Download

1 / 5

50 likes | 180 Views

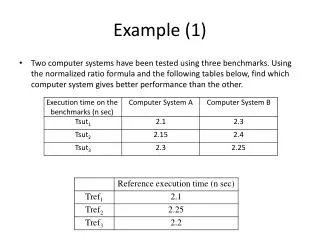

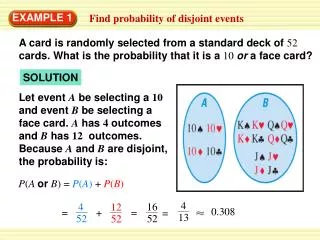

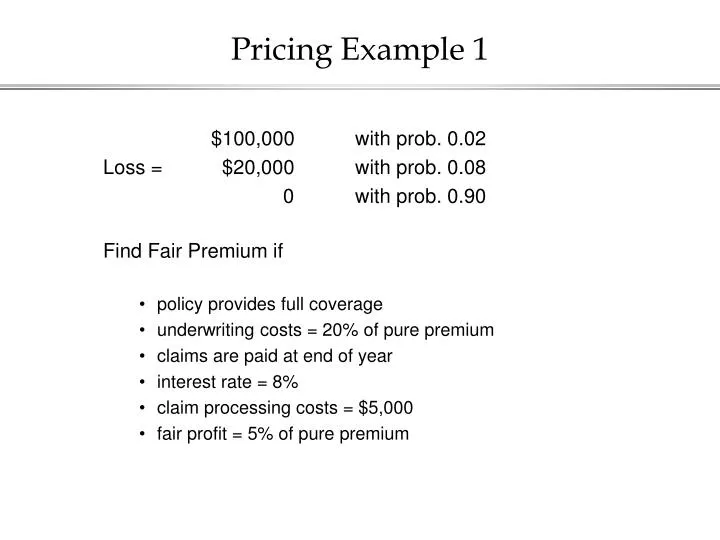

Pricing Example 1. $100,000 with prob. 0.02 Loss = $20,000 with prob. 0.08 0 with prob. 0.90 Find Fair Premium if policy provides full coverage underwriting costs = 20% of pure premium claims are paid at end of year interest rate = 8% claim processing costs = $5,000

E N D

Pricing Example 1 $100,000 with prob. 0.02 Loss = $20,000 with prob. 0.08 0 with prob. 0.90 Find Fair Premium if • policy provides full coverage • underwriting costs = 20% of pure premium • claims are paid at end of year • interest rate = 8% • claim processing costs = $5,000 • fair profit = 5% of pure premium

Pricing Example 1 • Solution: • pure premium = $3,600 • PV of expected claims = $3600/1.08 • underwriting costs + fair profit = (0.20 + 0.05) x $3,600 = $900 • expected claim processing costs = $5,000 x 0.10 = $500 • PV of expected claim processing costs = 500/1.08 • Fair premium = 900 + 4,100/1.08 = 900 + 3,796 = $4,696

Pricing Example 2 $100,000 with prob. 0.02 Loss = $20,000 with prob. 0.08 0 with prob. 0.90 Find Fair Premium if • policy has a $20,000 deductible • underwriting costs = 20% of pure premium • claims are paid at end of year • interest rate = 8% • claim processing costs = $5,000 • fair profit = 5% of pure premium

Pricing Example 2 • Solution: • pure premium = 0.02 x $80,000 = $1,600 • PV of expected claims = $1600/1.08 • underwriting costs + fair profit = (0.20 + 0.05) x $1,600 = $400 • expected claim processing costs = 0.02 x $5,000 = $100 • PV of expected claim processing costs =$100/1.08 • Fair premium = $400 + $1,700/1.08 = $400 + $1574 = $1,974

Comparison of the Two Examples • Note difference in loading on the two policies Full coverage Deductible Premium $4,696 $1,974 Expected claim cost $3,600 $1,600 Dollar loading $1,096 $374 Percentage loading 30.4% 23.4% (relative to exp. claim cost) Difference is due to the deductible policy eliminating expected claim processing cost on relatively frequent, low severity claims (see Chapter 8)