January 2007 Joint Bookrunner Joint Bookrunner January 2007 January 2007 Best Emerging Markets Bond House Best Debt Arranger 2007 Best Debt House in Asia 2007 December 2007 2007 ICICI Bank Ltd ICICI Bank Ltd US$ 2 billion US$ 2 billion 6.625% Fixed Rate Notes due 6.625% Fixed Rate Notes due December 2007 2012 2012 July 2007 Joint Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner September 2007 September 2007 Awards for Excellence 2007 IFR AsiaWinner Emerging Asia Bond 2007 — ICICI USD2bn Three-tranche Global IFR Asia Winner Best Investment Grade Bond 2007 — ICICI Bank USD2bn Offering 2007 Best Investment Grade Bond 2007 — ICICI Bank USD2bn 3-tranche Deal State Bank of India State Bank of India State Bank of India State Bank of India State Bank of India State Bank of India State Bank of India State Bank of India State Bank of India State Bank of India State Bank of India State Bank of India USD 300 million USD 300 million USD 300 million USD 300 million USD 300 million USD 300 million USD 400 million USD 400 million USD 400 million USD 400 million USD 400 million USD 400 million Senior Floating Rate Notes Senior Floating Rate Notes Senior Floating Rate Notes Senior Floating Rate Notes Senior Floating Rate Notes Senior Floating Rate Notes 6.439% Hybrid Tier 1 6.439% Hybrid Tier 1 6.439% Hybrid Tier 1 6.439% Hybrid Tier 1 6.439% Hybrid Tier 1 6.439% Hybrid Tier 1 due 2012 due 2012 due 2012 due 2012 due 2012 due 2012 Perpetual NC10 Perpetual NC10 Perpetual NC10 Perpetual NC10 Perpetual NC10 Perpetual NC10 December 2007 Joint Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner February 2007 February 2007 February 2007 February 2007 February 2007 February 2007 February 2007 February 2007 February 2007 February 2007 February 2007 February 2007 2007 Deutsche Bank Group Credentials in India ICICI Bank Ltd Bank of Baroda GBP 350 million USD 300 million 6.250% Fixed Rate Notes due 2010 6.625% 15NC10 Note due 2022 Joint Bookrunner Joint Bookrunner DEUTSCHE BANK IFR Asia Bank of the Year 2007 May 2007 May 2007 ICICI Bank UK PLC ICICI Bank UK PLC ICICI Bank Ltd ICICI Bank Ltd USD 500 million USD 500 million EUR 500 million EUR 500 million Triple A Assets Asian Awards 2007 Floating Rate Notes due 2012 Floating Rate Notes due 2012 Floating Rate Notes due 2009 Floating Rate Notes due 2009 Joint Bookrunner Joint Bookrunner Joint Bookrunner Joint Bookrunner Best Investment Grade Bond 2007 — ICICI Bank USD2bn 3-tranche Deal February 2007 February 2007 March 2007 March 2007 INAUGURAL WINNER 3-TIME WINNER 2005, 2006, 2007 REPEAT WINNER 2005, 2006 3-TIME WINNER 2005, 2006, 2007 REPEAT WINNER 2006, 2007 Asia Bond House of the Year Best International Bond House 2006 December 2007 December 2006

2007 Deutsche Bank Group League Tables(Yen) Thomson International Financing Review January 5 2008 Issue 1715 ifr 2007 YEARLY TABLES

IFR Magazine “Bond House of the Year 2007” “Few houses crop up in virtually every conversation regarding bonds, no matter where in the world it is held or what asset class is under discussion. Deutsche Bank is one of those few, boosting a stunning breadth of business stretching from high-grade to high yield and mainstream to emerging currencies...“ “In a volatile year, Deutsche Bank identified trends early and assisted clients across a range of structures with no currency bias…” “It is also notable that Deutsche was first bank issuer to return to market after the dislocation of the summer, when confidence was at its nadir” “The bank… played a key role in reopening the primary market in the midst of the global liquidity crisis.”