Download

1 / 14

190 likes | 716 Views

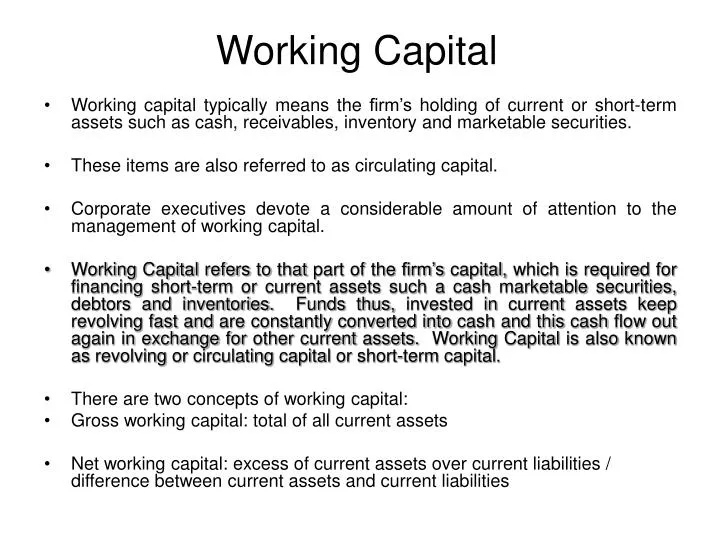

Working Capital . Working capital typically means the firm’s holding of current or short-term assets such as cash, receivables, inventory and marketable securities. These items are also referred to as circulating capital.

E N D

Working Capital • Working capital typically means the firm’s holding of current or short-term assets such as cash, receivables, inventory and marketable securities. • These items are also referred to as circulating capital. • Corporate executives devote a considerable amount of attention to the management of working capital. • Working Capital refers to that part of the firm’s capital, which is required for financing short-term or current assets such a cash marketable securities, debtors and inventories. Funds thus, invested in current assets keep revolving fast and are constantly converted into cash and this cash flow out again in exchange for other current assets. Working Capital is also known as revolving or circulating capital or short-term capital. • There are two concepts of working capital: • Gross working capital: total of all current assets • Net working capital: excess of current assets over current liabilities / difference between current assets and current liabilities

Working capital, also known as net working capital or NWC, is a financial metric which represents operating liquidity available to a business. • Working capital is really what a part of long term finance is locked in and used for supporting current activities. • circulating capital means current assets of a company that are changed in the ordinary course of business from one form to another, as for example, from cash to inventories, inventories to receivables, receivable to cash. • Along with fixed assets such as plant and equipment, working capital is considered a part of operating capital. • If current assets are less than current liabilities, an entity has a working capital deficiency, also called a working capital deficit. • When firms speak of shortage of working capital they in fact possibly imply scarcity of cash resources.

The firm has to maintain cash balance to pay the bills as they come due. • In addition, the company must invest in inventories to fill customer orders promptly. • And finally, the company invests in accounts receivable to extend credit to customers. • Operating cycle is equal to the length of inventory and receivable conversion periods. • The size and nature of investment in current assets is a function of different factors such as type of products manufactured, the length of operating cycle, the sales level, inventory policies, unexpected demand and unanticipated delays in obtaining new inventories, credit policies and current assets.

Working capital management involves the relationship between a firm's short-term assets and its short-term liabilities. • Working capital management/short-term financial management is concerned with decisions relating to current assets and current liabilities. • The key difference between long-term financial management and working capital management is in terms of the timing of cash. While long term financial decisions like buying capital equipment or issuing debentures involve cash flows over an extended period of time, short term financial decisions typically involve cash flows within a year or within the operating cycle of the firm. • The goal of working capital management is to ensure that a firm is able to continue its operations and that it has sufficient ability to satisfy both maturing short-term debt and upcoming operational expenses. • The management of working capital involves managing inventories, accounts receivable and payable, and cash. • Characteristics of current assets: • Short life span • Swift transformation into other assets forms

TYPES OF WORKING CAPITAL WORKING CAPITAL BASIS OF CONCEPT BASIS OF TIME Permanent / Fixed WC Temporary / Variable WC Gross Working Capital Net Working Capital Seasonal WC Special WC Regular WC Reserve WC

Operating cycle of a typical company Receive Cash Sell Product On credit Purchase resources Pay for Resources purchases Receivable Conversion period Inventory conversion period Cash conversion cycle Payable Deferral period Operating cycle

Importance of working capital • Risk and uncertainty involved in managing the cash flows • Uncertainty in demand and supply of goods, escalation in cost both operating and financing costs. • Strategies to overcome the problem • Manage working capital investment or financing such as • Holding additional cash balances beyond expected needs • Holding a reserve of short term marketable securities • Arrange for availability of additional short-term borrowing capacity • One of the ways to address the problem of fixed set-up cost may be to hold inventory. • One or combination of the above strategies will target the problem • Working capital cycle is the life-blood of the firm

Difference between permanent & temporary working capital Amount Variable Working Capital of Working Capital Permanent Working Capital Time

Variable Working Capital Amount of Working Capital Permanent Working Capital Time

FACTORS DETERMINING WORKING CAPITAL • Nature of the Industry • Demand of Industry • Cash requirements • Nature of the Business • Manufacturing time • Volume of Sales • Terms of Purchase and Sales • Inventory Turnover • Business Turnover • Business Cycle • Current Assets requirements • Production Cycle • Credit control

Inflation or Price level changes • Profit planning and control • Repayment ability • Cash reserves • Operation efficiency • Change in Technology • Firm’s finance and dividend policy • Attitude towards Risk

EXCESS OR INADEQUATE WORKING CAPITAL • Every business concern should have adequate working capital to run its business operations. It should have neither redundant or excess working capital nor inadequate or shortage of working capital. • Both excess as well as shortage of working capital situations are bad for any business. However, out of the two, inadequacy or shortage of working capital is more dangerous from the point of view of the firm.

Disadvantages of Redundant or Excess Working Capitalõ Idle funds, non-profitable for business, poor ROIõ Unnecessary purchasing & accumulation of inventories over required level õ Excessive debtors and defective credit policy, higher incidence of B/D.õ Overall inefficiency in the organization.õ When there is excessive working capital, Credit worthiness suffers õ Due to low rate of return on investments, the market value of shares may fallDisadvantages or Dangers of Inadequate or Short Working Capitalõ Can’t pay off its short-term liabilities in time. õ Economies of scale are not possible.õ Difficult for the firm to exploit favourable market situations õ Day-to-day liquidity worsensõ Improper utilization the fixed assets and ROA/ROI falls sharply

Working capital financing • The short term sources of finance are as follows: • Accruals • Trade credit • Working capital advance by commercial banks • Public deposits • Inter-corporate deposits • Short term loans from financial institutions • Cash credit • Hypothecation and pledge • Bank overdraft • Commercial paper • Factoring • Letter of credit