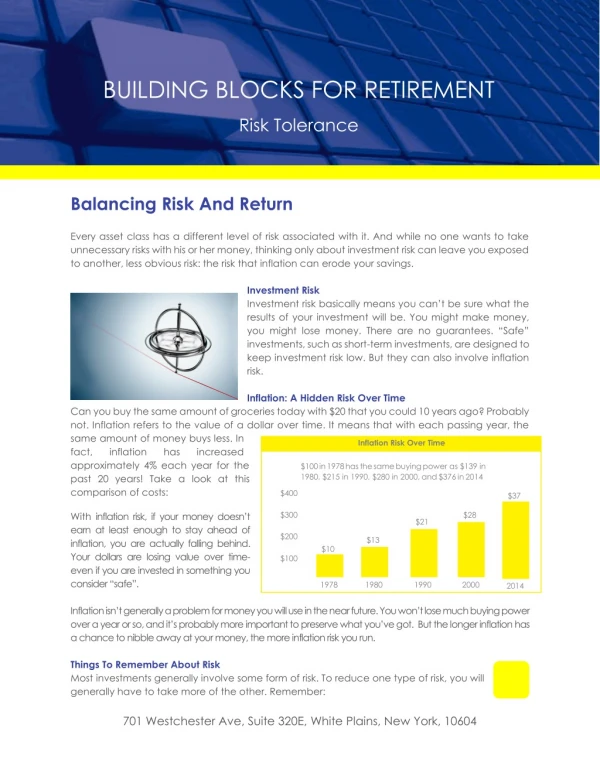

Download

1 / 0

10 likes | 138 Views

Balancing risk and opportunities. Han de Jong Chief Economist May 2014. Statement 1. The global economy is set to Strengthen Weaken Continue at its recent pace. Statement 2. In 2014, risky assets will provide Above average returns Below average returns Average returns.

E N D